This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst. This piece does not necessarily reflect the opinion of Hedgeye.

In this issue of The Institutional Risk Analyst, we update readers on the progress of the Financial Stability Oversight Counsel to root out risk, real and imagined, in the world of nonbank finance. Sadly for the mortgage industry, no matter who wins the White House in 2020, the FSOC will not go away.

The effort to address nonbank risk has been led by the Conference of State Bank Supervisors (CSBS), a trade association that informally represents the various states. An equally informal group of researchers within the Federal Reserve System is also in the vanguard of those warning about nonbank risk. But so far, the warnings of the FSOC regarding nonbanks have proven empty. The FSOC's earlier protestations regarding insurer MetLife, which was forced out of the mortgage business, were also in error.

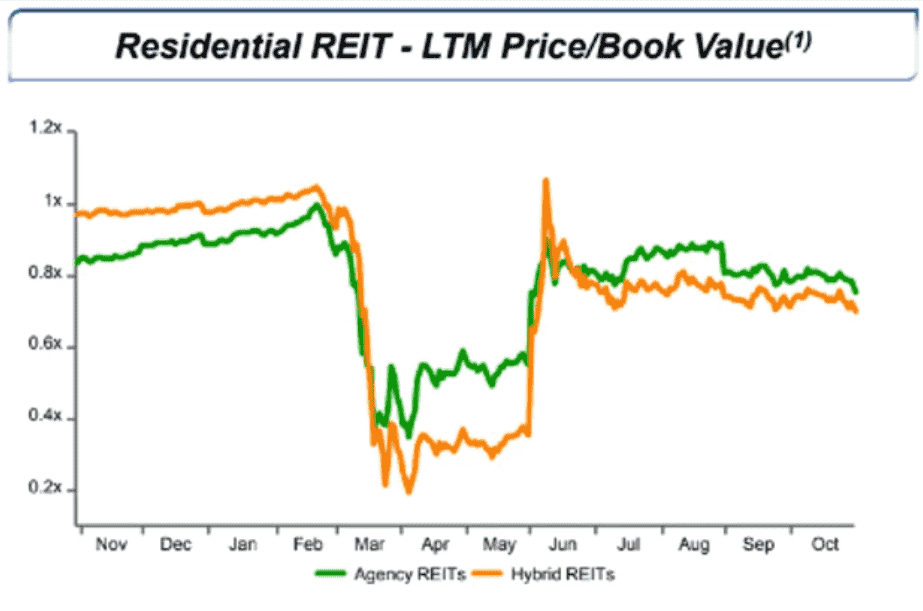

FHFA Director Mark Calabria is personally responsible for elevating this issue of nonbank risk within the FSOC, particularly regarding mortgage servicers. Director Calabria is not worried about highly leveraged hybrid REITs, you understand, but mortgage servicers.

Since 2015, the CSBS has been attempting to fashion a unified response by the states to the perceived risk from nonbank financial firms, aka independent mortgage banks (IMBs). Even though nonbank mortgage firms are already subject to regulation by Ginnie Mae and the Federal Housing Finance Agency, the CSBS believes that more need be done.

The good news is that the CSBS, in meetings with a number of mortgage firms, has proposed a quite reasonable framework for thinking about liquidity and capital that largely mirrors the current proposal out for public comment from the FHFA and the existing rules for Ginnie Mae issuers.

Also, the CSBS has advanced the marvelous idea of a streamlined state-level audit of major nonbank firms every 18 months. The regulators in different states would participate in an informal yet cooperative process, saving time and scarce resources.

Again, a seemingly positive development. More, the CSBS has encouraged the Federal Reserve to create a liquidity facility for nonbank mortgage firms. Another very positive step.

For the US mortgage industry and investors, there is an urgent need to ensure broad, uniform adoption of any framework proposed by state regulators. The CSBS recommendations are useful only to the extent they are implemented uniformly by the industry, the federal mortgage agencies and the states. The worst possible outcome, according to one industry briefing paper, is a patchwork regime of different standards or inconsistent regulations for liquidity and capital.

While the new FHFA rules for nonbanks may not take effect for some time, the industry should encourage the CSBS process. State regulators have real world concerns about the potential blowback from a nonbank failure a la 2008, but times have changed.

The nonbanks of today look nothing like rogue issuers such as Countrywide, Citigroup (C), Lehman Brothers or Bear Stearns & Co. The key question is whether the CSBS and other regulators are willing to advance their understanding of nonbank risk to fashion a workable policy.

Hint: Look for the leverage.

For example, both the FSOC and the FHFA continue to focus on stress testing and capital requirements of nonbanks through the lens of commercial bank regulation. But for nonbanks and even the GSEs themselves, a bank level approach to capital and liquidity will inevitably fail to address the true risks. Why? Because commercial banks and other creditors ultimately control the assets and liabilities of nonbank mortgage firms.

Since the SEC under Chairman Arthur Levitt wrongly amended Rule 2a-7 in the 1990s, nonbanks have been unable to sell commercial paper to money market funds. As a result, nonbank financial companies are essentially captive of the large commercial banks in terms of funding. Any risk, via secured financing facilities, is "in the bank" as we say.

The secondary source for liquidity for IMBs is the high-yield debt markets. Mortgage issuers are rarely investment grade credits on an unsecured basis. The quid pro quo for warehouse lending from banks to IMBs is deposits. Nonbanks control substantial escrow balances, which are deposited with the warehouse lender banks. Needless to say, this is a very sticky business relationship.

The liquidity of nonbank mortgage firms is a function of the willingness of commercial banks to lend against government-insured collateral. The FSOC and CSBS don’t seem to full grasp the significance of this point. Most nonbanks that do not retain servicing assets often function with net negative working capital. The whole point of secured finance beyond mortgage lending is to work with somebody else's money. Right?

