|

Below is a flashback written by Communications analyst Andrew Freedman on his short Netflix call. We are pleased to announce our new Sector Pro Product Communications Pro. Click HERE to learn more.

|

Ultimately, we believe the positive effect of COVID papered over clear signs of maturation, and we expect these negative trends to resume and be even more pronounced over the next 12-months.

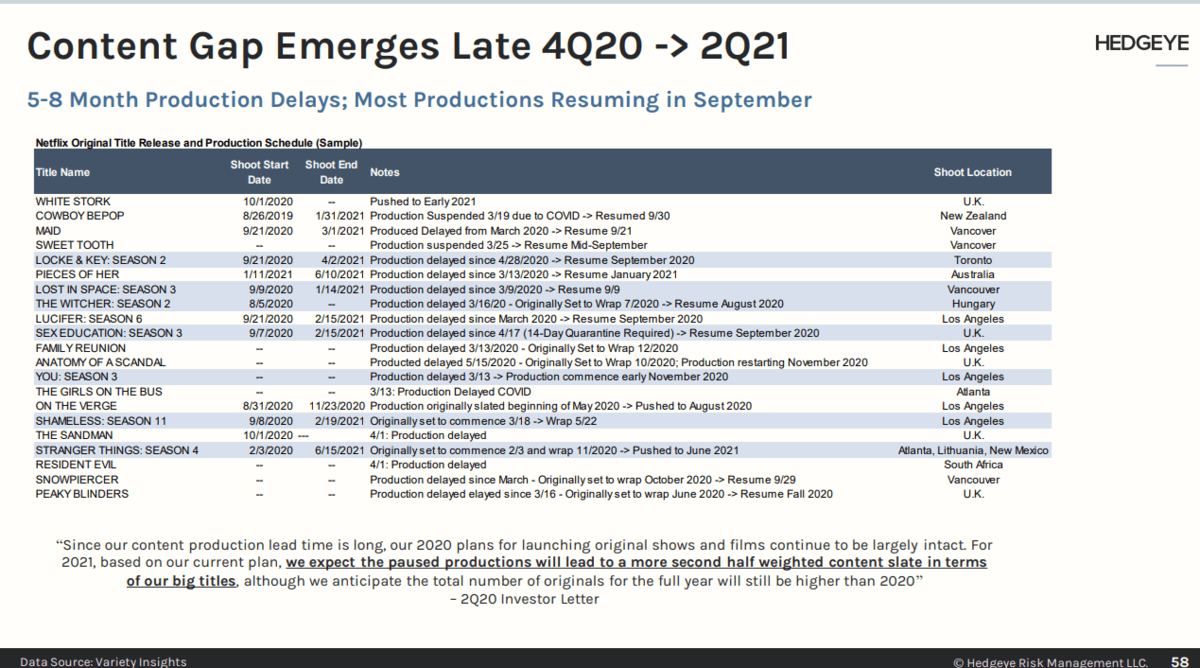

Additionally, we believe investors are (once again) underestimating the threat of rising competition and the inherent risks in Netflix's content/creative strategy. Not to mention the short-term headwinds from production delays.

