Here are some of our thoughts on both Dick’s and Hibbett’s headed into the Thursday and Friday’s prints respectively.

DKS:

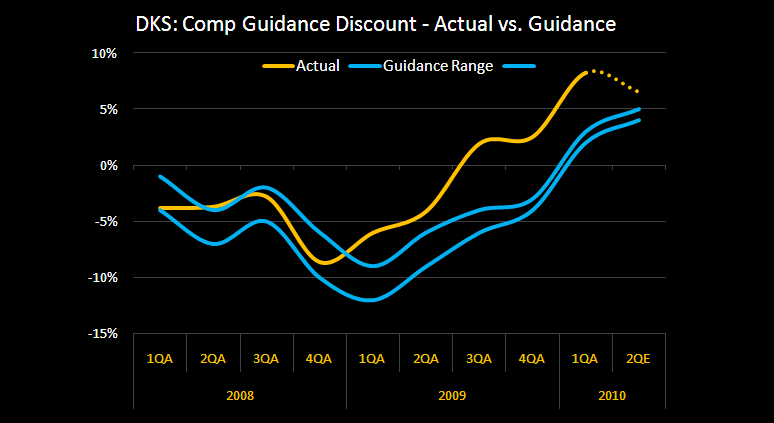

Our view is that the company will deliver on sandbagged guidance again after the close. The setup remains positive with the easiest top-line compare of the year and favorable GM compares. We expect comps to come in ahead of the guided range for the sixth straight quarter though we see the spread starting to compress (see chart below). A strong footwear cycle and benign promotional environment was a positive tailwind in the quarter. Also each qtr that passes leaves more opportunity for cycling investments in .com and planning systems.

- As it relates to EPS – our model is coming in at $0.48 vs. Street at $0.41 and guidance of $0.37-$0.39 driven by comps. Given trends in the channel throughout the quarter, it’s virtually impossible to get to the +4%-5% comp they guided to unless we assume hardlines decelerated at a surprising rate. Weather was little changed in DKS territory relative to last year and other parts of the country. In addition, they are going up against -2% traffic trends and -1%-2% ticket trends in the quarter. After posting a +6.4% increase in traffic on a -2.5% in Q1, we expect similar albeit modestly lower sequential results to drive a +6.5% comp in the quarter.

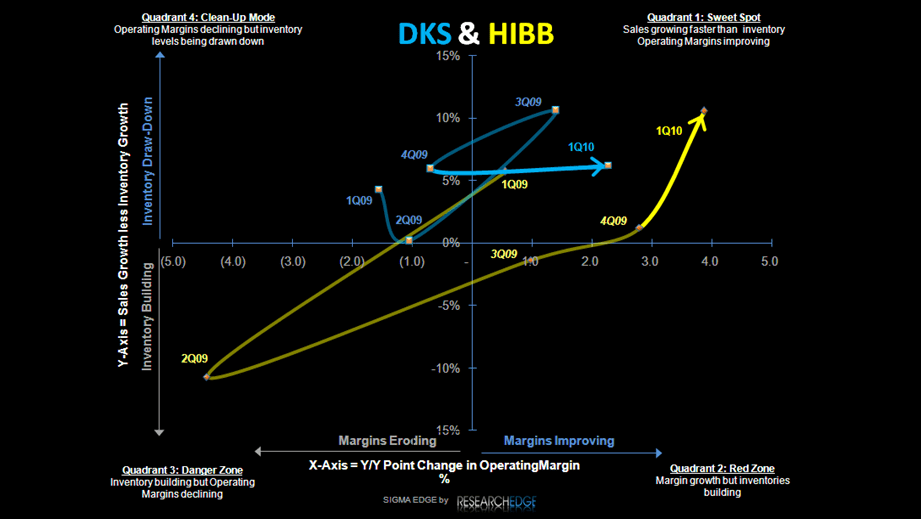

- GM%: +200bps has potential for upside. The sales/Inventory spread coming out of last quarter is in a relatively good position on our SIGMA chart suggesting inventory levels are in good shape. Lapping aggressive clearance activity at both Golf Galaxy and Dick’s and the incremental benefit of World Cup sales could drive upside.

- SG&A: +11% yy continues to be the greatest variable. The company will continue to incur deferred investments in systems to optimize regional product assortment that will add an incremental ~$8mm in the quarter similar to Q1. While nearly 80% of remaining store growth in 2010 is expected to hit next quarter, any acceleration of plans could result in higher incremental preopening expenses.

- Despite a strong 1H, and what is likely to be an upward adjustment to full-year guidance, there’s no reason for Ed Stack to change his (effective) sandbagging style.

