Is TGT teeing itself up as one of the best large cap growth stories in consumer discretionary, or is this setting up as the mother of all ‘Ackman Assault Hangover’ sucker punches? Our best ideas often stem from internal debate. We’ve got plenty of that here. Here’s the Bull vs. Bear…

Eric’s Bull(et) Points

- Topline has more drivers now, ex-macro, than it has had in some time. The company’s focus on rolling out the 5% rewards/loyalty program and the continued rollout of P-Fresh is accretive to sales. Management says each could be worth 1-2 pts of comp on an annualized basis. Clearly there is something they are seeing in the Kansas City test market (loyalty) and in the P-Fresh remodels to give them confidence. Either way, both company led initiatives offer internally generated sales drivers that others (i.e. WMT) don’t appear to have.

- Traffic is the key here, an TGT clearly has momentum. More food and consumables=more traffic. This also leads to opportunity, which in this case may mean a customer picks up an additional non-food item on any given trip. Probably works.

- Management disciplined about opening new units in this environment, instead using capital to fund .com infrastructure and P-Fresh remodels. We like the conservative approach and discipline in not growing for the sake of growth. Yes international is still on the table, but we suspect that means Canada first. There is no rush here and this is a positive for cash flow.

- Aggressive pricing activity from Wal-Mart seems to be a perpetual thorn in the side of traditional grocers and now BJ’s. However, TGT has clearly found a way to compete effectively. The introduction of the “Up and Up” private label brand and differentiated store and merchandise assortment seems to be keeping Target relatively insulated from pricing pressure issues. Perhaps this past quarter is the best example of this, where core retail gross margins were up 5 bps while WMT and BJ both saw pressure as they took prices down. We don’t need to remind anyone of the trend in grocery margins. The bottom line here is Target’s success away from commodity consumables affords better margins.

- Credit card portfolio risk gradually dissipating for two reasons. One, the overall credit environment is improving leaving opportunity to reduce reserves. Secondly, Target is shrinking its receivables base as tighter credit restrictions and increased government restrictions no longer allow for unabated growth. Target also discontinued its co-branded Visa program, which leaves future receivables growth entirely tied to store sales.

- Expense pressure from investments in dot.com will remain through 2011 as the company carries duplicative costs during the transition away from Amazon (TGT’s outsource partner). The flip side here is we should see leverage on such investments begin to materialize in 2012, the year in which Target.com becomes fully operated in-house.

- Management has clearly articulated the benefits of adding incremental food/consumables sales into their boxes via the P-Fresh remodel. However, the result over time will be lower gross margins and commensurately lower SG&A. Net, net EBIT rate should remain unchanged. While in theory this makes sense, we know that investors are not fully onboard with trading margin for expense savings. Over time, this will become more clear. In the nearer term, headline gross margins could remain under pressure from this mix issue alone.

- While TGT offers a more discretionary play vs. WMT, it also offers greater visibility over the intermediate term in my view. The two strategies currently underway to drive topline results have been tested. We already know that inventory management coupled with differentiated product helps Target to drive a higher EBIT structure than WMT. While the Street may be excited to learn that WMT has dialed back rollbacks (after they didn’t work to drive demand elasticity), the non-consumables part of the story is still very much in limbo. This is the single biggest wild card in the WMT story and one that in our view, has not been answered by a few mid-game personnel changes.

Brian the Bear

One factor I can’t shake is the Ackman Attack. Let’s look at the timeline.

Oct 07-Mar 08: As the credit bubble implodes and sets the stage for the worst economic downturn since the Great Depression, Bill Ackman buys 20.5mm shares of TGT at average price of about $50. By the end of 2009, Ackman owns 3.55% of shares outstanding.

Wanna hear some irony? Ackman’s activist stance was focused on 1) TGT’s outsized risk in credit operations, and 2) lack of accountability and responsiveness in addressing TGT’s valuation. As of latest filings, Ackman has 28.7% of his fund’s assets in TGT (even after having sold down to 2.81% of s/o). Over a third of one fund’s assets on one security??? C’mon Bill. I’ll give you the benefit of the doubt and assume that you aren’t even levered. How ‘bout holding yourself to the same risk management and accountability standards you demand from companies in your ’50-year model’? Give our Macro team a call. They can help you there.

