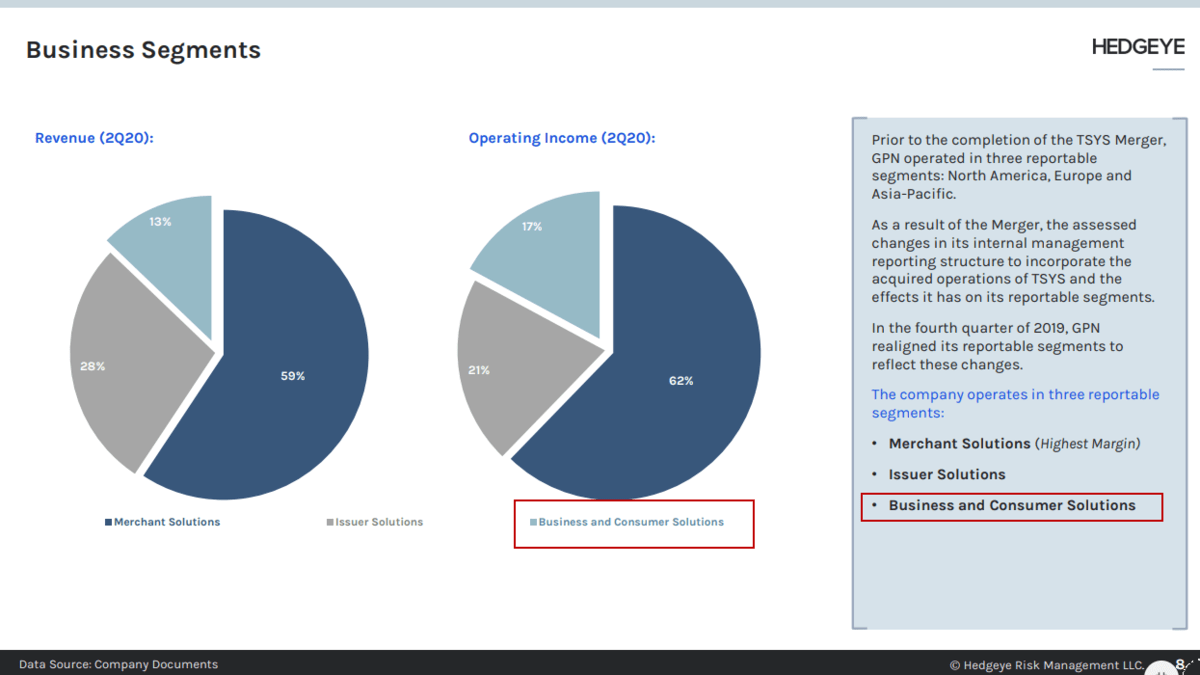

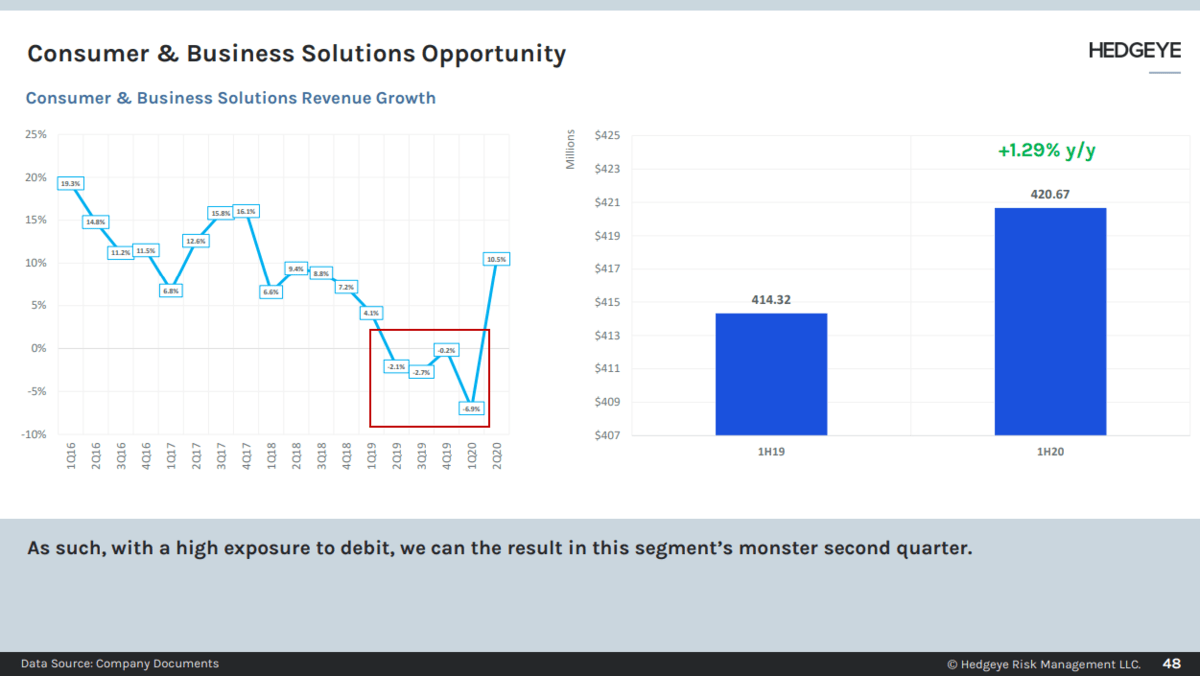

Recall, upon consummating its merger with TSYS one year ago, Global Payments acquired the former's Business and Consumer Solutions segment which provides general purpose reloadable prepaid debit and payroll cards, demand deposits, and other financial service solutions to the underbanked in the United States through the Netspend brand.

Netspend generates revenue through fees collected from cardholders and fees generated by cardholder activity.

In April 2019, shortly after the announcement of the merger of equals between Global Payments and TSYS, the CFPB's new Prepaid Rule took effect, requiring consumers to be presented with upfront information about prepaid account fees.

With a more informed consumer, and against a competitive backdrop of free and superior alternatives like Cash App, Chime, and Venmo, Netspend revenues declined over the subsequent twelve months.

We welcome the rumors, as reported by the Financial Post/Reuters earlier this afternoon, that Global Payments is exploring the sale of its prepaid debit card business, especially as the latter enjoys a temporary boost from fiscal stimulus while facing a challenging competitive and regulatory landscape. The war for the underbanked is being heavily waged by the likes of Square (Cash App), PayPal (Venmo), Chime, and others, and Global Payments is not well positioned to compete over the longer-term. Accordingly, the sale of Netspend would free up cash and rightly focus the company's time and resources on its core merchant and issuer processing businesses.

The business is expected to be valued at over $2B or >2.46x LTM revenues of $811 million, or using a LTM non-gaap operating margin of 25%, >10x non-gaap operating income.