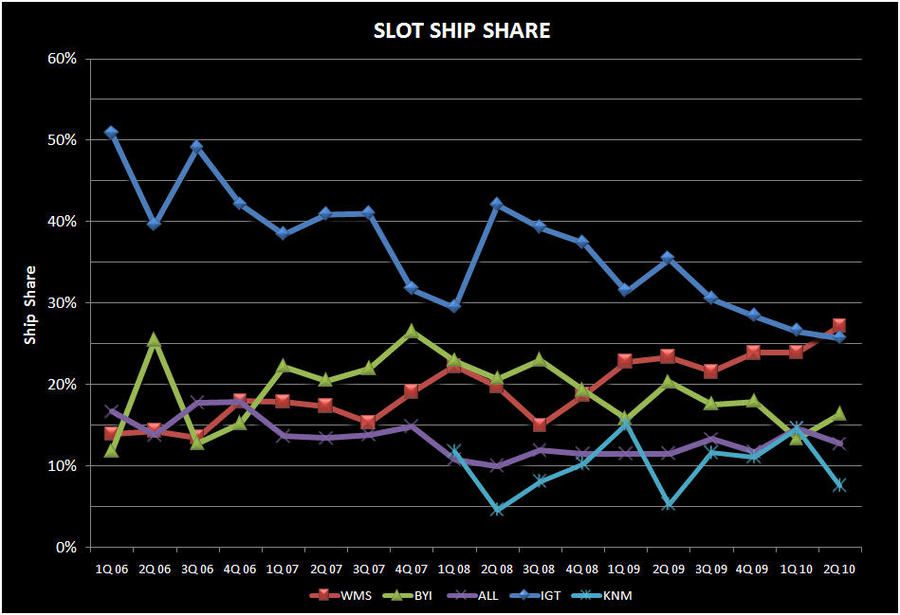

As expected, WMS took the lead over IGT and Konami normalized.

With all the public companies earnings out of way we can step back and take a look a slot ship share trends. Total shipments into North America decreased sequentially to approximately 16k in 2Q10 from an estimated 18.4k in 1Q10.

- We estimate that new and expansion units decreased to 4,750 from 8,700 in 2Q09 and increased from 3,300 units shipped in 1Q10

- Replacements in the quarter were about 11,200, up only 1% YoY and down from roughly 15,000 replacements shipped in 1Q10,

- The June quarter is usually a seasonally stronger quarter for replacements than Q1. As we discussed on “IGT: LOW QUALITY, LOW GUIDANCE, HIGH FCF” published on “07/28,” we believe that several factors in 1Q2010 pulled forward demand:

- IGT’s Dynamix promotion

- Konomi’s FY end March quarter is always seasonally much stronger than their June quarter.

Market Shares

- IGT: 26%, down 1% from last quarter and down from 35% last year

- WMS: 27%, a record ship share quarter for the company. This compares to 24% in 1Q2010 and 23% in 2Q09.

- BYI: 16%, up from 13% last quarter and down from 20% in 2Q09

- ALL: 1H2010 results were at 12%, up 1% from the same period last year

- Konami: 8% down from 15% in 1Q2010; for 1H2010, Konami’s shipshare was 11%, putting it right behind ALL. Konami’s share in 1H2009 was 10%.

Other “Trends"

- The competition for floor share is higher than ever

- For the first time since the 1980s (we think), another supplier recorded higher quarterly shipments than IGT. WMS looks capable of maintaining its share in 25% range (+/- 2%)

- Is 25% the bottom for IGT? Will ship share move converge back toward their floor share (52%) as many investors believe? While they should retake WMS, they days of 50% share are long gone

- BYI share should tick-up over the 12 months as the rollout of its new platform and content commences in 3Q2010. We expect BYI share to stay in the 15-20% range.

- ALL seems to be gaining modest traction with its new Viridian cabinet

The chart below summarizes slot ship share trends: