Summary:

Despite key business drivers performing in-line or slightly better than consensus estimates, the company missed on both its top-line and bottom-line on weaker-than-expected cross-border revenues as traditional T&E spending remains depressed and slow to recover, resulting in the continued, unfavorable mix shift in cross-border volumes towards far lower margin, intra-Europe transactions. In addition, with a smaller domestic footprint compared to rival Visa, Mastercard's near-term challenges include greater exposure to a slower rest-of-world recovery, made worse by the recent re-emergence of global lockdown measures as countries like the UK, Italy, Spain, France, and Germany impose new coronavirus restrictions to battle spiking case counts. Moreover, with worries mounting over new regulatory threats posed by the DOJ's reported targeting of Visa's $5.3B Plaid acquisition, as well as interest from federal regulators into Mastercard's $1B planned acquisition of Finicity, the company's prevailingly positive investor sentiment is being tested.

Like its card network peer Visa, we expect cross-border declines to continue to weigh on Mastercard's revenues over the next 1-2 years, and although we expect the recovery in payment volumes, both foreign and domestic, to moderate in the fourth quarter, we continue to favor Mastercard based on the pull-forward of secular tailwinds resulting from hurried preferences for contact-less, in-person card payments; the accelerated digitization of consumer spending; and the increasingly addressable nature of G2C, B2C, and P2P payment flows. In addition, as we observe a global convergence in central bank policy towards the monetization of government debt used to finance transfer payments to the household and corporate sectors, it is difficult to think of companies better positioned than the card networks with their inflation-hedged, globally diversified revenue bases which can uniquely offset weakness in one part of the world with strength from another while also benefiting from a weaker dollar.

Accordingly, we continue to favor Mastercard's strong and defensible business model, demonstrated by its recurring revenues, superior margins, low capital intensity, and rich free cash flow generation, with the latter evidenced by the company's resumption of its share repurchase program last quarter.

Mastercard shares (MA) remain a Best Idea Long.

The Details:

Mastercard reported 3Q20 non-gaap diluted earnings per share of $1.60, down -25% y/y on a currency-neutral basis and missing the average street estimate for $1.65 - calculated from a set of 32 estimates ranging from $1.49 - $1.75 per share. The company missed across all of its revenue lines, with the bulk of the top-line miss coming from lower cross-border volume fees and transaction processing revenues. Net revenues of $3.8B, down -14% y/y in constant-currency terms and coming in -$160 million below consensus, drove the company's earnings miss with domestic assessments, cross-border volume fees, transaction processing, and other revenue all comparing unfavorably to estimates.

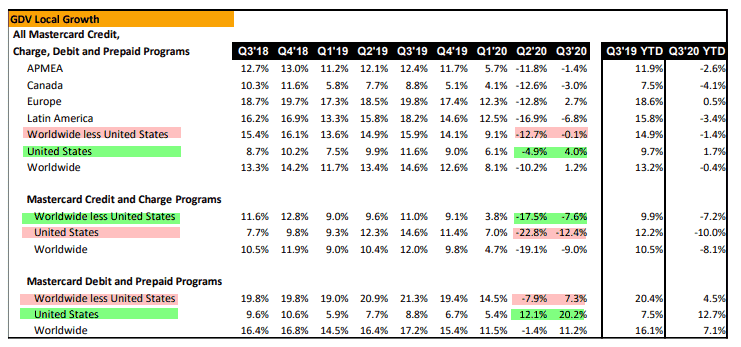

The top-line decline was propelled by a -48% y/y erosion in constant-currency cross-border volume fees, the combined result of a -36% y/y cratering in constant-currency cross-border volume and an increase in the proportionate share of low-yielding intra-Europe cross-border activity. Domestic assessment revenue was up +5 % y/y, +4 point higher than the +1% y/y increase in gross dollar volume (GDV) of $1.6 trillion due to a favorable mix shift towards higher-yield online spending - recall, Mastercard's domestic assessment revenues are based on same-quarter volume, whereas Visa's are based on prior-quarter volume. Although transaction processing revenues recovered +7 pts sequentially to +1% y/y, earned processing fees underperformed the +5% y/y increase in switched transaction volumes with the -4 point difference driven by the same adverse cross-border mix harming cross-border revenues.

Observing the company's GDV more closely, the +1% y/y improvement was driven by strong third quarter domestic volume, up +4% y/y compared to flat volumes in the rest of the world. Domestic credit card volume recovered +10 points sequentially to down -12.4% y/y, offset by accelerated debit growth of 20.2% driven by stimulus checks, enhanced unemployment benefits, and the cash flow positive effects of widespread lender forebearance programs.

Despite rest-of-world debit and credit volumes have respectively lead and trailed the United States in the past, we have seen an inversion of this trend during the pandemic.

In the company's latest update on its key business drivers, we can see global switched transaction volume having remained positive since inflecting in July, led by strong U.S. volume growth. Although the latest week in October shows a sequential acceleration in volume growth, management noted that this is due to the timing of significant promotional activity by an e-commerce merchant and their competitors, suggesting a moderation of growth in mid-October. Meanwhile, switched transaction growth has also held up since inflected positively in July, now tracking +5% y/y higher. Cross-border volumes, however, remain plagued by border closures, with non-intra-Europe activity showing little-to-no signs of recovery as it tracks down -44% y/y as of the week ended October 21.

As is well known, the global depression in cross-border spending is being led by the decline in card-present spending, primarily in the categories of travel, hospitality, and leisure.