Below are updates on our nineteen current high-conviction long and short ideas. We have removed Las Vegas Sands (LVS) from the long side. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

CHWY

Click here to read our analyst's original report for Chewy

Yes, there’s actually an ETF for the pet care industry – ProShares Pet Care ETF (PAWZ). It’s outperformed the S&P500 by 24% for the year-to-date. The reason…and I’m not making this up… “With all the sheltering in place and working from home folks have been subjected to this year, many are realizing pets are excellent avenues for reducing stress and loneliness.”

As is the case with cloud computing, online retail and working from home, the pandemic is setting in motion long-term trends that have favorable implications for the fast-growing pet care industry.

As ProShares notes, pet adoptions jumped 60% year-over-year during the pandemic. Additionally, there are favorable demographic trends pertaining to "PAWZ," including 26% of millennials spending more on their dogs than on themselves during these trying times. You want our opinion? The premise of the ETF is correct, but the best way to play the pet adoption trends is to go direct to the source instead of going the ETF route. That’s Chewy (CHWY).

The ETF does not have the dominance that CHWY does in its core market, nor does it have the optionality in adding a simply massive leg of growth onto the core by growing into international markets. We still get to $80 over a TAIL duration using non-aggressive modeling assumptions.

NOMD

Click here to read our analyst's original report for Nomad Foods.

For the week ended September 26, the CPG Index in the UK accelerated to +10% YOY from +7% in the prior week. Frozen food accelerated to +21% YOY from +16% in the prior week, as seen in the following chart. The frozen category led all edible categories. The recent increases in UK COVID-19 cases, plans for tighter social restrictions, and the expiration of the eating out promotion have led to a reacceleration in sales in September.

Recent strength in product categories like canned meats (+33%), canned vegetables (+28%), dry pasta (+25%), and of course, toilet paper (+66) also suggests consumers are likely stockpiling some grocery items. The UK is Nomad Food's (NOMD) largest country by sales, representing 31% of overall sales.

ZM

We can theoretically argue peak as much as we want but as long as Zoom's (ZM) is making higher highs in billings we aren't there. Zoom is the best tool in the category on key factors (adoption, ease of use, & stability) as well as single pane management for companies ZM follow on product creates a compelling roadmap for customers to easily unburden themselves of older telephony systems and should have significant COVID tailwinds.

Highly efficient cost structure with 42% NG OPM puts Zoom in a class of its own which is real margin rather than PE-rollup add-back margin (ahem, ZoomInfo) Zoom is still under-penetrated at the enterprise level and the growth of clunkier peers in 2020, like Webex, grows the market and leaves a long tail of wins ahead for Zoom.

NLS

This week, after an embarrassing pseudo partnership with Amazon that AMZN came out and quickly refuted – Echelon started to sell its bike in Costco. To be frank, we give Eschelon all the credit in the world.

The category is hot – even to the extent that Apple is launching a Fitness + app that can be used with lower price bikes like Echelon. It’s striking while the iron is hot. And for now, this category is white hot. Nautilus (NLS) was up another 20%+ this week, while competitor Peloton pushed an astonishing $120 – or $40bn in market cap. Its funny…at $6 no one wanted to talk about NLS. Now that it’s over $20 and can’t keep up with demand, we’re finally seeing institutional interest in the name. Nothing attracts a crowd like a crowd…

ZEN

Zendesk (ZEN) is a specialist in the customer support software category. In recent years, the company’s adoption curve has materially underperformed reported revenue growth as the original go-to-market motion became saturated.

The multiple for ZEN also deflated during this time. Our recent data on field notes, customer adoption, surveys, and other points, shows a refresh in customer adoption of ZEN potentially extending what was a stuck motion to a renewed adoption motion which could reset customer growth for at least several quarters if not longer.

FVAC

Increasing US tensions with China, flows into ESG funds, growth in alternative transport powertrains, lower carbon energy investment, combine with macro forces like accelerating inflation should drive investor interest in Fortress Value (FVAC). Rarely does a single equity check so many ‘thematic’ boxes, particularly when many of those categories are seeing rich equity market valuations.

The Mountain Pass mine has the richest developed rare earth deposit in the U.S. at a time when the geopolitical value of those assets has rarely been greater. Molycorp was ‘early’ to market, leaving an extremely valuable processing asset base and unfocused operationally, which we expect Mountain Pass to optimize (finally). As highlighted in our prior work, EV/Motors, Electronics, and Sensor market growth are very real for rare earths.

FVAC remains long.

STKL

Sales of non-dairy milks have risen over 60% in the last few years. The largest dairy company, Dean Foods, declared bankruptcy in 2019 as its borrowings and the revenue declines put too much pressure on the company.

