APHA is a Best Idea SHORT on the Hedgeye Cannabis Best Ideas List. We elevated APHA from our SHORT bias list to a Best Idea SHORT in October 2019.

APHA, like a number of the larger Canadian LP's, is struggling under the weight of mismanagement and an extremely challenging operating environment in Canada. Excess inventory and lower retail pricing will be a theme for all the companies to contend with for the foreseeable future. Despite some players scaling back cultivation, the 5-6 week growth cycle for an average cannabis plant will only make the inventory issue more challenging until the retail store base's growth allows for increased consumption in the legal market.

Yesterday, APHA reported fiscal Q1 net revenues of C$145.7 million vs. FactSet C$159.6 million, missing consensus estimates by -8.7% and posting a sequential decline of 4.3%. Net cannabis revenue grew 17.8% QoQ and 103% YoY to C$62.5 million, while distribution revenue fell -17.1% QoQ and -13.8% YoY to C$82.2 million. The company attributed the top-line decline to lower distribution revenue at CC Pharma in Germany, with COVID-19 reducing the number of in-person visits to physicians and pharmacies. Net loss per share was C$0.02 vs. FactSet C$0.03, a slight beat. The company posted gross revenue for adult-use cannabis at C$69.6 million.

Adjusted cannabis gross profit increased to C$31.5 million in 1Q20 compared to C$28.1 million in 4Q19. Adjusted cannabis gross margin was 49.7% in 1Q20 versus 52.9% in 4Q19. The increase in adjusted cannabis gross profit dollars and decrease in gross margin was primarily due to the release and pipeline fill of large-format products and B!NGO, an economy brand utilizing lower potency cannabis, which provided an increase in sales, but at a lower margin than APHA's premium branded products. The company is guiding to gross margins staying in the 50% to 54% range, but those will be hard to sustain as retail pricing declines.

