“Not just anyone can float a global currency.”

- Peter Zeihan, Dis-United Nations

Ain’t that that truth, Peter. Not just anyone can get all of Global Macro markets addicted to Down Dollar inverse correlations either!

After signaling immediate-term TRADE #overbought on Thursday of last week, it’s back to Down Dollar #Quad3 speculation on a big US “stimulus” announcement by Tuesday of this week. It’s a good thing people aren’t forced to be super short-term out there.

After 3 straight down days, I got very long of stahks! on red on Thursday/Friday, so personally I’m thoroughly enjoying this volatility.

Back to the Global Macro Grind…

Welcome to a critical Macro Monday @Hedgeye where I’ll review how last week’s Dollar Up move provided plenty of weekly alpha for anyone who was positioned for it. In addition to September’s discounting of rising #Quad4 probability, was that it for #Quad4? I don’t know.

To contextualize where the world’s at in Global Currency terms:

- US Dollar Index had a #Quad4 week +0.7%, taking its 1-month gain back to +0.5%

- EUR/USD signaled immediate-term TRADE #oversold, down -0.9% on the week and remains Neutral TREND @Hedgeye

- Yen was +0.2% vs. USD last week and remains Bullish TREND @Hedgeye

- GBP/USD corrected -0.9% last week and also remains Neutral TREND @Hedgeye

- Brazil’s Real depreciated another -2.0% vs. USD last week and is down -7.3% in the last month = Bearish TREND

- Russia’s Ruble was down another -1.4% vs. USD last week and is down -3.7% in the last month = Bearish TREND

- Aussie Dollar broke down -2.2% vs. USD last week and is down -3.1% in the last month = Bearish TREND

In other words, while this morning will be a fun one to be long big USD inverse correlations, there’s still plenty of scope here (i.e. if the US Dollar makes another higher-low vs. the one it made during #Quad3 in AUG) for global currencies like Euros, Reals, and Rubles to break-down…

That’s why on #Quad4 being fully priced in, I say I don’t know. What I do know is where that risk is trading, every minute of every day.

One of the big TAAS (There Are Alternatives to SPY) macro markets to be paying acute real-time attention to is the Commodities market. There were mixed signals on #Quad4 there last week too:

- CRB Commodities Index was down -0.2% on a Dollar Up week but is +1.2% in the last month and still signaling Bullish TREND

- Oil (WTI) was +0.7% on the week and is also +1.2% in the last month = Bullish TRADE duration, but still Bearish TREND

- Copper corrected -0.5% on the week but is +0.2% in the last month and remains Bullish TRADE and TREND

- Corn inflated another +1.8% last week and is +8.1% higher in the last month signaling Bullish TREND alongside most of Ag too

- Lumber deflated -4.2% last week and is down -12.7% in the last month breaking bad to Bearish TRADE and Neutral TREND

- Cattle deflated another -3.5% last week and is -8.7% in the last month also breaking bad to Bearish TRADE and Neutral TREND

Lumber & Cattle are interesting signals if only because they were both early in signaling Bullish TRADE and TREND breakouts when we initially made the Long Commodities Asset Allocation call back in June. When you pay deliberate attention to everything that moves, it’s easier to see.

