In looking over the results out of both Dick’s and Hibbett’s it would be disingenuous to say that we weren’t a bit disappointed. Both came in light on the top-line, each have their respective margin considerations, however, they both raised outlook for the full-year. Rather than looking through the quarter and chalking up favorable guidance adjustments to positive trend momentum and hopeful execution we’ve highlighted the key deltas both in the quarter and 2H as we look forward. For DKS our ‘we’re not against owning it’ positioning remains unchanged, though for HIBB, a lack of upside in margins in the quarter and marginally higher costs curb our expectation for further upside at least in the near-term. As always, our view changes as prices do, but the key is we’ll need to see an improvement in footwear trends as we enter the 2H and as the product cycle starts to pick up meaningfully before these names move up in our queue.

Thematic Call Outs:

Store Expansion: Both players remarked that 2011 will be a year of considerably more aggressive growth relative to 2010. Dick’s expects 30% store growth next year resulting in a reacceleration of square footage growth to a HSD rate up from low-to-mid single digit over the last two years. HIBB also sees opportunity primarily rooted in existing real estate opportunities at Movie Gallery and Blockbuster locations as well as adjacent states. Interestingly, while HIBB maintained its goal of closing 10-15 underperforming stores by year-end, DKS announced that it will be closing 12 Golf Galaxy locations in 3Q – an incremental and positive change that will be immediately accretive to profitability and earnings albeit small. Most importantly, while some will call for Dicks increasing focus on expanding into smaller format stores as a direct threat to the Hibbetts model, the reality is that just isn’t the case. While the new format is similar in size to new Sports Authority stores at ~35,000 sq. ft., it remains well above the average 5,000 sq. ft. Hibbett store and will still be targeted for considerably larger markets.

Category Trends: The bottom-line here is that while all three categories (footwear, apparel, and hardlines) comped positively for both companies, footwear came in softer and is clearly not materializing at the rate we have been expecting. Comps across three key retailers over the last 2-days (DKS, FL, HIBB) have all come in lighter than our expectation particularly those with greater exposure to footwear. While much of the new product that we’ve been highlighting during the year isn’t expected to start hitting floors until now, without commensurate demand sales could be softer yet again in the 2H.

Product: The outlook for basketball appears mixed with DKS far more upbeat reflecting strong momentum with Nike collaborations while HIBB was more cautious on the category citing weak launches as the cause for a challenging 2Q and modest participation in 2H launches. In addition to Nike product, the new Under Amour shoe and Reebok’s Zig remain key launches in basketball. Running continues to be the standout category with both retailers optimistic on toning, particularly in Q4 driven by accelerated marketing initiatives.

In apparel, Columbia’s OmniHeat commands all the buzz. DKS has significantly more exposure to the brand and is positioned to benefit more significantly if consumers believe the technology is as evolutionary as Columbia suggests. Importantly, Hibbetts committed to Columbia earlier this year and expects to have the brand in ~50 stores by year end as compared to some 350 stores in which North Face is carried. This is the most significant apparel launch to note for sporting goods retialers heading into the 2H hands down.

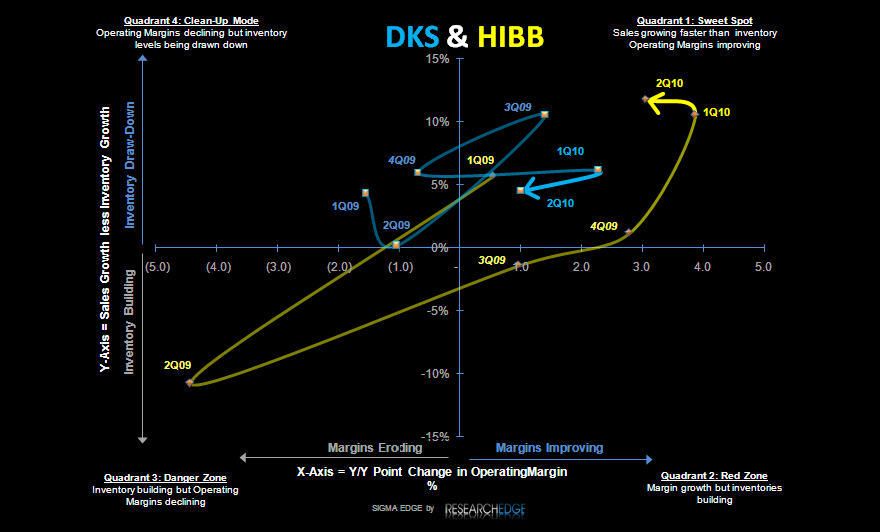

Inventories: As seen in the SIGMA chart below both company’s sales/inventory spread remains positive and little changed from last quarter suggesting that inventories remain relatively clean. While management systems are playing a key role in driving comps with considerably less inventory than in years past, HIBB is further into the process leaving DKS with an opportunity for additional and more meaningful margin gains over the next 12-months.

Company Specific Call Outs:

DKS:

- Mgmt is getting more aggressive on the long-term outlook for the business announcing that after another review, there is an opportunity for 900 DKS stores (up from their original view of 800).

- Will be looking toward smaller format stores to get there (~25% of the incremental 100 oppty).

- Decided to take the pain and shutter 12 of the 91 Golf Galaxy stores that were underperforming in Q3 (too costly, bad local or both) – lots of questions on this, but good call for profitability both near and long-term.

- Chick’s renovation will take another 2-years to complete (longer than expected) to get profitability up to corp. avg.

- Like FL and FINL, DKS also working on concept shops with NKE (Fieldhouse – more premium and Evolution) and initial steps are going very well. Nike recently commented that it’s the best and most complete representation of the brands worldwide. Already have 5 Fieldhouse prototypes operational.

HIBB:

- Comps came in +11.9% with a significant deceleration in July despite easier compares (May up +12.8%, June up +13.3%, and July up +9.5%). However, the first 19 days of August suggest a robust start to Q3 up low double-digits. With August accounting for 40% of the quarter and BTS largely complete management’s expectation of a HSD/LDD comp is better than we were expecting heading into the quarter and an incremental positive.

- While both traffic and transactions were up, average ticket was down.

- Product margins up +60bps in Q2 were ahead of the company’s internal plans though less than we expected given the level of clearance activity during the same time last year. Given the benign promotional environment this is reflective of either an overall shift towards lower priced product, or is evidence that retailers are absorbing higher costs – our gut tells us it’s the later.

- Georgia’s non-participation in the tax holiday season impacted comps by 80-100 bps in Q2.

- Management expects to once again raise its outlook for the full-year again next quarter maintaining that year-end guidance is "very attainable." With Q2 coming in lighter than expectations, our confidence in the 2H is incrementally lower. That said, August trends have been strong out of the gate and account for a disproportionate portion of the quarter.

So where does this leave us – a bit flat-footed actually. We’re adjusting our models for the full year with DKS shaking out at $1.52 and HIBB at $1.51 down from our prior estimates of $1.58 and $1.60 respectively. While both companies raised the outlook for the full-year, confirmation of trends through August from our trend data over the next several week will be critical before these names move up in our queue.

- Casey Flavin, Director