R3: REQUIRED RETAIL READING

August 16, 2010

The results out of LOW this morning were slightly off the mark, but not beyond the realm of expectations. For now the gradual fade is visible. But as 2011 brings with it a likely double-dip in housing – this story could look very different.

TODAY’S CALL OUT

One of the more obvious conclusions coming out of our conference call and Black Book on housing’s impact on retail related to the headwinds the home improvement retailers should face in 2011. Yes, I know. You don’t need to be a rocket scientist to make that conclusion. With Lowe’s reporting this morning, we get a glimpse into where the DIY/Home Improvement sector is heading, and for now, it’s not that surprising. The stock might be up on the number relative to expectations. But let’s face some facts… comps decelerated on a 1 and 2 year basis for the first time in 6-quarters, and earnings were down 10% on 3.7% sales growth. At face value, can someone rationally tell me why this is acceptable?

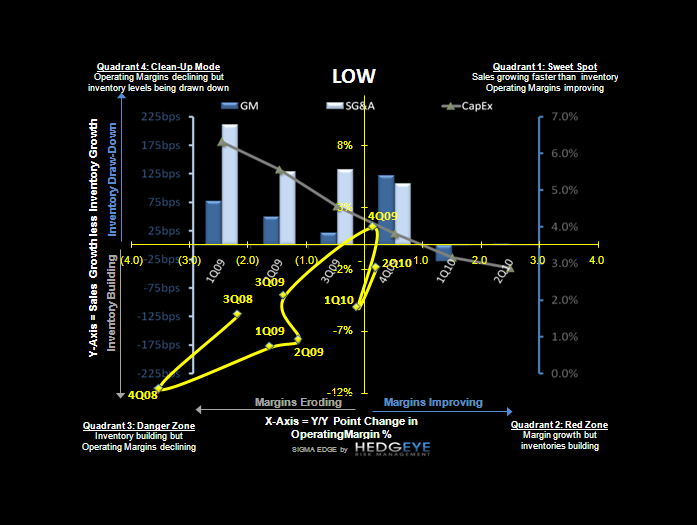

The one area that LOW had in its favor was inventory management. While still growing faster than sales (in 7 of the past 8 quarters), the sales/inventory ratio (see SIGMA chart) sequentially ticked up this quarter, which explains away the little squeeze in the stock today.

But the only real catalyst to get this name higher will be cash flow momentum – which is not there (especially vis/vis Home Depot), and/or a true underlying rebound in the housing market. As we gain confidence along with our Macro and Financials/Housing team that a double dip in 2011 is increasingly likely, can someone explain to me why LOW can’t have a down year AGAIN, and then AGAIN? Note: The Street has 12% EPS growth baked-in to this model for the next 24 months.

- Eric Levine, Director

LEVINE’S LOW DOWN

- JC Penney noted the early customer response to the company’s Liz Claiborne launch has been “overwhelmingly positive”. Interestingly, the brand has not been officially launched, as marketing efforts are slated to begin in mid-September. Unfortunately, a couple of weeks worth of data, while positive, is too limited to draw a conclusion on the ultimate success of the launch.

- Fashion blogs are abuzz with Talbots latest marketing campaign. As the company continues its transition towards a more youthful (not teen, but younger) image, the latest print ads featuring Linda Evangelista are out and gathering attention. The next step is to see if the marketing shift will translate to a sustained pick up in fall sales as “tradition is transformed”.

- While e-commerce may still present one of the greatest opportunities for growth for the retail sector in general, it does not look like it will be driven by further broadband adoption. After several years of uninterrupted growth, consumer use of high speed internet access at home appears to be hovering around 66% of American adults. This represents a small (up 5%) increase from the prior year and the smallest increase in seven.

- If you thought holiday sales promotions came early last year, the “Christmas Creep” will be upon us even earlier in 2010 according to an annual benchmark report from Experian Marketing Services. While Target’s “Black Friday in July” sales appeared aggressive at the time, we can expect more of the same from other retailers looking to capitalize on early movers as consumer spending trends become increasingly less certain heading into the 2H.

MORNING NEWS

Long Beach Port Cargo Traffic Increases in July - The monthly container cargo count at the Port of Long Beach increased for the eighth straight month in July 2010, rising 35.8%. Imports were up 32.5%, while exports rose 16.4%. Empty containers, which are mostly bound overseas for refilling, were up 63.1%. <polb.com/economics>

Hedgeye Retail’s Take: Despite concerns over consumer spending in the 2H, container traffic continues to suggest retailers are betting on stronger demand heading into the holiday sales season.