Liquidity is a function of collateral, thus expecting nonbanks to increase liquidity in a countercyclical fashion before recessions, for example, is impractical. Lending volumes typically fall as an economic expansion matures. Only after unemployment rises, the Fed has lowered interest rates and mortgage lending volumes grow do liquidity levels typically rise for IMBs.

Mortgage lending is entirely cyclical, as shown over the past six months. For this reason, it is important to state that the lender banks are unlikely to abandon nonbanks, even in times of financial stress. In the dark days of 2018, when few mortgage lenders were profitable and most IMBs had breached debt covenants, the banks did not abandon the IMBs.

And this past April, when many IMBs were again technically insolvent because of the Fed’s massive open market operations in response to COVID, the banks again stepped up and supported these important commercial customers. Several IMBs that went public in the Fall were literally saved by the commercial banks and TBA dealers in April. How would the CSBS and FSOC propose to model the "risk" from Fed open market operations?

Why did the banks support the IMBs in 2018 and in April of this year? Because the vast majority of the “assets” of the IMBs are comprised of government-guaranteed loans and related servicing assets. These assets are money good as collateral and are easily sold in the event of default by the IMB. (See our 2017 comment, "Who's Afraid of Mortgage Servicing Rights.")

As the public record going back decades clearly indicates, the failure of an IMB is basically a non-event from either a credit or systemic perspective, especially once the loans and servicing assets are sold under the protection of the Bankruptcy Court. For some odd reason, neither the FSOC nor the CSBS nor the FHFA nor the Office of Financial Research have taken notice of the public record regarding failure of IMBs.

Another area of investigation by the CSBS and FSOC is whether nonbanks should have “living wills” like large commercial banks. The answer clearly is no. First, by law the GSEs and Ginnie Mae have preemptive rights with respect to the government-insured loans and servicing assets "owned" by IMBs. If an IMB fails, the GSEs and Ginnie Mae will unilaterally transfer responsibility for servicing the loans. Then the remaining assets are liquidated. Please remember to turn off the lights.

Second, in the event of a default, the Bankruptcy Court will essentially ignore the living will of an IMB. Just as the CSBS has no legal authority or sovereign immunity, a living will for an IMB is a waste of paper and toner.

Keep in mind that the FDIC acting as Receiver for a failed commercial bank would ignore a living will mandated by Dodd-Frank. The millions spent preparing the living will of a large bank is completely wasted effort. A similar document for a nonbank is equally pointless. Those who work with Trustees and Receivers know these things.

The Trustee in a bankruptcy is responsible to the Bankruptcy Court and the estate, not to state regulators. Historically, the GSEs and Ginnie Mae have not entered bankruptcy proceedings for IMBs or FDIC bank receiverships as parties. Without a defined receivership process as in the case of 12 USC for federally insured banks, there is no choice other than federal bankruptcy for an insolvent mortgage lender or servicer.

The other bone of contention between the CSBS, FSOC and the nonbanks is the notion that, like commercial banks, IMBs ought to do annual stress tests. As we noted in our recent report in The IRA Premium Service (“Bank Profiles: Morgan Stanley vs Goldman Sachs”), the Fed’s stress tests are a political circus more than an analytical exercise. But this fact has not prevented the other agencies in Washington, including the FHFA, from copying the Fed’s bad example.

So far, the only agency that has been able to assemble an effective stress assessment process for IMBs is Ginnie Mae and HUD. The stress testing is conducted internally by HUD with input from the issuers, rather than imposing this huge analytical burden on nonbanks directly.

The Ginnie Mae process is viewed as a success by issuers and is an example of cooperation between industry and regulators to address liquidity and other issues.

Since the Ginnie Mae market is by far the most demanding and high-risk agency sector from an operational perspective, it makes sense that the new capital and liquidity standards for Ginnie Mae issuers should be the basic point of departure for the CSBS and the FSOC. And as the CSBS gets better acquainted with the Ginnie Mae approach to regulation of nonbanks, they will begin to understand the riddle of liquidity.

In all of the doom and gloom scenarios the come from FSOC and the CSBS with respect to nonbanks, there is no actual evidence of a mortgage lender or servicer causing systemic risk because of a liquidity problem. There are no examples of a failing hybrid REIT causing a global financial meltdown, for example, although we almost tested that in April. Wall Street investment banks like Lehman and Bear, and subprime lenders like Citibank, created and spread toxic assets throughout the financial system before 2008.

Indeed, there is no evidence to support the contention by the FSOC and Director Calabria that nonbank mortgage companies pose a systemic risk. IMBs are leveraged lenders and asset managers that generate a lot of cash, at least for the moment.

But the one thing you can be sure of is that if you stress test a nonbank using the same criteria as a commercial bank, all the nonbanks will fail every time. The liquidity of nonbanks is a function of the willingness of commercial banks to lend.

We can save the folks at the CSBS and FSOC a lot of time and money by giving them the answer to the stress test ahead of time. In even a modestly stressed scenario, with the fantasy land assumption that the lender banks will walk away from large commercial clients, then the nonbanks all fail. But as we already discussed, that is very unlikely to ever happen. If the banks did not walk away in 2009-2010 or in 2018, just when would that happen?

The mortgage industry is going to have to work with the CSBS and FSOC to address their concerns, real or imagined. In a practical and political sense, the objective of the CSBS has been to get a seat at the table in Washington, with Ginnie Mae and the FHFA, to ensure that any risks from nonbanks are addressed in a reasonable way. The IMBs also need to get a seat at that same table.

The only question is this: Who will represent the political interests of private finance companies, REITs and IMBs in Washington, separate and apart from the interests of the big banks?

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.