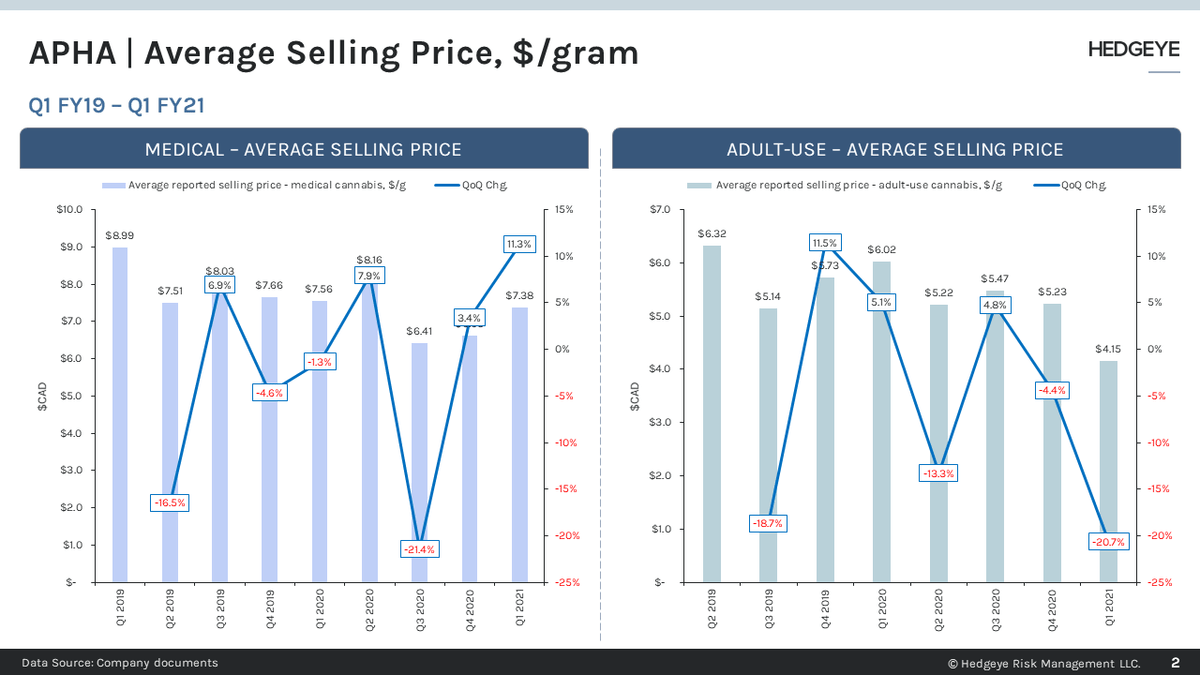

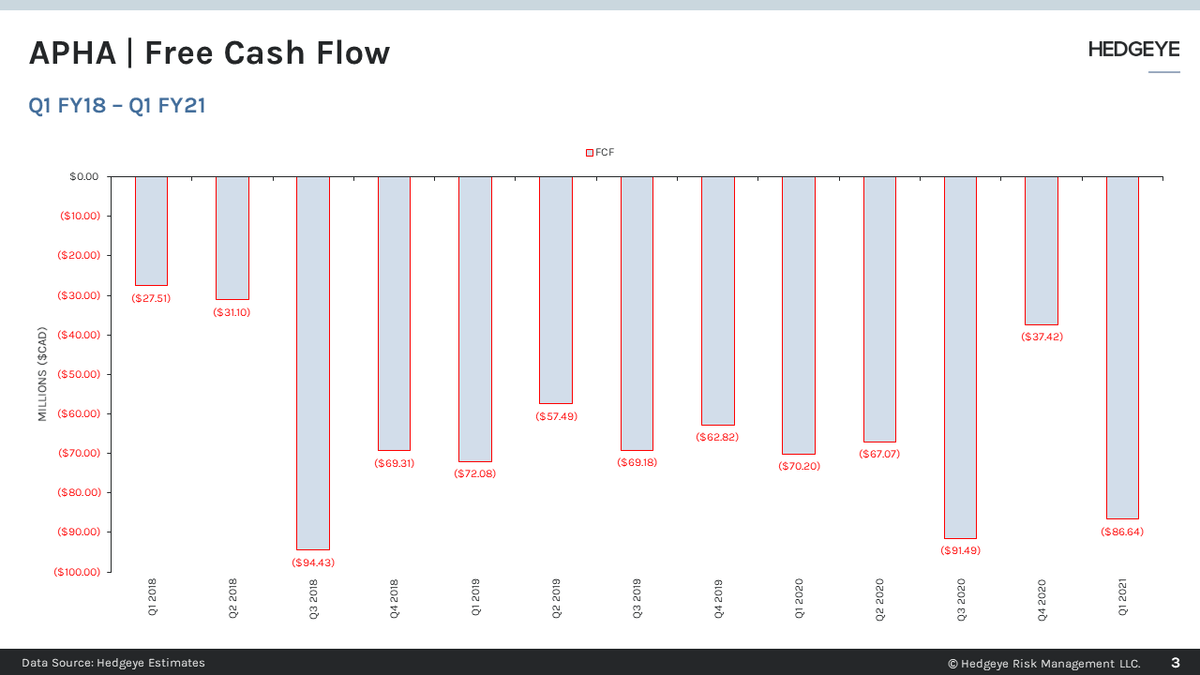

Inventory grew 21.6% QoQ to C$321.3 million, which puts APHA's inventory turnover ratio on an LTM basis at 2.1x – a year ago, it was 3.4x. Given the supply issue that has plagued Canadian LPs, future write-downs and impairment charges seem inevitable. APHA continues to post negative Operating Cash Flow at -C$69.3 million compared to -C$9.4 million in the prior quarter. This worsening burn-in OCF is coupled with its cash position, decreasing to C$400 million compared to C$497 in the preceding quarter. The average selling price of medical cannabis increased by 11.3% QoQ. However, the average selling price for recreational fell to C$4.15, marking a decline of -20.7% QoQ and -31.1% YoY. Management likewise attributed the sequential deterioration as a result of the initial pipeline fill of new large-format offerings and the introduction of B!NGO. As we noted back in July, declining ASP with an inventory buildup is not a good set up.

As the Canadian market progressively shows improved sales figures and an increase in store openings nationwide, APHA has grabbed significant market share. For August 2020, management reported that "Aphria ranked as the number one LP for sales in the brick-and-mortar retail channel across all brands in Ontario and Alberta." Yet, for Aphria's leading market share, its financial performance continues to be lackluster.