A different deal making cycle beginning? (NESN)

Nestle has now kicked off its North American water brands, Pure Life and Poland Spring. The brands are said to fetch about $5B based on sales of $3.7B and core earnings of $600M.

Arbor Investments, which has backed food and beverage brands in the past, including Gold Standard Baking, Artisanal Brewing Ventures, and deli meats producer Columbus Manufacturing, raised $1.67B for its largest fund to date, targeting investments in the food and beverage industry. Arbor sees an increase in corporate carve-out opportunities from large public companies seeking to divest brands “that have gotten stale.” Several companies could seek to sell some non-core brands to Arbor, including but not limited to Hain Celestial, Conagra, J.M. Smucker, SunOpta, and General Mills. A divestment can boost the company's future growth rate, but it has almost no risk compared to an acquisition.

Several other SPACs could announce acquisitions in the consumer staples sector, including Gores Metropoulos (GMHI), Pershing Square Tontine (PSTHU), Yucaipa (YAC), and PMV Consumer Acquisition. Instead of mergers and acquisitions, could we be beginning a cycle of SPAC IPOs and divestments?

Bar closures, across the pond for now (BUD)

A month ago, Dr. Fauci said restaurants and bars should stay closed. Since then, the percentage of local bars closed fell slightly to 33% on October 4th from 37% a month earlier. The following chart from Womply (a CRM provider) shows the very gradual reopening rate for local bars in the U.S. Europe is taking steps to place restrictions again due to the second wave of increasing infection rates. The Netherlands closed bars and restaurants last week. Brussels closed bars for at least a month, and Paris closed bars for at least two weeks. In expectation of additional restrictions delaying the recovery, we lowered shares of Anheuser Busch InBev on our long bias list last week. Heineken, Carlsberg, and Molson Coors are all negatively impacted by the headwind to the on-premise business.

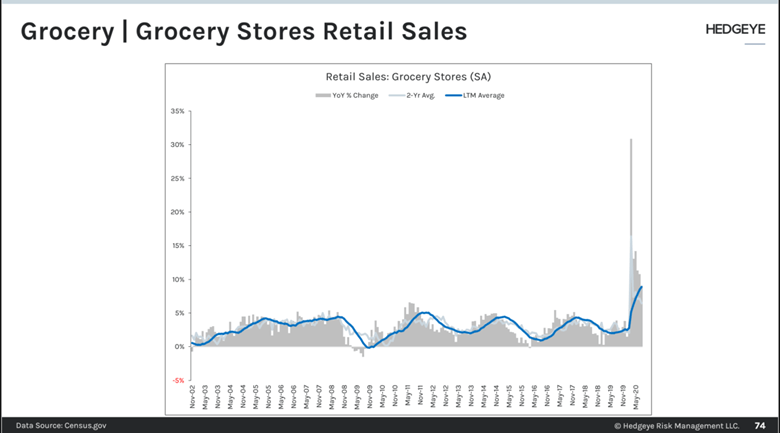

September retail sales accelerate for grocery and restaurants

On Friday, the Commerce Department reported that retail sales increased a seasonally adjusted 1.9% month over month in September. Retail sales grew 5.4% YOY in September on a seasonally adjusted basis. Unadjusted sales (how our companies report results) fell 2.8% in September. Grocery stores sales grew 9.6% YOY, accelerating from 8.6% in August on an adjusted basis, as seen in the following chart. Grocery store sales grew 10.5% YOY in September on an unadjusted basis, accelerating 7.2% growth in August. Warehouse clubs and supercenters reported growth of 4.5% unadjusted in August in comparison (September will be reported next month). Food services and drinking places grew 2.1% month over month and decreased 14.4% YOY in September on an adjusted basis. That compares to 4.3% growth MOM and -15.7% YOY in August. On an unadjusted basis, food services and drinking places fell 13.7% YOY in September than -17.4% in August. Grocery sales continue to outperform expectations despite an improvement in restaurant spending and a drop in government transfer payments.