Position: Bullish Bias on Germany (EWG); Long the British Pound (FXB)

The negative reaction from European capital markets to positive Q2 GDP numbers out of Europe today is another confirming signal of our call for “trouble ahead” in the region in the back half of the year.

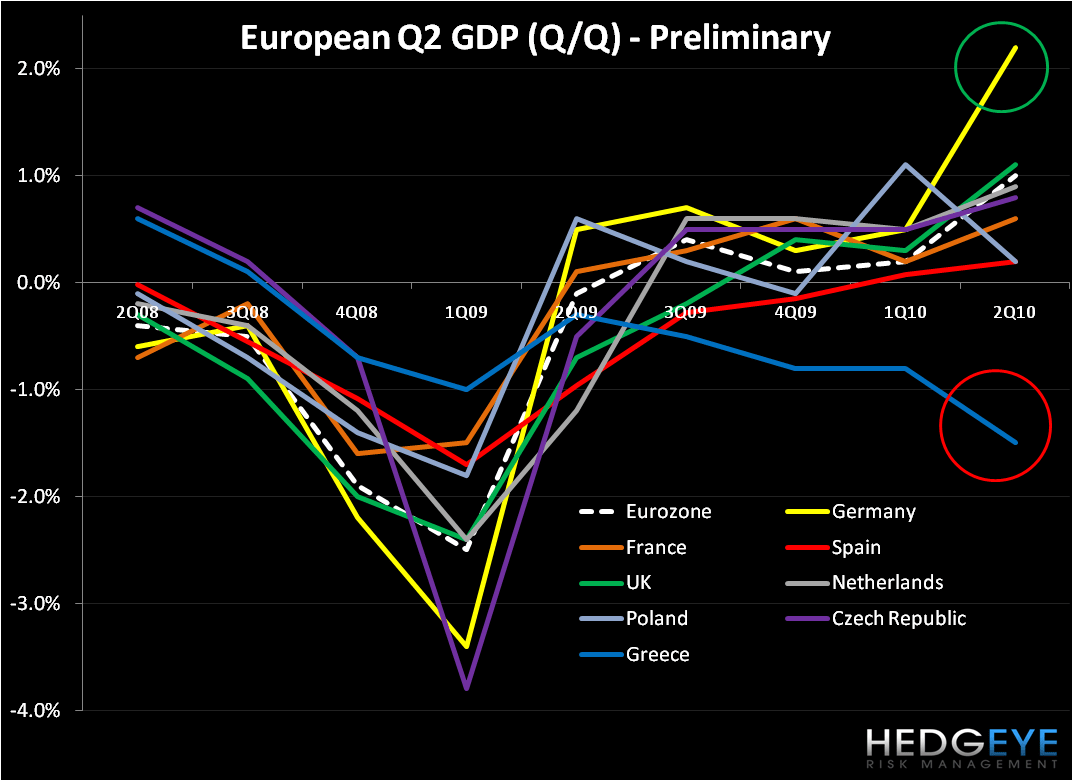

We’ve maintained a bullish bias on Germany over the last weeks. Certainly the outperformance of Germany’s Q2 GDP print (2.2% Q/Q, the largest quarterly gain in over 20 years) over its European peers has also translated to its equity market outperformance: the spread of the DAX over Greece’s ASE is 2700bps! (see charts below)

However, our outlook on Germany and the region still remains cautious in 2H10. Importantly, we’re still looking for the DAX to confirm its TREND line of support at 6076 before we’re a buyer. We believe that August and September European data will be especially critical for it will show an inflection point to the downside.

Certainly Germany’s strong Q2 growth is in line with the fundamentals we’ve followed over the last months: a weak Euro (esp. in May/June) boosted exports, German exports found strong demand from China, the country’s employment and inflation picture remains stable, and comps have been “healthy”, especially when compared with bombed out levels in 2009.

Yet the inflection we’re expecting to see has yet to show up in the data, both due to the skew in the numbers because of the World Cup in the early summer and the impact that austerity measures issued throughout European countries will have in 2H10 and 2011, namely in choking off growth.

Taking a look at the charts below, “risk-on” in Europe has shown up over the last week. Sovereign CDS for many European countries rose ~15-30% over the last week and Greece continues to flash weakness, with its 10YR bond yield spread over German Bunds busting out (see charts below). As a reminder we believe that sovereign debt risks in Europe are not rear-view. Debt come due this year and next is one outstanding issue that the ‘PIIGS’ will continue to wrestle with.

We remain long the Pound (FXB) with a trading range for the GBP-USD of $1.54-$1.61.

Matthew Hedrick

Analyst