-

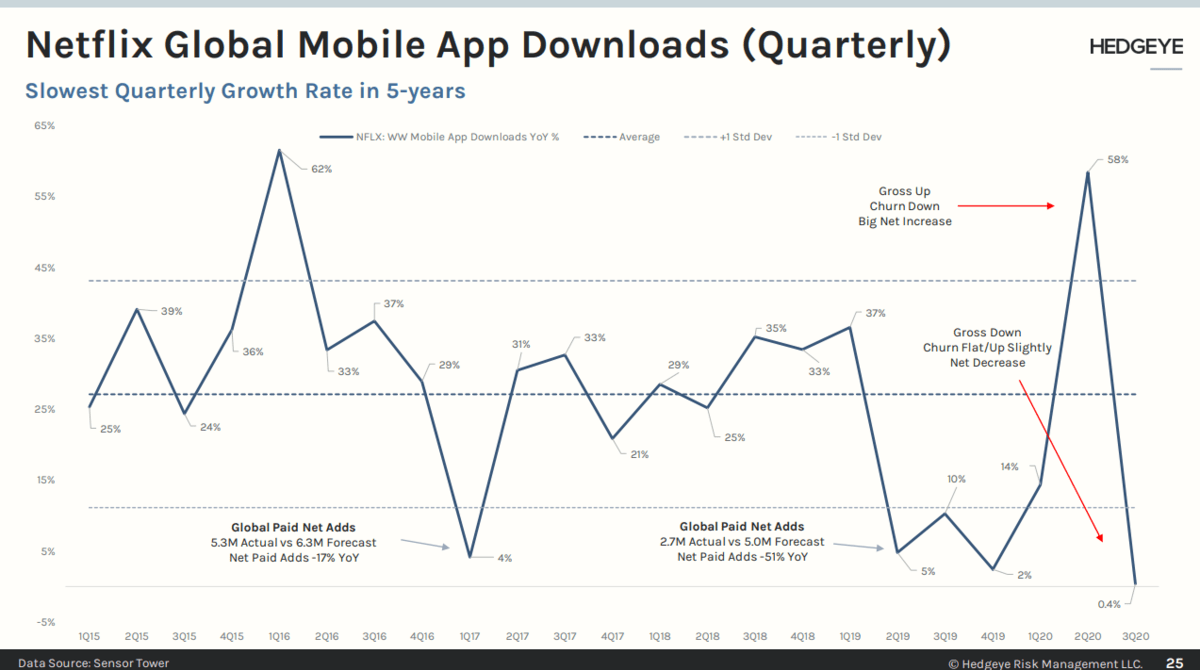

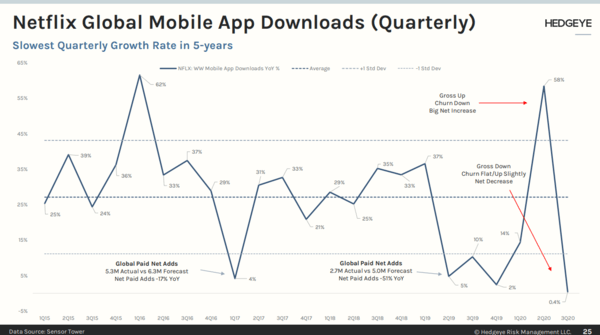

A significant slowdown in gross subscriber acquisition. The app download data is a proxy for gross subscriber adds. Therefore, you have to adjust for churn when thinking about how the data point converts to net. Even if gross is flat YoY, unless your churn rate % is down, your net number will be lower. We believe sell-side calls for a big beat using the app data are missing this point. They are also missing the free-to-paid conversion and mobile-only launch impact.

