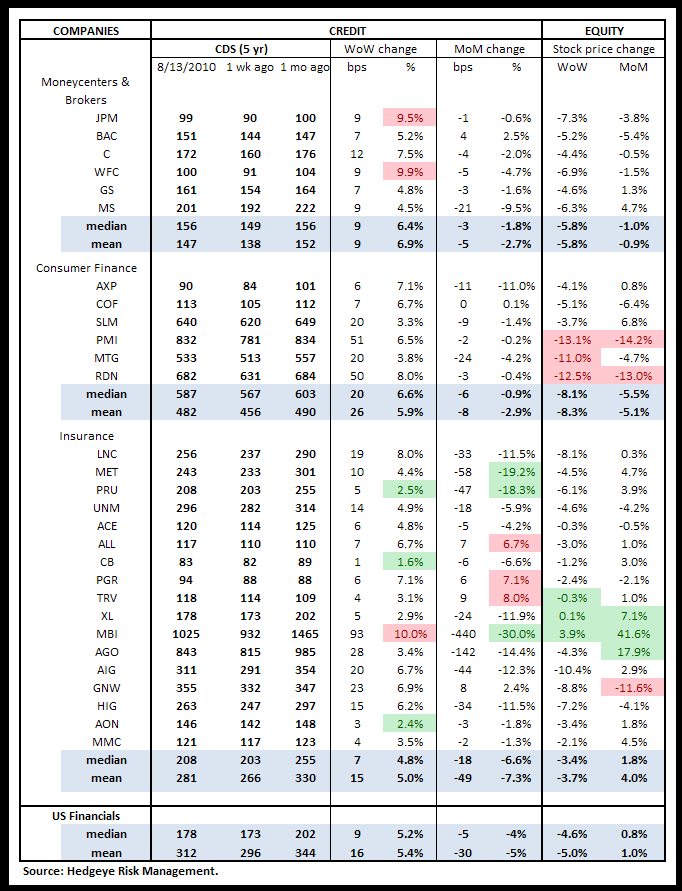

Last week, 7 of the 8 risk measures registered negative readings on a week-over-week basis and one was positive.

Our risk monitor looks at the following metrics weekly:

1. CDS for all available US Financials (29 companies)

2. CDS for large European Financials (39 companies)

3. High Yield

4. Leveraged Loans

5. TED Spread

6. Journal of Commerce Commodity Price Index

7. Greek Bond Spreads

8. Markit MCDX

1. Financials CDS Monitor – Swaps widened last week for all 29 reference entities. Conclusion: Negative.

Widened the most vs last week: JPM, WFC, MBI

Widened the least vs last week: AON, PRU, CB

Widened the most vs last month: ALL, PGR, TRV

Tightened the most vs last month: MET, PRU, MBI

2. European CDS Monitor – In Europe, swaps for 37 of the 39 reference entities widened and 2 tightened, with an average widening of 9.0% week over week. Conclusion: Negative.

Widened the most vs last week: Societe Generale, Alpha Bank, National Bank of Greece

Tightened the most/widened the least vs last week: Danske Bank, DnB NOR, Nordea Bank

Widened the most vs last month: Hannover Rueckversicherungs, Banco Popular, Intesa Sanpaolo

Tightened the most vs last month: Nordea Bank, UBS, DnB NOR

3. High Yield (YTM) Monitor – High Yield rates rose 17 bps last week. Rates closed the week at 8.47% up from 8.30% the week prior. Conclusion: Negative.

4. Leveraged Loan Index Monitor – The leveraged loan index fell 2 points last week, closing at 1491 versus 1493 the week prior. Strong momentum in July appears to have eroded. Conclusion: Negative.

