R3: REQUIRED RETAIL READING

August 12, 2010

While there is no question basketball has been weak for some time now on an absolute basis, our weekly scan data suggests the trend has actually improved sequentially over the past three months.

TODAY’S CALL OUT

There’s been some noise in the marketplace suggesting the basketball footwear category has eroded over the past few months, especially in the athletic specialty channel. While there is no question basketball has been weak for some time now on an absolute basis, our weekly scan data suggests the trend has actually improved sequentially over the past three months. Weak or not, we believe the opportunity for the category (against easy compares) is becoming even more exciting. This comes on the heels of an inevitable investment in product by Nike to support Miami’s “big three” and as Under Armour prepares to launch its hoops product in October. And, while Reebok hasn’t been on the basketball scene since AI entered the league, there is some promise with the signing of John Wall and a line built off of the Zigtech platform.

Importantly while basketball is just one part of Foot Locker’s merchandise mix, this data does support our positive stance on the upcoming quarter. While we are conservatively forecasting a 4.5% comp increase (could be upside from Europe driven by successful World Cup sell-throughs), we believe margin trends will be solid given tight inventory levels entering the quarter as well as another quarter of benign promotional activity. Our model is looking for $0.13, well ahead of the $0.03 consensus. FL reports next week on August 19th.

LEVINE’S LOW DOWN

- Macy’s noted that back to school selling has been “very encouraging”. In particular, the company’s recently launched Material Girl line (in collaboration with Iconix, Madonna, and her daughter Lourdes) has been posting strong initial sell throughs. Management also believes the buzz surrounding this line is also helping to boost traffic beyond the brand itself.

- Keep an eye on the state of California which is soon to bring a bill to the senate which aims to ban the plastic bag. With a clear focus on the environment, the bill which already passed the Assembly would make CA the first state to ban retailers for using plastic. Looks like paper or BYO if passed.

- As JC Penney prepares for the launch of its Mango shop-in-shops, the Spanish retailer is looking accelerate its growth plans globally. The family owned business is planning to open a store per day over the near-term, with an eye on expansion in China. With 1,500 stores currently, this growth rate puts the fast fashion retailer in rare territory for concepts that are still looking add meaningful square footage.

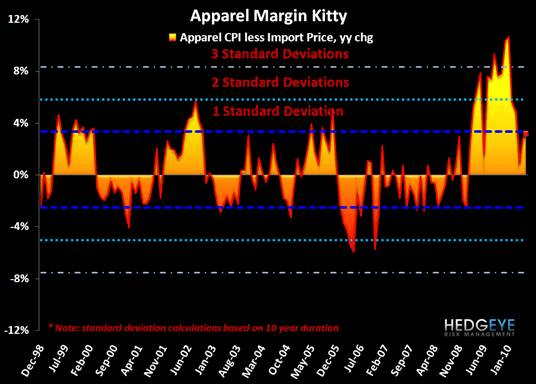

MORNING NEWS

June Apparel Imports Rose 36% - Led by major gains from Asian countries, textile and apparel imports to the U.S. surged in June, as retailers restocked inventories. Combined shipments of textiles and apparel to the U.S. rose 36.1% driven by apparel imports growth of 25.8% and textile shipments growth of 45.1%. Combined textile and apparel imports from China (#1 supplier) spiked 52.4%, India (#2 supplier) increased 32.6%. The top five apparel suppliers to the U.S. in June were: China, Vietnam, Bangladesh, Indonesia and Honduras. China was also the top textile supplier, followed by Pakistan, India, Mexico and South Korea. <wwd.com/business-news>

Li & Fung Acquires US Footwear Brand Jimlar - Hong Kong-based sourcing giant Li & Fung Limited confirmed Thursday that it has acquired U.S.-based footwear maker Jimlar Corporation, confirming a July report in these columns. LF USA is nearing a deal to acquire Jimlar Corp. for $450 million. Jimlar is a privately held firm that owns the Frye trademark and does business through licenses such as Coach and Calvin Klein. A price was not disclosed in Thursday's announcement and the company could not be reached for comment at press time. <wwd.com/business-news>

Hedgeye Retail’s Take: As expected, Li & Fung continues its shopping spree, but this time with an acquisition of some content. Recall earlier in the week the company acquired a transportation logistics business in an effort to take more of the logistics process in-house.

Gap Inc. Expanding Global E-commerce Reach - Gap Inc. said its e-commerce capabilities will extend to 65 countries by year end. The international Web push marks the e-commerce debut of Gap, Banana Republic, Old Navy, Piperlime and Athleta outside of the U.S. With the expansion, Gap’s online presence will touch more of the globe than the company’s brick-and-mortar stores. Gap is in five countries with company-owned units and 20 with franchised units, while Old Navy has no stores beyond North America. Gap has partnered with FiftyOne, a New York-based e-commerce specialist, to develop the online infrastructure needed to support a Web business around the world, with the exception of China. For China, Gap is working with Shanghai Yi Shang Network Information Co. Ltd. to provide e-commerce starting this fall. Gap’s e-commerce business was $295 mm in Q1 up 11%. <wwd.com/business-news>

Hedgeye Retail’s Take: A no brainer given the platform is in place and the cost to build out has dropped substantially as technology advanced. Makes a ton more sense than opening stores across the globe.