-

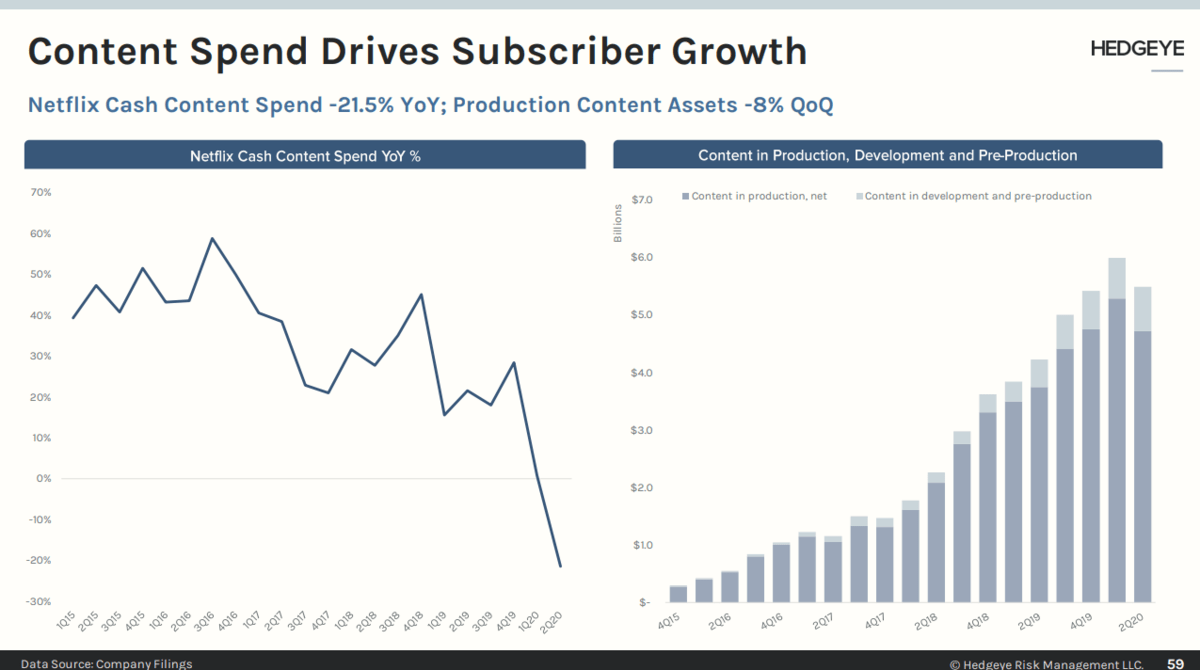

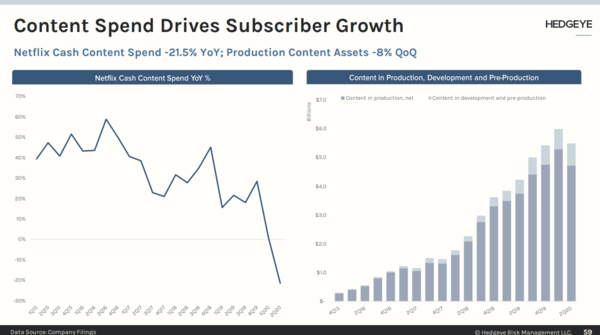

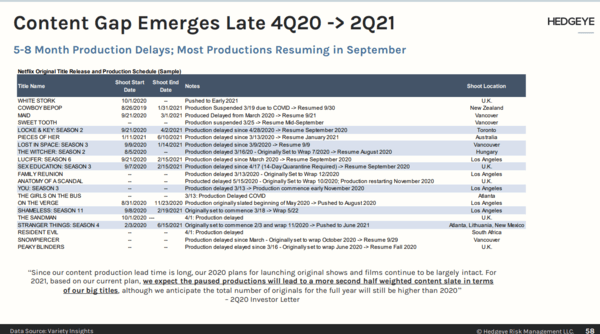

Street leans bullish and mistakingly extrapolating 1H20 trends to 2H20. We would caution folks to extrapolate trends we saw during 1H20 to the NTM. Stating the obvious… but it was a rare situation where stay home at orders pulled forward massive subscriber demand while content spend declined. Historically, content spend leads sub growth. Which is why we expect to see a reversal of the 1H20 trends over the next 6-12 months as slower content spend (-21.5% YoY in Q2) catches up with Netflix (content gap) and result in fewer net adds and higher churn.