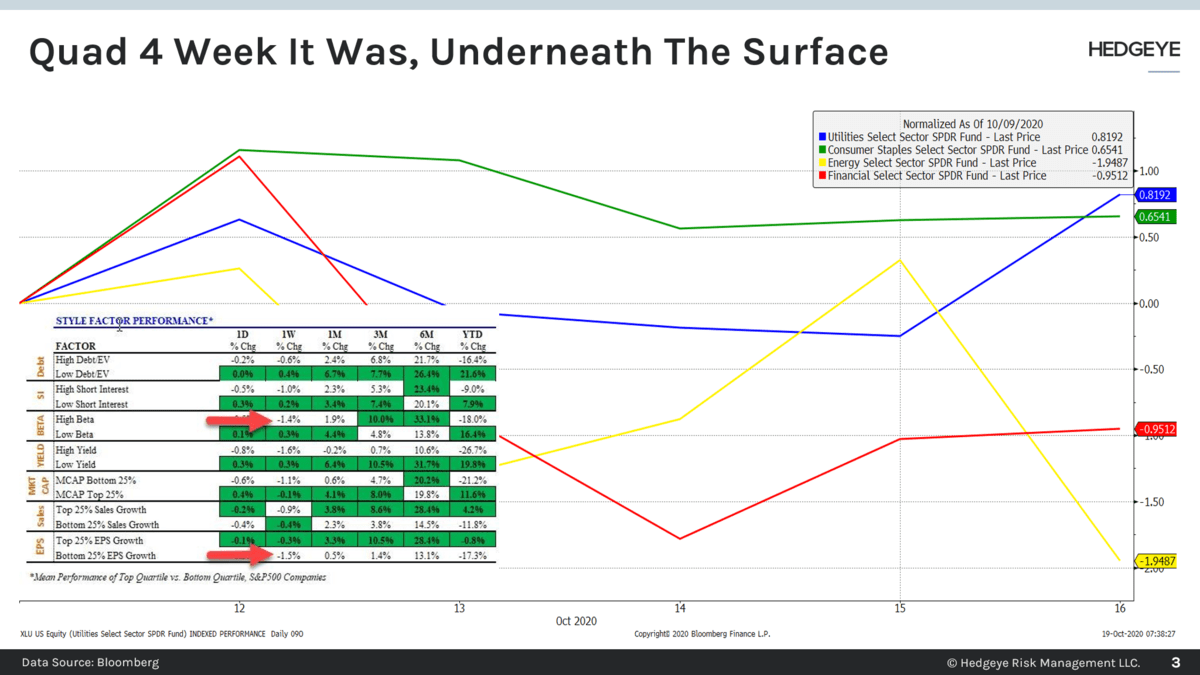

Meanwhile, in US Equity Sector Style terms, it was very much a #Quad4 week:

A) Energy (XLE) and Financials (XLF) were down -1.9% and -1.0% on the week, respectively (both are #Quad4 Shorts)

B) Utilities (XLU) and Consumer Staples (XLP) were up +0.8% and +0.7% last week (both are #Quad4 Longs)

Utilities (XLU) are interesting because they work during both #Quad3 Stagflation and #Quad4 Deflation. That’s probably why they’re the best US Equity Sector to be long of here so far in Q4 at +7.8% for OCT to-date.

The big question for both Utes (and Gold), from here, is whether the Fed’s largest bond buying week since May is going to cap US Treasury Yields around 0.81-0.82% (i.e. the top-end of my Hedgeye Risk Range). If they don’t, the MOVE (treasury vol) is going to move!

Last week saw the UST 10yr Yield fall alongside Global Yields (Germany’s Bund Yield collapsed on Germany being in #Quad4 in Q4) with UST 10yr down -3 basis points to 0.75% and High Yield OAS Spread widening +2 basis points to +471bps over Treasuries.

What else mattered last week? Our long/short setup in Global Equities continued to work, despite the Dollar Up week:

A) Chinese Stocks led major Global Equity market winners +2.0% on the week and +1.6% in the last month

B) Spanish Stocks led major Global Equity market losers down -1.5% on the week at -3.7% in the last month

At down another -2.7% last week and -9.5% in the last month, Russian Stocks (RTSI index) were signaling that #Quad4 in Q4 is clear and present danger too. So just keep that in mind as I may very well be out of my #Quad3 USA position by Tuesday!

Stay nimble, my friends.

Immediate-term @Hedgeye Risk Range with TREND signal in brackets:

UST 10yr Yield 0.68-0.81% (bearish)

UST 2yr Yield 0.12-0.16% (bearish)

SPX 3 (neutral)

Tech (XLK) 115.50-125.33 (bullish)

Utilities (XLU) 60.18-64.81 (bullish)

Financials (XLF) 24.23-25.60 (bearish)

Shanghai Comp 3195-3401 (bullish)

Nikkei 235 (bullish)

VIX 23.99-29.69 (neutral)

USD 92.89-94.15 (neutral)

EUR/USD 1.16-1.18 (neutral)

USD/YEN 105.00-106.09 (bearish)

GBP/USD 1.28-1.31 (neutral)

Oil (WTI) 39.12-41.89 (bearish)

Gold 1 (bullish)

Copper 2.94-3.12 (bullish)

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer