2021 could have more hard seltzer launches than 2020 (SAM)

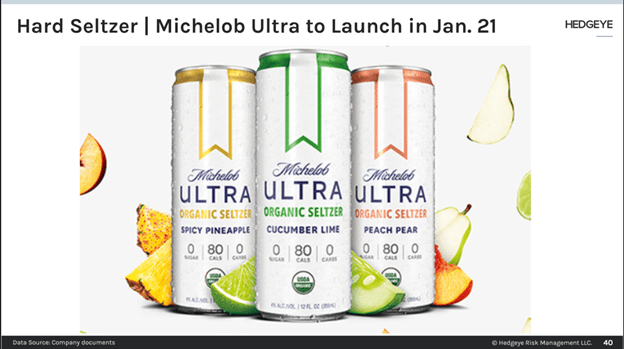

Anheuser-Busch InBev announced yesterday that it would launch Michelob Ultra Organic Seltzer in January. It is the first nationally available hard seltzer brand that has been certified organic by the USDA. The product will have 80 calories, 4% ABV, and zero grams of carbs or sugar, putting it below White Claw and Truly’s 100 calories, 5% ABV, and 2 grams of sugar. Michelob Ultra is the second best-selling beer in the US off-premise retailers after Bud Light. Anheuser Busch InBev now has a suite of hard seltzer brands positioned differently. Bon & Viv is the premium brand, Bud Light Seltzer leverages Bud Light, Bud Light Platinum is positioned for evenings out with 8% ABV, Natural Light Seltzer is an opening price point, Social Club has cocktail flavors, and Michelob Ultra Organic Seltzer is geared for an active lifestyle.

The CEO of PepsiCo had the following to say about a hard seltzer product yesterday, “We look at every opportunity, there is in the industry and a couple of years ago was CBD. Now it's more alcohol. So, we got a lot of opportunities in front of us. Of course, we're looking at all of them, and we have people that are thinking more long term versus the very immediate 2021. So, we're reflecting, we're thinking what the best options are, and we will make decisions in the coming quarters whether this is an area where PepsiCo wants to play. More importantly, how do we capture a lot of value for this opportunity? Given the three-tier system, it's not obvious how you capture a lot of value. So, there is first, do we play or not? Second, very important, is who do we play with and who do we partner to maximize the value for PepsiCo?”

It sounds like PepsiCo will continue to evaluate the space, but there is a good chance the company could enter the hard seltzer category after 2021 using its Rockstar or Bang brand. PepsiCo seems more concerned about the economics (see our comments about Coca-Cola’s Topo Chico from yesterday) than brand confusion. We expect 2021 to be another year of robust growth for the hard seltzer category as well as the number of new competitive entrants. PepsiCo is on our Long Bias List.

STZ’s Q2 puts the pandemic in the rearview, fires in wine country ahead

Constellation Brands reported FQ2 EPS of $2.76 vs. consensus of $2.51; the results include $.15 of equity losses from Canopy Growth. The upside was driven by better margins, with marketing spend delayed until the 2H. Beer sales were up 1%, excluding the sale of Ballast Point with organic shipment volumes down 1%. Beer depletion growth of 4.7% and shipments down 1.6% were in line with our expectations and at the high end of guidance. Beer sales grew 11% in IRI channels with Modelo up 12% and Corona up DD%. Wine & Spirits' net sales decreased 11% with shipment volumes down 19%. Excluding the divestiture, organic net sales declined 9%, with shipment volumes down 17%. Overall, wine depletion volumes decreased by 3%, with its power brands down 1%.

Gross margins were flat with favorable pricing offset by unfavorable mix and reduced throughput at the breweries. Marketing was 70bps lower with fewer events. Beer EBIT margins expanded 70bps while wine margins expanded 310bps. Management expects the impact from the West Coast fires to be $25-35M in FQ3 and $10-15M in FQ4. Corporate expense grew 13% in the first half, which seems incongruent with business trends. The closing of the Gallo transaction was pushed out another quarter.

Management said the timing of 1-2% price increases would be more staggered in 2021, which seems appropriate given the economic environment. Management also said their goal is to be a top 3 brand in hard seltzer. Corona Hard Seltzer is currently in fourth place, but share points have grown from 4% to 6%. Bud Light Seltzer currently has a 10% share in the third spot. Shipments will outpace depletions in FQ3, but depletions are accelerating with better inventory availability.

Constellation Brands’ most negatively impacted quarter from the pandemic is now behind us. Going forward, we see sales growth accelerating from better in-stock levels (September depletions could be the best month of 2020), more on-premise re-openings, and more sporting events/marketing to be positive catalysts for the shares. Increasing confidence in its ability to continue to gain share despite the growth in the hard seltzer category and smaller losses in Canopy should lead to a higher multiple. Constellation Brands is the Best Idea Long.

CAG makes a case for at-home meal consumption for longer

Conagra reported FQ1 EPS of $.70 vs. consensus of $.57 driven by slightly better sales growth and margin upside. Organic sales growth was 15%, above guidance of 10-13%. Retail sales grew 14.6% in snacks, 13.5% is frozen, and 11.6% in staples for total retail sales growth of 12.9%. Shipments were 600bps above consumption as retailers looked to rebuild inventory levels.

The frozen business was led by frozen single-serve meals up 17.7%, while plant-based meat alternatives grew 35.7% and frozen vegetables only grew 0.7% (shipments grew much faster as retailers rebuilt inventories). The snacks business was driven by a 20.1% increase for meat snacks while popcorn grew 19.5%, sweet treats grew 15.4%, and seeds declined 11.9%. Staples was driven by Armour up 18.8% and Wishbone up 16.9% while Chef Boyardee grew 5.6%, and Vlasic grew 3.6%. Foodservice declined by 20.3%.

Management expects at-home eating is likely to remain elevated due to recessionary pressures, increased work from home, and elevated at-home eating even as states re-open. Management points to the 2009 recession, which saw a 200bps shift towards at-home consumption, repeated in Q2 of this year. Sales have re-accelerated in the two most recent weeks, as seen in the following chart.

Adj. Operating margins expanded 450bps to 20.2%, beating guidance of 17-17.5%. Realized productivity, price/mix, leverage, and synergies benefited margins by 610bps. COGS inflation of 3.1% was a 220bps headwind to gross margins, divestitures were an 80bps headwind, and COVID costs were another 150bps headwind. SG&A leveraged by 190bps.

FQ2 management is guiding to EPS of $.70-.74 compared to consensus expectations of $.72. Organic sales growth is expected to be 6-8%. Adj. Operating margins are expected to be 18-18.5%. With the cash flow, the company is generating the net leverage ratio has fallen to 3.7x from 4.0x a quarter ago, and the target of 3.5x reachable before year-end. Deleveraging and synergies will help to change opinions on the Pinnacle acquisition. In the near term, investors may be concerned about the 600bps differential between shipments and consumption and what that implies for sales deceleration going forward. Still, for the grocers, the elevated consumption could lead to share price outperformance. Conagra is on our long bias list.