For the year, we're at $1.58 vs. Street at $1.46 and guidance of $1.41-$1.44. Next year is $1.75.

Sell-side sentiment is a 70/30 split between bulls/bears compared to 55/45 3-months ago.

Insider activity has been relatively quiet. Short interest remains below 10%.

We don't love the story long term due to its latent rent hurdles due to aggressive growth posturing. But near term, the R&D cycle out of the brands is helping, and that should last at least through CY11. We're not averse to owning this.

HIBB:

The bottom-line is that the company should print something starting with a 2, vs. the Street at $0.16 cents. The setup for the quarter is about as solid as it gets – against the worst comp in company history along with extremely favorable GM and SG&A compares. Consensus estimates equate to a ~14% comp based on our math – we’re at 16%. Like DKS, a strong footwear cycle and benign promotional environment continues to bode well for HIBB.

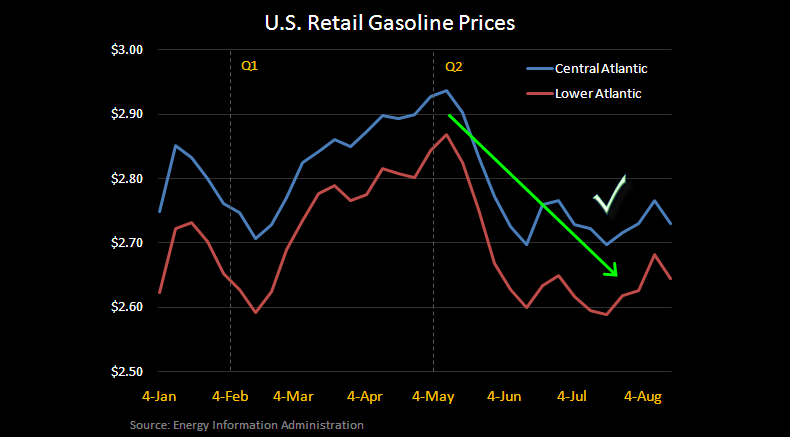

- As it relates to EPS – our model is coming in well above consensus at $0.22 vs. Street at $0.16 driven primarily by comps (we expect the addition of six new stores to add ~$5mm, or 4% to Q2). Sales were strong in the channel based on our trend data throughout the quarter (see charts below) with several incremental data points supporting our expectation for relative outperformance. First, employment figures in the southeast/central have been better than was largely expected driven by a BP funded stimulus. In addition, more favorable weather in Hibbett’s most concentrated regions compared to last year, gas prices that have receded from the critically important $3 level since the end of Q1 to ~$2.70, and both traffic and ticket going up against MSD declines in Q2 FY09 all contributed to regional outperformance as seen in the chart below. Anecdotally, Wal-Mart highlighted that traffic improved sequentially during the quarter – a trend we expect HIBB to confirm given declining comp trends last year down -8% in May, -10% in June, and -14% in July.

- GM%: +350bp could even prove conservative. Sales/Inventory spread ended last quarter in solid position on our SIGMA chart – suggesting that inventories are lean. In addition, the company is lapping a period of aggressive clearance activity that impacted margins by at least 100bps in the year ago period as well as a spike in occupancy expense that accounted for another 130bps. A swing in both of these components along with a benign promotional environment relative even to Q1 could lead to further upside in product margins.

- SG&A: +10% yy. While comping against a significant increase in comp and benefits last year, we expect absolute growth to be marginally higher than Q1 (+9.6%) due primarily to the addition of an estimated six new stores as well as opportunistic marketing spend that management highlighted on the last call. A key variable here is the potential for accelerated store growth should opportunities to acquire additional Movie Gallery/Blockbuster locations become available sooner than expected – not something we expect, but would view favorably as an accelerant to 2H revs.

- Lastly, despite decelerating trends over the last few weeks ahead of BTS, we expect the company to raise year-end guidance for the third straight quarter primarily based on Q2 results.

Q1 YouTube:

"in terms of our guidance, we hope to increase it again in August and then again in Q3, but depends on the macro." – Mickey Newsome

For the year, we're at $1.60 vs. Street at $1.52 and guidance of $1.35-$1.50. Next year is $1.80.

Sell-side sentiment is about 60/40 split between bulls/bears.

Insider activity has been relatively quiet following sales in March. Short interest has come down from 32%, but still stands at a toppy 24% - high for such a good model.

Net/Net, numbers are likely to come in better than expected this quarter for both DKS and HIBB and there are going to be many reasons as it relates to the industry cycle why trends should continue for both players.

Casey Flavin, Director