Lactose intolerance, health reasons, and stories of animal use (do you remember Joaquin Phoenix’s Oscar speech) have all contributed to the decline in dairy sales. The impact to the dairy industry has been significant enough that dairy farmers have lobbied and sued to prevent plant-based milk producers from using the term “milk” to describe their product. SunOpta (STKL) is a leading supplier to the majority of plant-based milk producers. Plant based foods and beverages represent roughly a third of SunOpta’s total revenues and significantly more of its profits.

IIPR

This week Vermont legalized recreational marijuana sales, becoming the 11th state to legalize recreational use. Sales are not expected to begin until October 2022. This weekend Maine is finally slated to start recreational marijuana sales four years after voters approved the ballot initiative. There are five other states that will vote on similar initiatives next month.

It takes several years for legislation to reach the cash register. The long time frame gives Innovative Industrial Properties (IIPR) a longer timeframe to earn the outsized returns it is currently enjoying. IIPR also hit another 52 week high this week. IIPR stands in a unique position at the intersection of the cannabis industry and the REIT space in a rapidly changing legislative landscape, earning outsized returns in the current environment with few competitors.

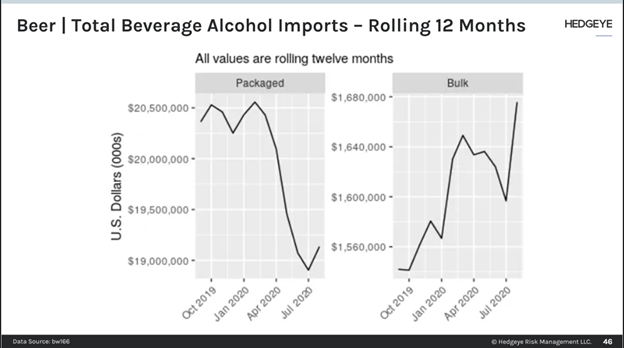

STZ

Total alcohol beverage imports declined 4% over the twelve-month period ended in August. Over the last three months, imports declined by 5%. 30% of all imported alcoholic beverages by value came from Mexico.

Imported beer declined 5% by volume and declined 2% by value over the last 12 months. Over the last three months, imports were flat by volume and up 3% by value. This compares to a 20% volume decline and an 18% value decline in the three-month period ended July, as seen in the following chart. 71% of beer imports by value come from Mexico, which shut down beer production from early April to June.

Constellation’s beer imports are now running full steam ahead which is leading to better depletion trends in packaged goods and grocery stores. Constellation Brands’ (STZ) sell-through rates are on track to have the best month of the year in September, that’s accelerating revenue growth headed into Quad 4 in Q4.

MIK

As evidence of the heat around the home/arts and crafts category, this week Dollar General launched a new concept called popshelf, which features non-consumable product from $1-$5 geared toward the home, and to a lesser extent, the crafting category. Imitation is the best form of flattery, you can say on one hand.

Increased competition is what I’d say on the other. To be clear, it will take 5+ years of store growth for popshelf to pressure Michaels in any meaningful way, and that’s giving Michaels (MIK) no credit for its own initiatives to grow share in the category. But it makes sense for DG to launch this initiative around the home at a time when demand is strong, and will only get stronger through the holidays. The consensus is looking for the same store sales growth rate at MIK to be cut in half by the January quarter, which we think is too conservative by several hundred basis points. One piece of pushback we get on this long is the leverage that MIK has on its balance sheet.

Agreed there. Retailers and financial leverage don’t mix. But leverage works both ways. When the business is in a decline, it could be a nail in the coffin. When the business pops, you get meaningful upside surprises, which we think will be the case for MIK.

EXPE & MAR

Click here to read our analyst's original report for Marriott.

The still widening divergence between both business travel and leisure travel is a key theme within hotels, in our opinion. Spreads have been widening in actual reported data and forward looking survey data continues to suggest that the current trends are likely to persist. Updated survey results per MMGY’s monthly “Travel Intentions Pulse Survey” (TIPS) suggests that intent for travel among business travelers took another step back in the late September survey, and still remains well below its recovery highs from June of this year. On the leisure side, optimism about future travel made a new post Covid high again in September, and so did the “net” intent.

Until we see clear tangible evidence that can get us more positive on sustainable step towards recovery for business travel, we’ll remain negative on the industry’s highest margin customer. Better leisure travel sentiment will help the hotel industry’s recovery, but the added leisure demand will not be enough to bail out the biz travel weakness.

We remain open minded, but thus far, the data has made us very skeptical regarding a near term corporate travel demand recovery, and the best way to express this continues to be our core C-Corp short Marriott (MAR). On the flip side, our Best Idea Long Expedia (EXPE) is a great way to play the upside in leisure travel demand.

GOLF

Click here to read our retail analyst's original report.