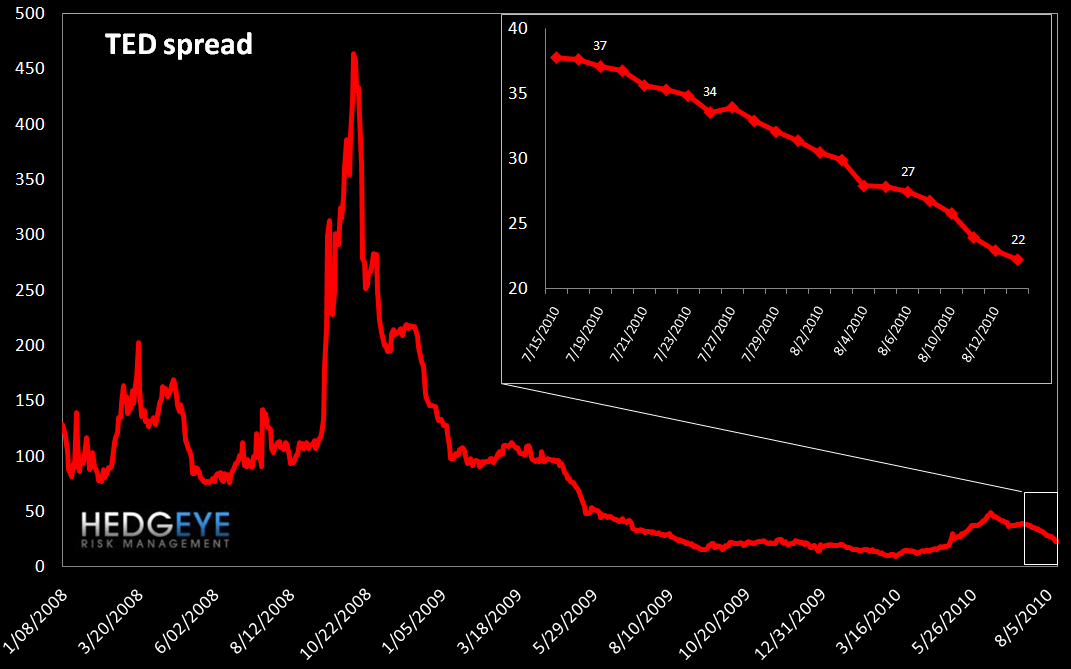

5. TED Spread Monitor – Last week the TED spread fell 5 bps, closing at 22 bps versus 27 bps the prior week. Conclusion: Positive.

6. Journal of Commerce Commodity Price Index – Last week, the index fell 4.5 points, closing at 13.65 versus the prior week’s close at 18.11. Conclusion: Negative.

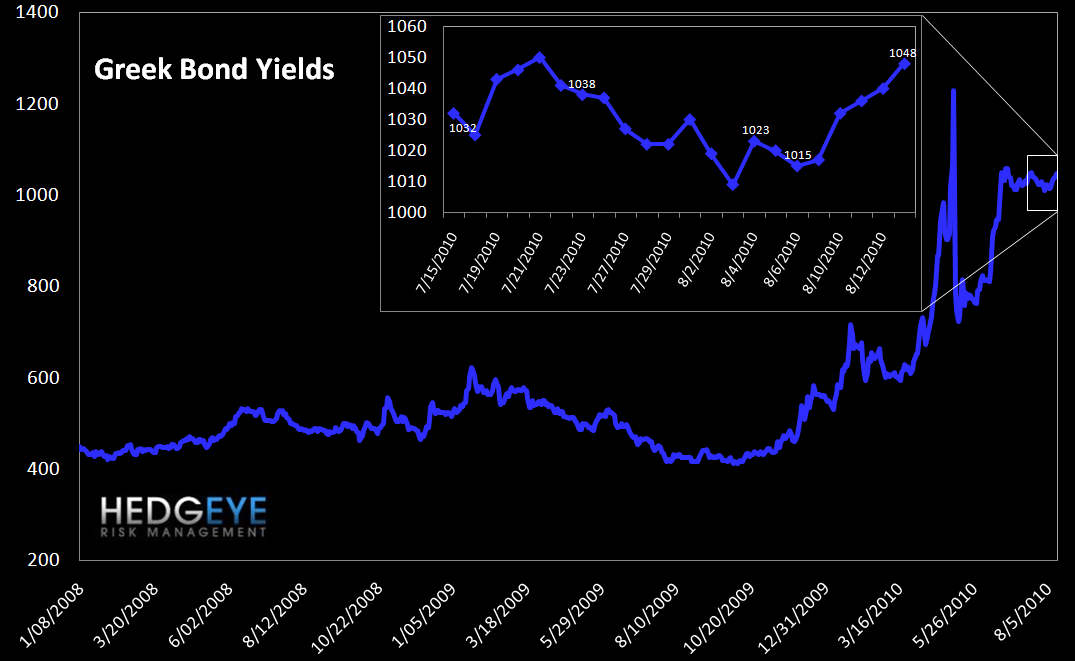

7. Greek Bond Yields Monitor – We chart the 10-year yield on Greek bonds. Last week yields rose 33 bps, ending the week at 1048 bps versus 1015 bps the prior week. Conclusion: Negative.

8. Markit MCDX Index Monitor – The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on four 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. Our index is the average of their four indices. Spreads rose last week, closing at 213 versus 206 the prior week. Conclusion: Negative.

Joshua Steiner, CFA

Allison Kaptur