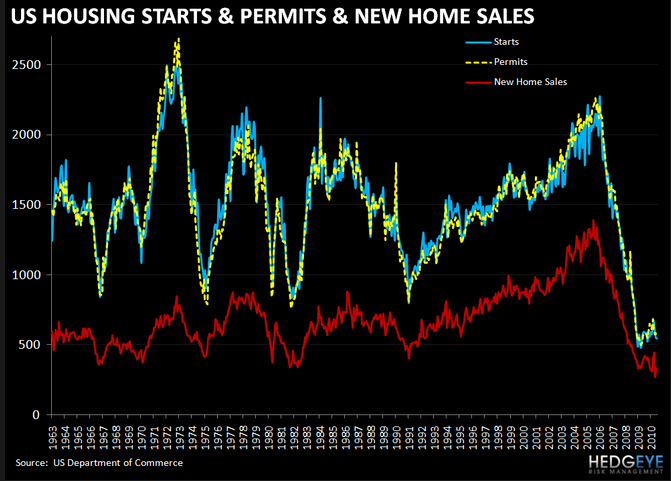

This chart was extracted from Josh Steiner's "HOUSING SUMMIT OFFERS EARLY GLIMPSE OF WHAT MAY COME - STARTS & PERMITS SHOW CONTINUED WEAKNESS" post, yesterday.

This chart was extracted from Josh Steiner's "HOUSING SUMMIT OFFERS EARLY GLIMPSE OF WHAT MAY COME - STARTS & PERMITS SHOW CONTINUED WEAKNESS" post, yesterday.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.