-

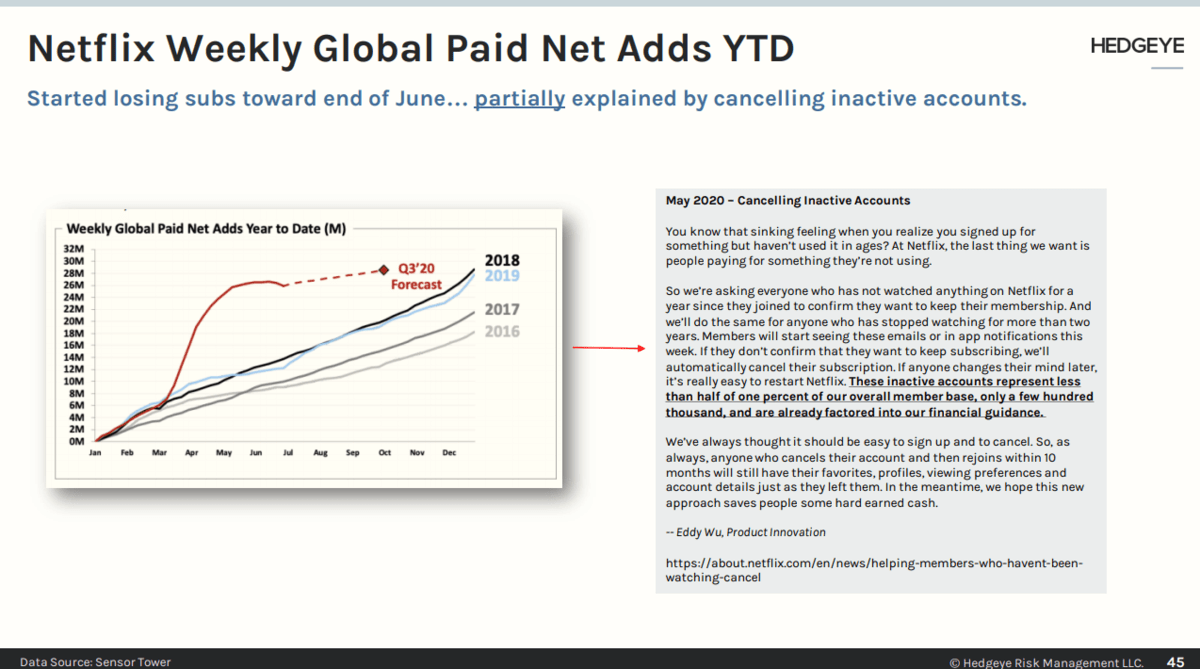

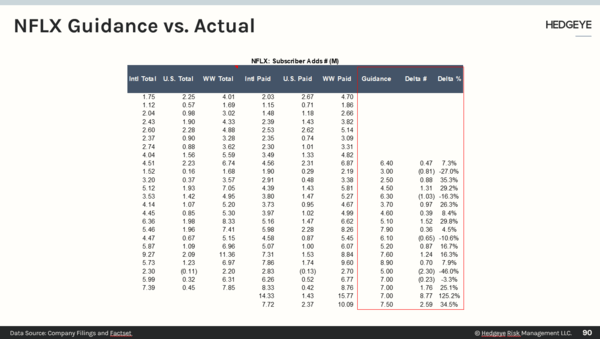

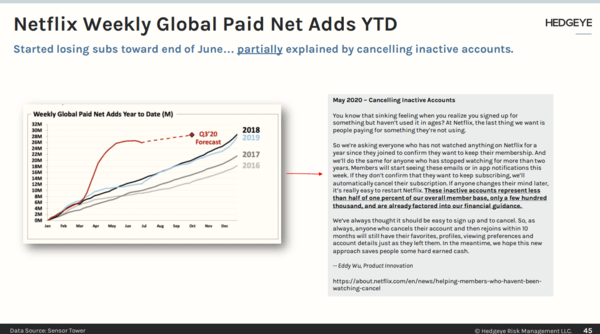

We don't think management's Q3 sub guidance is conservative. Before 1Q/2Q, the average variance on their guide was only 0.3M. We believe investors are assuming management’s guidance of 2.5M for Q3 is conservative, and are pointing to the upside to guidance in 1H20 as evidence. However, to our second point, it wasn’t a normal operating environment so we are reluctant to call it conservative. Especially, given the magnitude of the slowdown we saw QoQ in the app data (a larger sequential decline in the growth rate from Q2->Q3, then an acceleration from 4Q19->2Q20). Maybe management is seeing what we are seeing? Keep in mind, the weekly paid net add chart they show in their letter had them losing subs at the end of June. It would require a pretty significant re-acceleration in growth for them to put up a 4-6M net adds in Q3. The two times they missed guidance in a big way before was when we saw a significant rate of change slowdown in the app data (e.g., 1Q17 and 2Q19).