Cotton Climbing Higher to 1995 Peak - Cotton may climb to the highest price since 1995 as rising demand in emerging markets for everything from shirts to bed sheets forces textile makers to restock inventories that are the tightest in 13 years. Export sales by the U.S., the largest shipper, are off to their fastest start since 1993 as apparel demand in China, the biggest consumer, increased 24%, government data show. Cotton may advance 13% to a 15-year high of 94.9 cents a pound before new supplies are harvested in October, according to 17 analysts surveyed by Bloomberg on Aug. 12 and Aug. 13. The commodity is projected to extend its gains because demand is growing in Asia’s developing nations, even as signs emerge that the U.S. economic recovery may slow. While the rally is enriching some cotton investors, it’s also boosting costs for Levi Strauss & Co. and Hanesbrands Inc. <bloomberg.com/news>

Hedgeye Retail’s Take: Surging higher following Thursday’s USDA crop report and continued flood damage in Pakastan, the rising cost of cotton is exceeding all estimates despite expected cost inflation in the 2H. Recall, Gildan with ~30% of COGS exposed to cotton noted last week that ~$0.80/lb. cotton would impact earnings by $0.50 next year on a ~$1.60 base…less than a week later, that view appears increasingly optimistic. HBI notes that its exposure is closer to 6-8%, but keep in mind that this understates the true impact as HBI buys much of its cotton FOB (i.e. it’s an indirect cost instead of a direct cost).

Shopping Habits Forever Changed? - Marketing firm BrainReserve doesn’t see women going back to their ferocious shopping habits once the economy fully recovers. The entire consumer mentality has changed across the socioeconomic spectrum. So is this the dawn of a New Consumer Age, as many experts contend, one that will force brands and retailers to make tectonic changes in the way they do business and transform the nature of shopping in America. It’s clear the shopping rules have changed and key trends include:

• The boom in e-commerce, making it easier for consumers to buy from home — and to comparison shop.

• Technology is now more fashionable than fashion — in other words, teens and twentysomethings would rather buy an iPad than a handbag.

• Social networks are driving real consumption, with friends telling friends about hot products or brands — meaning brands have to enter the conversation.

• The Great Recession has forced everyone, even the rich, to alter their shopping behavior and buy less.

• High levels of personal and household debt continue to constrict the Baby Boomers, who are looking for simplicity and value. <wwd.com/retail-news>

Hedgeye Retail’s Take: Call it “ferocious shopping,” or whatever you want, but excessive spending is officially taboo and frugal is in – a trend we don’t expect to change anytime soon.

Half of Local-Made Leather Shoes Disqualified in Recent Sampling Test - Shanghai Consumer Protection Committee has recently conducted a sampling test on locally manufactured leather shoes which revealed that about 45% of samples were not up to the standard. For the testing, twenty-nine pairs of shoe were sampled from Shanghai markets including five pairs of men’s shoes and twenty-four pairs of lady’s shoes that were made in Shanghai, Zhejiang, Jiangsu and Guangdong province. The test results found that thirteen pairs of leather shoes were defected in the nine technical parameters including appearance quality, peeling strength and heel fastness. <fashionnetasia.com>

Hedgeye Retail’s Take: Wage inflation isn’t the only reason for the shift of global manufacturing out of China towards countries like Vietnam and Indonesia. While we’re not certain quality standards are any better in these countries, an alternative is usually preferable to results such as these.

Nike Inks License Deal With Athlete Performance Solutions - Athlete Performance Solutions has teamed up with Nike for a line of pinnacle, performance footwear for sailing, rowing, fencing, weightlifting, boxing and shooting. The footwear is hitting retailers now. Discussions are in the works for retail partners in sailing and shooting, as well as premium retailers. <licensemag.com>

Hedgeye Retail’s Take: Why not? Footwears pre-eminent brand is targeting smaller markets albeit with considerably less competition.

H&M July Comps Improve by 10% - Hennes & Mauritz AB said same-store sales in July increased 10%, compared to 9% in June. Including new stores, total revenues for the month of July grew 21%, versus 20% in the previous month, showing a strong improvement on the same period last year. H&M had experienced a weaker-than-expected performance this April and May due to cold weather across key markets. <wwd.com/business-news>

Hedgeye Retail’s Take: Fast-fashion continues to be a relative outperformer within global retail.

eBay Invests in General Manager of eBay Fashion - In an effort to grow its apparel business, eBay has made recent investments in technology. Now it’s investing in people. Miriam Lahage has been named general manager of eBay Fashion, a new position. A 20-year veteran of The TJX Cos. Inc., Lahage founded Koodos.com, an online discount luxury boutique based in the U.K. At eBay, Lahage will be responsible for growing and driving innovation across the site’s fashion category, which did $5.4 bn in worldwide gross merchandise volume last year. Part of her job will be to attract more brands to eBay to give a fashion and editorial point of view. Lahage wants to bring more consistency to the apparel presentation on eBay’s selling platforms. <wwd.com/business-news>

Hedgeye Retail’s Take: Creating a more consistent apparel presentation for a retailer that will always be known for its consumer generated auction supply sounds like an impossible task. If eBay can ramp its new offerings rather than used merchandise there in an opportunity to gain share, however that segment of the market is getting increasingly more competitive behind the likes of RueLaLa and Gilt Groupe – eBay is wading into deeper waters with this one.