MGM’s leverage and cash flow troubles are well-known in the credit community. However, it’s not really an imminent issue if MGM can sell its stake in Borgata and IPO a piece of MGM Macau.

Actual free cash flow is negative. Even when MGM’s EBITDA improves over the coming years, much of the increased income will go towards catch up maintenance spend (see 8/22/2010 note, "MGM: MAINTAINING LOW CAPEX").

Since 2006, MGM’s FCF (Consolidated EBITDA pre-ESO less gross interest expense (reported interest expense + capitalized interest)) has been on a rapid decline. In 2006, MGM’s FCF before debt service peaked at $973MM, before declining to $594MM and $410MM respectively in 2007 and 2008. To be fair, the drop is exaggerated by a period of elevated capital expenditure spending. In 2009, despite meager capex spending, FCF before debt service continued to plummet to just $65MM.

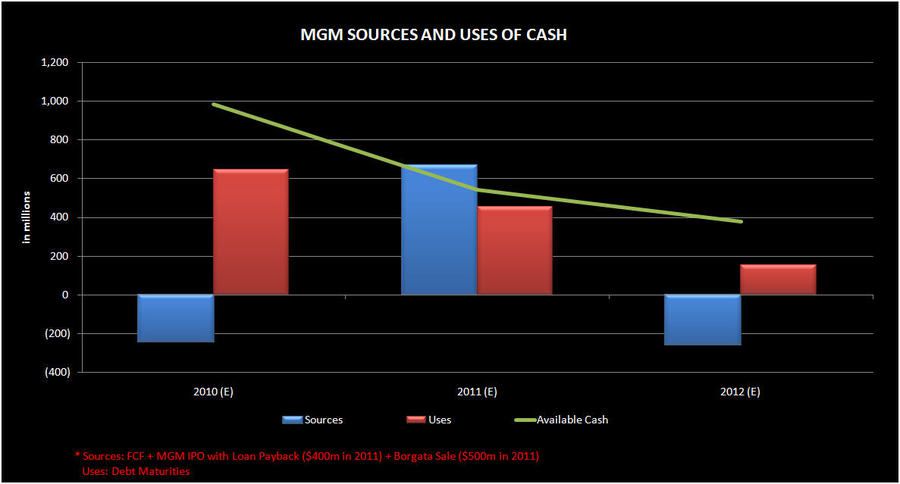

For the next several years, we’re projecting that FCF before debt service turns negative, especially as maintenance capex returns to more normalized levels. Over the next 3 years, MGM could burn through about $730MM of cash before debt service. When you layer in $1.25BN of debt maturities through 2012, MGM's cash burn jumps up to approximately $2BN. However, this in of itself may not be an immiment problem if MGM is successful in selling its 50% stake in Borgata and IPOing part of their stake in MGM Macau in 2011 (including getting back that ~100MM receivable). Although by 2012, even after generating a combined $900 million from these two transactions, we estimate that cash balances fall to uncomfortably low levels of roughly $400 million. In addition, after $1.2BN of MGM's bank debt matures in Oct 2011, they will only have a $3.6BN facility, which we estimate will be fully drawn. Therefore another debt issuance or equity offering seems like a certainty.