-

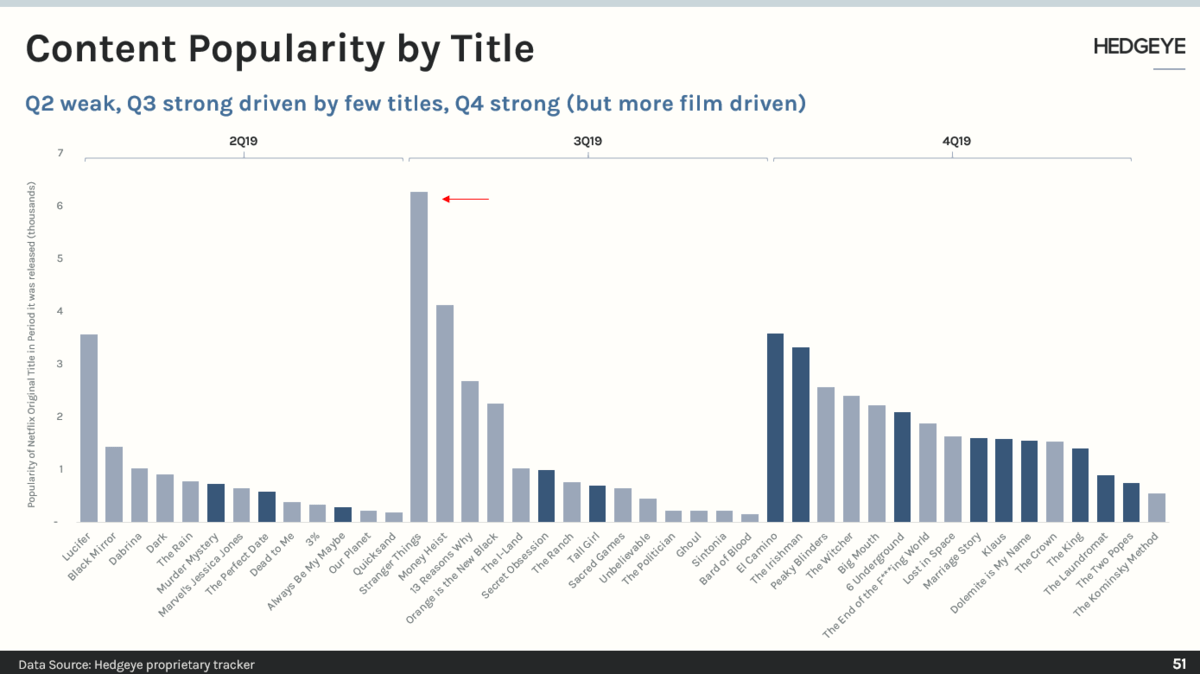

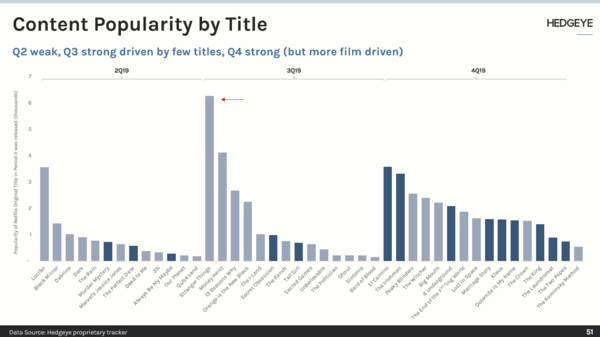

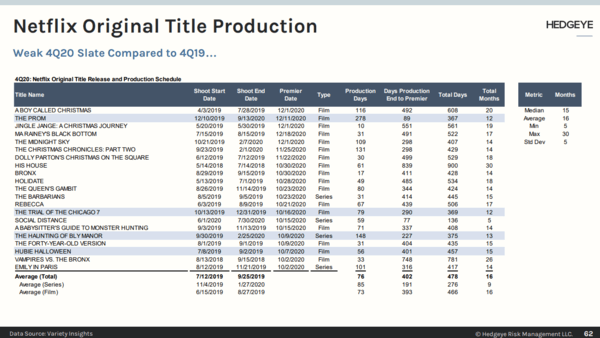

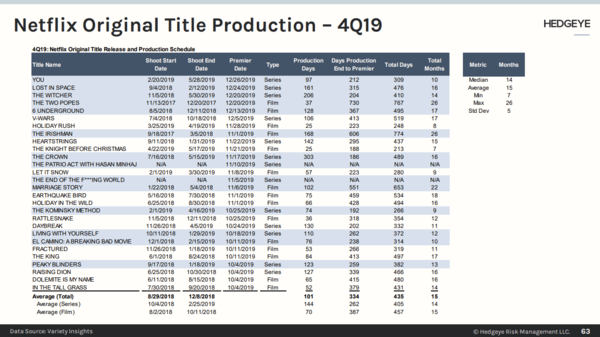

Stranger Things, Money Heist and Sacred Games (India) all dropped in 3Q19, making for a difficult comparison. Netflix also rolled out mobile-only plans in India and began eliminating free trials faster, which we believe positively impacted paid adds by ~1.3M and ~2.7M in 3Q19 and 4Q19, respectively. What does this mean? Well, adjusting for these factors, worldwide net paid adds in 3Q19 were closer to 5.5M versus 6.7M reported. And we know the 3Q20 slate was much weaker than the 3Q19 slate, so we have a tough time rationalizing the bullish 4-6M net adds this quarter. Meanwhile, we have the same dynamic for Q4… where the content slate in 4Q20 is much weaker than the prior period, but Q4 had even a larger contribution from the elimination of free trials. Maybe that is why management decided now is the time to pull the U.S. free trial on 10/6?

-

Everyone we speak with wants to wait until we get closer to the tough COVID comparison next year before considering the short since estimates for 2021 are too high. However, in our view, by the time we get there, it may be the time to get long Netflix as they will be pulling themselves out of the content gap by then. We want to be short as they fall in. Management even said that 2021 is likely to back-half weighted for some of their largest titles. It seems that no one is listening. Or maybe they are and we are wrong in thinking that it will be a big deal.