Celebrity/Proprietary Brands Squeeze Independent Labels - As retailers seek to add more celebrity and proprietary brands, there’s no end in sight to exclusive pairings. And it’s getting a lot tougher for other labels to compete. Brand exclusives and private label are increasing their share of big-store real estate, commandeering dedicated advertising and promotional support, not to mention buying dollars. If a store has two brands that are similar, and one is an exclusive, there's plenty of reason to leave one out. With department stores narrowing the number of vendors they carry, those brands without an exclusive will have a much harder time competing. <wwd.com/retail-news>

Hedgeye Retail’s Take: Exclusivity has been a trend for the past several years and this is nothing new. Note to vendors: Produce a line consumers want and they will pay full price for it.

Li-Ning USA and Champs Sports Team Up - Li Ning Company Limited and Champs Sports have announced their partnership in the U.S. launch of the Baron Davis sportswear collection. Beginning on Friday, August 13, the “BD Doom” line of footwear and apparel will be available in select Champs Sports stores, located primarily along the west coast. Named after and designed in part by NBA All-Star Baron Davis, the BD Collection includes both performance and lifestyle footwear and attire. The assortment will also be offered online at Champssports.com and Eastbay.com, both divisions of Foot Locker, Inc. Champs Sports is the first U.S. retailer to partner with one of China’s most popular sportswear companies. <sportsonesource.com>

Hedgeye Retail’s Take: Well within the realm of our expectations, this marks yet another exclusive partnership for Foot Locker under new leadership. While the partnership with a Li Ning is interesting on its own merits, the exclusivity with Champs/Eastbay is just a small part of FL’s strategy to differentiate and ultimately regain market share. We expect to see similar deals coming over the next 12-18 months.

Nine West Steps Into M-Commerce - Consumers can use the shoe retailer’s mobile site to access the complete catalog of products found on the Nine West e-commerce site. Shoppers also can buy products and access accounts that contain default payment, billing and shipping information. <internetretailer.com>

Hedgeye Retail’s Take: Newsflash. M-commerce is essentially e-commerce when you’re not at your desk. At some point soon, m-commerce launches will no longer be newsworthy, but rather just a part of normal retail activity.

Timberland to Expand Green Index to All Footwear by 2012 - The Timberland Company plans to expand its "Green Index" to all its footwear by 2012. <sportsonesource.com>

Hedgeye Retail’s Take: While once a gimmicky marketing ploy, it is clear consumers actually do care where there products come from and how they are constructed. TBL remains on the forefront of the “green” movement, an area in which the overall footwear industry has a long way to go.

UK Ethical Tradition Initiative Calls Upton Bangladesh to Increase Minimum Wage - The Ethical Trading Initiative has backed calls for the Bangladeshi government to make a further increase in the minimum wage. <drapersonline.com>

Hedgeye Retail’s Take: While the wage debate continues in Bangladesh, there is no denying prices are on the rise as labor heads higher.

Brazil Reaches 1 BN in Leather Exports Despite July Decline - Sales of the Brazilian product grew by 74% in the first seven months of this year as compared to the same period last year and is expected to reach US$1.7 billion in exports by the end of this year, according to the Confederation of Hides and Skins Industries. Brazilian leather exports totaled US$ 1 billion from January to July. Despite the growth in exports during the period, sales in July dropped by 13.3% as against the previous month. The reduction was a consequence of financial problems faced by international markets, especially the European Union. <fashionnetasia.com>

Hedgeye Retail’s Take: Keep an eye on Brazil as a leather source as China looks to cut capacity in an environmental effort to eliminate toxic factories.

Despite Fewer Internet Users than Men, Women Spend More Online - According to comScore’s “Women on the Web” white paper, women account for just less than half of US internet users but make up a disproportionately large share of online buyers, at nearly 58%. Their share of transactions is even higher, with more than 61.2% of online purchases made by women. They also spent more than men, accounting for 58.2% of the total, suggesting men tend to make fewer purchases of bigger-ticket items, while women are more frequent buyers with a lower average order value. In the US, women dominated most in the online market for fashion and jewelry, toys, housewares, books and other entertainment, and even video games. Around the world, comScore found that women spent 20% more time on retail sites than men. Reach of most categories of retail site was higher among women, with a few exceptions: Computer hardware and software, consumer electronics, sporting goods and music were more likely to be shopped for by men. <emarketer.com>

Hedgeye Retail’s Take: Not surprisingly the breakdown between male/female purchasing behavior looks very similar to metrics tracking traditional retailing. Yet another reason why online and offline shopping have reached a point where they are now seamless in the mind of the consumer.