This is more than McGough ranting. I actually do have a point there…

On Target’s May 7 sales release last year, comps were in-line, but more importantly TGT noted that tight expense controls and better gross margins (markups better, markdowns fewer) will lead EPS to be “well above First Call estimates". Credit quality also came in line vs. a trend of coming in slightly below plans. Then, four days later, TGT issued a press release titled “Questions That Attendees May Want To Ask At The Pershing Town Hall.’ In other words, TGT started to pull out all the stops to make Billy go away.

Ultimately, Billy took it on the chin, and lost his proxy battle on May 28 of 2009 after it was clear that the momentum of the business was going against him. The ‘strong cost control’ is particularly notable to me. Being cost-conscious is great – I tell my wife and kids that all the time. But this is a company that has added $1.5bn in revenue (2.5% over 2 years) since The Ackman Assault, but has held SG&A dead even. And yes, that’s despite 9.5% square footage growth over that same period. Last I checked, a new store requires a few bucks.

Yes, TGT is great retailer. No doubt. But my point this is a company where working capital is eroding on the margin, and starting next quarter, the Gross Margin compares get very tough at the same time Target will need to actually start to spend real SG&A dollars to support the much-touted growth initiatives that prompted positive press and sell-side upgrades.

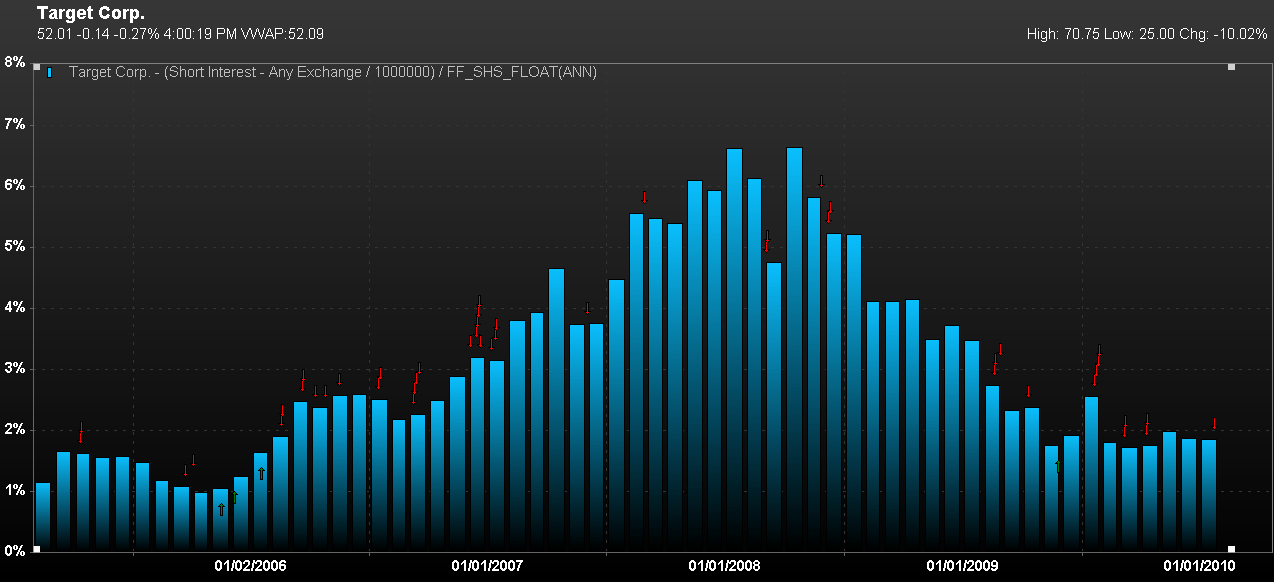

In fact, there’s a sell-side consensus “Buy Ratio’ of 82%. For those of you counting, that’s the most favorable since April of 2000. Yes, 2000. The short interest is down by a factor of 2-3x from the beginning of the Ackman Assault.

If it were not for context that Eric Levine adds to the equation, I’d have the bear claws out big time.

We’ve got more work to do on this puppy.

Keith’s factor models suggest that TGT is bearish TREND with resistance = 53.63.