-

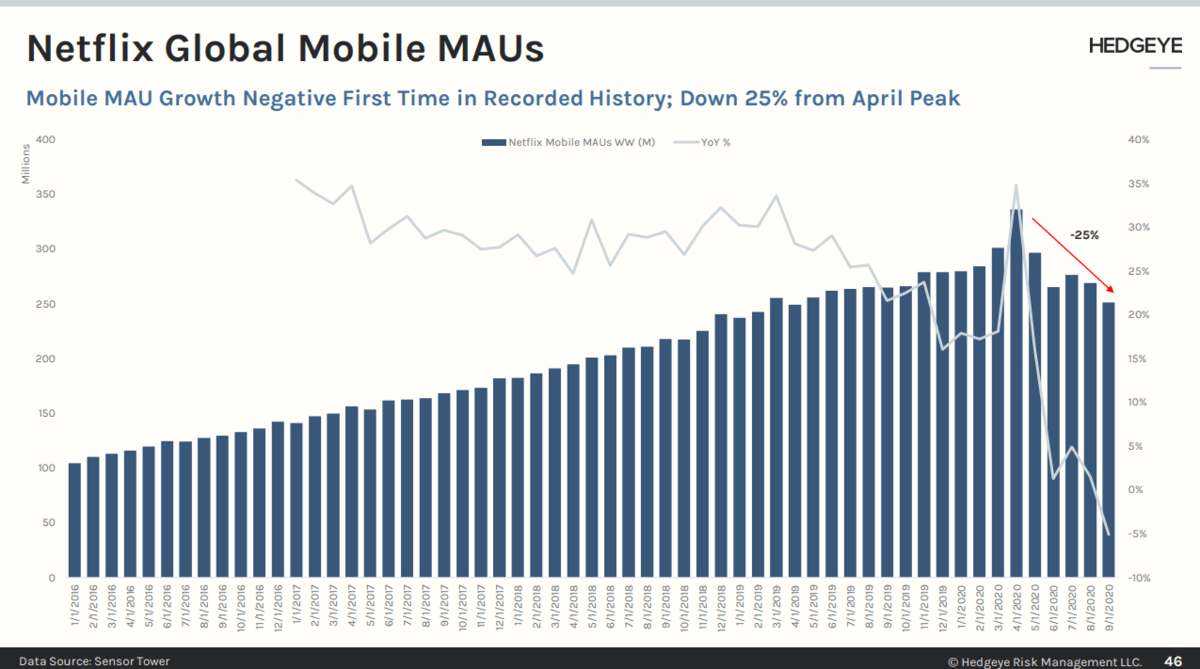

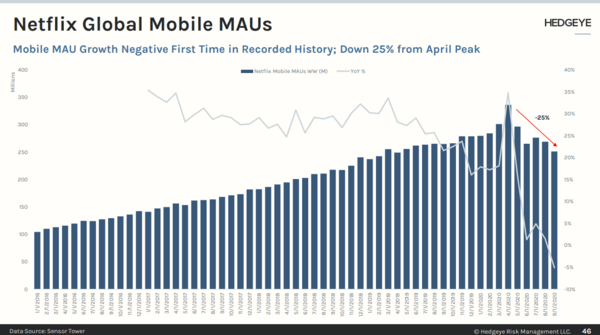

Global Mobile MAUs are down 5% YoY in September and 25% from the April peak. A significant slowdown from where Netflix was growing before and during COVID. This likely reflects a pickup in churn and weaker gross adds at the end of Q2 extended to Q3. Eliminating free trials usually means a higher churn rate of those who were on free trials before and converted to paid. Again, remember that Netflix shows in their letter on the weekly chart, they started losing subscribers in June. The MAU trend also supports the demand pull forward thesis.

