Today we re-shorted the Consumer Discretionary (XLY) that we covered last week. Our outlook for US consumer spending and housing continues to be bearish for the intermediate term TREND.

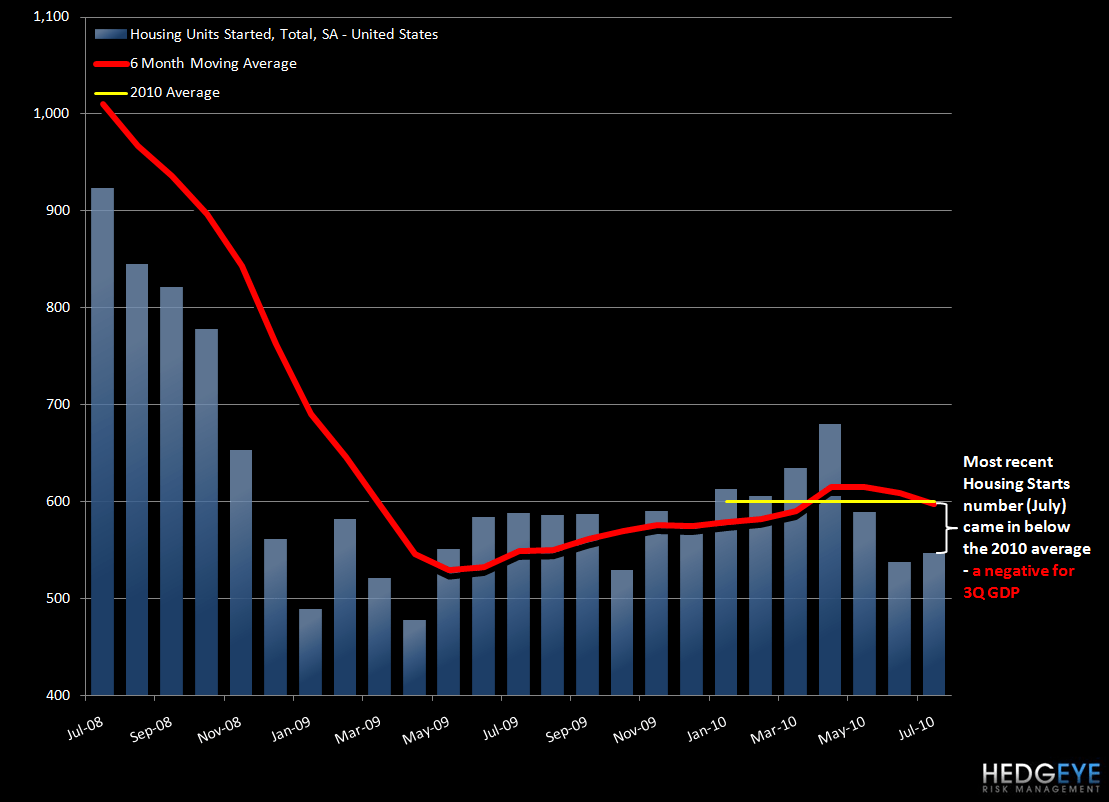

Today the Census Bureau reported very soft July 2010 numbers for housing starts and permits. If it were not for a large downward revision to June’s number, the small monthly gain in July would have been a decline. Furthermore, the actual July number was below the 2Q10 level, suggesting slowing GDP growth in 3Q10. The expectation of a slowing GDP number is also consistent with the retail sales data released last week.

Importantly, this suggests weaker new home sales when the data is released next Wednesday.

With consumer credit continuing to contract and confidence readings trending lower, the downward sequential movement in GDP growth matches up with what the data is indicating. We estimate that personal consumption growth will slow to less than 1% in 4Q10 and that discretionary spending growth will slow to a rate close to what we experienced in 1Q09.

The market is currently bulled up over the improvement in industrial production and the weak dollar reigniting the “reflation” trade. The better-than-expected gain in industrial production came from the seasonally-adjusted auto industry, which increased 10% for the month. This seasonally-adjusted “production of motor vehicles and parts” is a “guesstimate” and is at the discretion of the FED. Not to say they are making up the numbers, but they are making up the numbers. Bernanke needed an upside surprise and he got one!

If you are looking for individual shorts (or longs) within consumer discretionary, the subsectors within the Consumer Discretionary that are the consensus longs (street is too bullish) are Internet and Catalog Retail, Hotels, Restaurant and Leisure and Diversified Consumer services.

Howard Penney

Managing Director