Acushnet Holdings (GOLF) was up yet again on the week pushing the stock above the consensus price target of $33, which suggests that we need to either see a series of upwards revisions – which we think is extremely unlikely given the disconnect we’re seeing in rounds played (positive) versus the impact on the actual golf economy (negative), or downgrades in the stock.

The stock’s sentiment is perplexing, as the sell side only has 11% of ratings as ‘Buy’, but the buy side only is sitting on 7% of the float short (below the critical 12% level we often refer to in our analysis/process) – and interesting dichotomy. This is one of the rare occurrences where we think ‘old wall’ is right to not be bullish.

It’s not just because valuation is top decile on both earnings and cash flow, but that the earnings revision factor should turn negative as people focus on 2021 earnings, which is right around the corner.

AXP

American Express (AXP) carries risk on two main fronts: transaction and credit. T&E spending makes up more of American Express’ transaction volume than any other card company, which, although recovering slowly, is still comping down 65-70% Y/Y. It’s also important to note that this is higher margin business than the non-T&E categories, making it disproportionately impactful.

Will Covid-19 result in structural changes to business travel and entertainment? Given its exposure to T&E spending due to the travel-heavy appeal of its card products, we think the company's top-line will likely be impaired long-beyond a basic resumption of activity, as evidenced by the very slow recovery in T&E billings. Marred by a deteriorating merchant value proposition and staring down the double barrel of depressed payments volume and rising credit risk, we continue to see asymmetric downside in the shares of American Express and are thus keeping AXP.

ZI

An excerpt from some of our field-work on ZoomInfo (ZI):

ZI rolled out Engage, their new sales engagement tool. This is what salespeople commonly and incorrectly refer to as “auto-dialer”. This tool allows a salesperson to initiate an email or a phone call to a prospect without leaving the ZI platform. Analytical information such as salesperson productivity, success of their campaign and email open rates are then available for review by both the rep and management.

The rollout seemed to be rushed and badly thought through. I attended a webinar touting the benefits of the products for existing customers and the presenters were junior, late, and ill prepared. Now, a month or so after the rollout presentation the usual ZI advertisement for the product on users’ portals and videos or marketing pieces seem absent. According to sales management ZI hasn’t been pushing it hard a t all and few salespeople at my company know or care about it.

SMAR

The bull case on Smartsheet (SMAR) is that users like the tool – and it provides unique value relative to the other solutions in the market. As some have expressed: a Smartsheet is more powerful than tools from Asana, Monday, or Trello, but less powerful than Microsoft Project.

The problem? The market for paid users in this category is still small and will remain that way until some innovative new product comes along and unlocks a bigger seat TAM. Such a product will likely use ML to read our existing workloads and autopopulate and manage intra-company project management by tiers of decision makers; it will probably also be really cheap.

MDLA

While profits improved into 2020, Medallia (MDLA) will confess (after they raise the convert, not before) that 2021 will be ‘an investment year’ and profitability will not improve. How do we know? Because incremental revenue driven inorganically doesn’t waterfall profit the way organic revenue does, and because the two companies most recently acquired are in cash-burn mode.

The acquisition of Stella Connect keeps 4Q above 20% revenue growth. Stella is a perfect MDLA acquisition: raised $50MM+ over 12 years, acquired for $100MM, and MDLA CFO pretends MDLA can "make Stella great again". MDLA needs one more to get them there for 1Q22. But the next one will be smaller ($10MM annual revenue; should cost $50-60MM) and CEO Leslie Stretch will be sure to remind all of us that he only does technology tuck-ins.

RL

Apparel Imports Bearish for Holiday Sales. Slight sequential improvement in the rate of apparel import declines for the month of August – the latest month reported by OTEXA. Apparel imports were down 22% to $6.6bn vs -32% in July. Props to the apparel retail space in aggregate for adjusting inventory purchases to the anemic level of demand.

But what that means is that to the extent that demand actually shows up around holiday, the inventory won’t be there – in other words they’ll be money left on the table. We’d like to say that’s bullish for gross margins, but on the flip side we’re seeing the holiday shopping season start so early – next week with the launch of Amazon’s Prime Day – that we think the margin equation will be impaired for the quarter even if demand materializes at a rate better than expected. Ralph Lauren (RL) is relying on SG&A cuts to save its margin over a TREND and TAIL duration, which is a big mistake.

RL needs to invest in SG&A to regain consumer connectivity with the brand – not flow the benefit of headcount cuts through to the bottom line to drive earnings – which will prove to be temporary in nature.

WORK

While Slack (WORK) has hinted at some amazing potential roadmap products, the progress from imagination and hyperbole to actuality has not been the Ferrari pace that might inspire us. We have listened to management describe a Slack-first universe and we have read blog posts from technologists who can describe a Slack-first world, but as of August 2020, it still seems a little bit like science fiction.

We struggle to get excited about current products and while we are theoretically excited for rumored products, we are still waiting for the science part of the science-fiction story to come through.