-

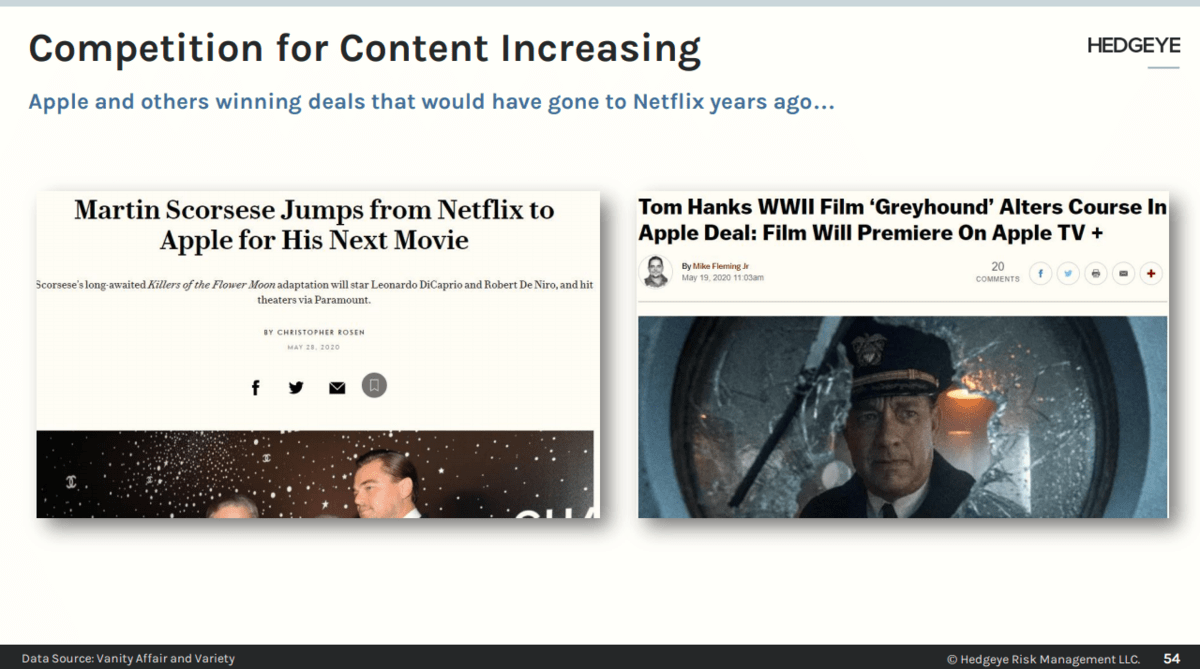

Competition for content is heating up in 4Q20. With the theatrical window shut, we see more content getting released to streaming. Disney made the decision earlier this week to release “Soul” on Disney+ on Christmas, Mulan becomes universally available on 12/4, Season 2 of The Mandalorian drops on 10/30 (with an episodic release that builds mind share over time). We also get WandaVision coming on 12/20. Meanwhile, Amazon just paid $125M to VIAC for streaming rights for Eddie Murphy’s “Coming 2 America” with an expected premiere date of December 18. It seems every day we get another report that Amazon or Apple has outbid Netflix on some deal. This isn’t only our observation, Lucas Shaw, from Bloomberg put out this piece earlier in the week:

“But now that Netflix has transitioned from the upstart to the established power, it’s exercising more control over spending and behaving more like a traditional network. Studio chiefs, producers, and agents all say Netflix is routinely outbid by Apple, Amazon, and HBO Max.”

“While strategically this makes sense for Netflix, there is an argument to be made that it could hurt the company’s reputation. Every week I hear people talk about how the town is getting tired of the company, which is more of a factory than a studio. Executives are impersonal. Shows get lost in the crowd. Netflix doesn’t market anything. Netflix is no longer anyone’s first choice.”

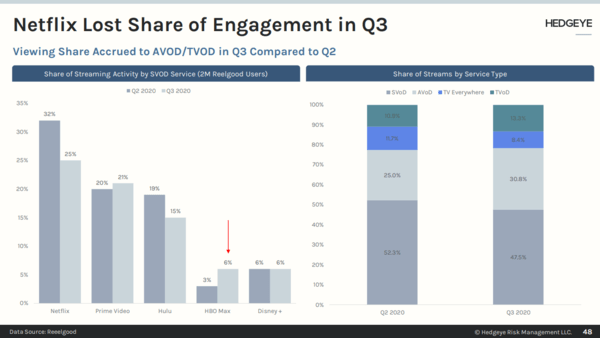

The implications of this for Netflix over time are that they will lose share of OTT streaming hours and engagement to these new services, which will eat into Netflix’s pricing power and subscriber growth. Many of these competing services are a customer acquisition cost (CAC) or retention mechanism for some other part of the business, and therefore don’t need to make money on streaming alone as Netflix does.

|