Foot Locker continues to deliver on its strategic turnaround initiatives as evidenced by another quarter of sequential and year over year improvement on both the top and bottom lines. For the bears out there, we are all well aware that same store sales of +2.5% fell short of the Street’s and our expectations (we were at 4.5%). We’re not shying away from the fact that the topline is and will remain a key component of this turnaround. However, the underlying message from the company’s conference call is “profitable growth”. Gone are the days of chasing sales with aggressive promotions, selling commodity apparel at a loss, and building aged inventory over multi-year periods. 2Q results confirm that progress is well on its way towards higher sales and profits, a course which has really only been set in motion for three quarters now. For the bulls, there is plenty to chew on.

- Even at a 2.5% comp increase (in which most regions and divisions hovered around the mean), 2Q marked the first time since 2005 that Foot Locker reported a consecutive increase in comp store sales. It may not be a 5% increase, but consistency is building and the trend is clearly something to note. Importantly, a pickup towards the end of the quarter and in early August gives management confidence to raise the same store sales outlook to a low to mid single digit increase for Q3.

- Basketball not the culprit here. Much speculation was made that the basketball category was extremely weak during the quarter, causing a drag on sales. We didn’t hear anything on the call to confirm this. Management did confirm our belief that on a go forward basis, there is much to be excited about from a product standpoint in the category. The “Big Three” in Miami, Under Armour’s basketball launch, and perhaps even a resurgence from Reebok (ZigTech x John Wall) are all opportunities to drive improvement.

- Elimination of unprofitable and aggressive promotions impacts the P&L in three ways. First, transactions were down mid single digits. Second, ASP’s were up low double digits. Third, merchandise margins improved 210 bps. Part of the margin expansion reflects apparel’s sequential improvement, but the majority is due to lower markdowns, clearance, and promos. This formula is expected to remain in place as higher priced technical running, fewer promos, and a substantial upgrade in apparel (technical and private label) drive profitable sales.

- Many questions from those focused on the past are quick to point out that recent margin gains put overall gross margin rates near peak levels. While factually accurate, we continue to believe there is opportunity to surpass peak for a number of reasons. Most importantly, the apparel category as a whole is currently producing margins BELOW the company average and footwear. Apparel for almost every other retailer on the planet carries a higher margin structure than footwear. This is a huge opportunity for FL and one that is in the early stages of showing signs of life. Apparel comps for the quarter increased by low single digits, a sequential improvement from being down low singles in Q1 and down high single digits in Q409. According to management, the apparel assortment is about 50% towards being upgraded.

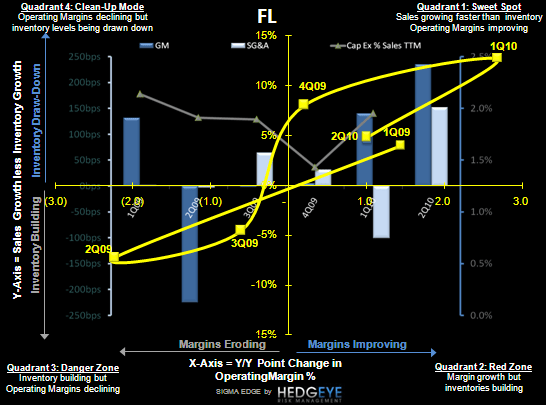

- Inventories remain well controlled, down 5.1% against an essentially flat topline (positive comps offset by shirking store base). We believe this is the one of the keys to the turnaround as the company continues to reduce inventories and increase turns. Recall that in a 10 year history prior to 2009, FL grew sales at a rate higher than inventories every single year.

- Some slight tweaks to the company’s store opening/closing plans. Management is now expected to open an incremental 5 units this year although the capex budget of $110 million remains unchanged. On the flipside, closings may not reach the original goal of 150 units for two reasons. First, some stores slated for closure are showing meaningful improvements in profitability as a result of the product and inventory initiatives put in place. Second, as stores were slated to close landlords appear to be willing to strike longer-term lease concessions at favorable terms. Recall that we have never been in the camp that major store closures were the key to this turnaround. Getting the product, marketing, and sub-brand positioning in our view supersedes the decision to close meaningful amounts of stores.

- Lots of questions as expected on toning. While the category has been a contributor, management was quick to point out that category growth is likely to slow in the back half as the industry anniversaries the hyper-growth of last Fall. Second and more interestingly, FL appears to be more focused on capturing the sales opportunity with the female customer beyond a simple toning purchase. This is particularly relevant for Lady Footlocker, which is the largest female athletic shoe and apparel chain in the U.S. We continue to believe FL is working to build a sustainable women’s business for the long-term and as such, is not over indexing to the toning trend at the current time.

Net, net this was an essentially inline quarter driven by an impressive gross margin performance offset by a slightly weaker than expected topline. There is nothing that we see in the 2Q results that change our view on the opportunity for the company’s turnaround or our above-expectation earnings over the next 12-18 months. We’re tweaking our model a bit to reflect the lower earnings in 2Q relative our expectations, but still stand above the Street at $0.92 for the year. We continue to believe that the opportunities to improve assortment, right size inventory levels, and profitably maximize FL’s market share dominance will unfold over the next 4-6 quarters.

Eric Levine

Director