Gaming operations used to be a fantastic business for IGT. Now, investment spend is essentially maintenance capex, at best.

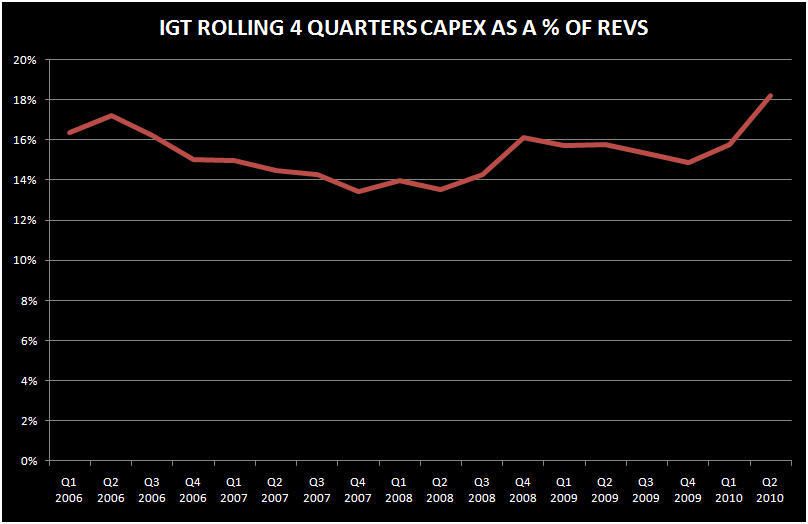

IGT spends about 16-18% of its gaming operations revenues on gaming operations capex. Since revenues haven’t grown, we’d have to characterize this capex as maintenance. Maintenance at best, I should say. We estimate that casino operators should spend 5-7% of revenues on average on maintenance capex. IGT, on the other hand, is up to 18% on its gaming operations business. Certainly, IGT’s gaming ops carries higher EBITDA margins, approximately 500-1,000 bps higher. That’s not enough to offset 3x higher maintenance capex. Dare we say, that gaming operations is not as good of a business as the casino business? At least for IGT, that may be true.

As can be seen in the next chart, capex attributable to gaming operations has been remarkably constant. The problem is that there is not incremental gross profit on the spend. In fact, due to the tough macro environment and increased competition from other gaming suppliers, gross profit has been coming down since 2007. Rolling four quarters gross profit is down $156.1 million or 18.7% from the peak with no corresponding decrease in capex. Capex actually appears to be creeping up lately.

We like the 3-5 year outlook for the gaming supply industry but IGT's gaming ops business needs a boost. The competition continues to get better and IGT remains very reliant on the Wheel line of products. It is difficult to see how IGT will turn this segment into a grower again.