This insight was published on July 14, 2010. RISK MANAGER SUBSCRIBERS have access to SELECT MACRO content in real-time.

___________________________________________

The Singapore Sling: Why We Are Long of Singapore

Position: Long Singapore via the etf (EWS); Bullish on SGD-USD.

Conclusion: As part of our call that growth will slow globally in 2H10, we want to be long currency and equity markets that are poised to accelerate domestic consumption. Singapore is one of those economies and, as a result, is one of Hedgeye’s top Macro investment ideas.

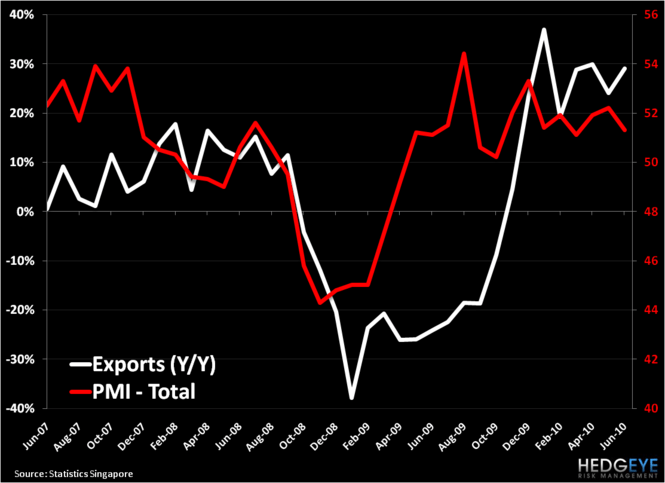

Based on recent strength in manufacturing and exports Singapore posted a 2Q10 GDP growth number of 19.3% Y/Y. The record gain was fueled by strong industrial production growth, which accelerated in May to +58% Y/Y. Manufacturing in Singapore has grown by an average of 45% in the first five months of 2010, led by strong output in the pharmaceutical and electronic sectors – two of Singapore’s largest export bases.

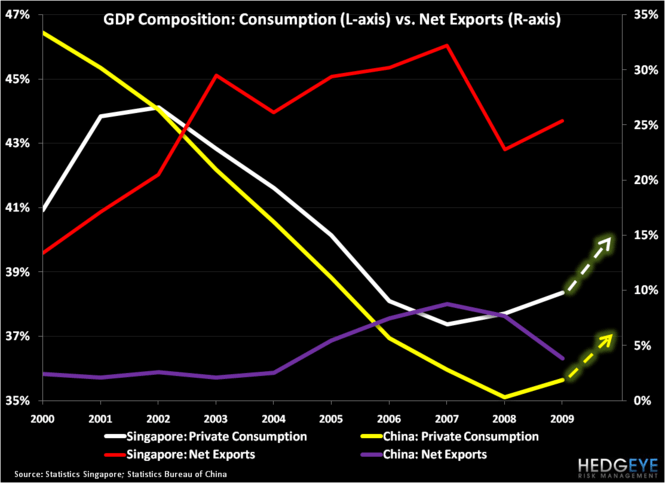

Despite the EU’s sovereign debt issues, the large growth in exports during the 2nd quarter, the net of which compromised 25% of GDP in 2009, is an incrementally bullish read-through in conjunction with the 2Q GDP release. Singapore’s non-oil, domestic exports accelerated on the margin in June to +29% Y/Y vs. +24% Y/Y in May. Upon further scrutiny, however, we find that European austerity and economic stagnation in the U.S. paints a more sober picture of the intermediate term trade outlook for the $182 billion economy. Today, the Trade Ministry of Singapore stated:

“In the European Union, domestic demand remains depressed as concerns over the sovereign-debt crisis persist… The implementation of fiscal austerity measures in some of the economies may further weaken their domestic demand. The weakening of the euro against key trading partners will also dampen import demand in the European Union. Signs of a slowdown in the labor market in the U.S. have affected consumer confidence, and sluggish final demand from the world’s largest economy as well as Europe has led to a moderation in manufacturing in Asia.”

The consensus belief that European Austerity may negatively negative impact Singapore’s exports has upside risk. Nominal exports to the EU are less than 8% of the total with the economically healthy Germany compromising 20% of that share. That said, just last week, the EU Delegation to Singapore plainly stated that trade between the two entities would remain vigorous in 2H10, despite austerity measures.

Breaking down the most recent trade numbers in more granularity, we find that growth of non-oil, domestic exports (NODX) to the EU accelerated in June (+75% Y/Y vs. +5.7% Y/Y in May) due to a favorable inventory cycle for pharmaceuticals, electrical machinery, and computer parts. This is likely to moderate going forward, as Singapore PMI slowed in June (though still showing expansion in all major categories: total, new export orders, new orders, and order backlog). The takeaway from this is that, while cause for concern, European austerity fears should not be overstated in an analysis of Singapore’s trade outlook.

Trade Outlook: Moderate

In fact, the majority of Singapore’s exports go to Asian economies, with the largest recipients being: Hong Hong (11.6%), Malaysia (11.5%), China (9.7%), Indonesia (9.7%), and Japan (4.6%) (CIA Factbook, 2009). The U.S. is a destination for roughly 11% of Singapore’s nominal exports, so continued weakness (Y/Y growth flat sequentially from May to June) from that market – which we expect – may continue to weigh on Singapore’s export growth throughout the remainder of this year. Conversely, bullish demand from China – supported by government stimulus and recent wage growth – may help offset any potential declines in exports caused by the U.S., which we’re already seeing evidence of. While growth of NODX to both China and Hong Kong slowed marginally in June, the Singapore Trade Ministry has credited one or both of these markets as the largest contributors to overall export growth in every month this year except February. Even then, Taiwan and Indonesia picked up the slack in February as two of the largest contributors to growth. Asian markets will likely be the key drivers to Singapore’s export growth going forward and the recently launched China-ASEAN Free Trade Area agreement holds the potential to greatly accelerate intra-regional trade.

All said, Singapore’s export growth is still likely to moderate from here and, like many world economies, will slow in 2H10. Despite this, we contend that the economy is in a bullish setup supported by internal demand, as supported by the Ministry of Trade’s third upwardly-revised 2010 GDP estimate today (+13-15% Y/Y vs. previous forecast of +7-9%).

Domestic Consumption Outlook: Bullish

At a mere 2.2% in 1Q10, Singapore’s latest unemployment rate is at its lowest level in 18 months, thanks to private and public efforts to bolster the services sector the Southeast Asian economy. The opening of two casino resorts by Genting Singapore Plc and Las Vegas Sands contributed to a net addition of 36,500 jobs in the quarter and record tourism for the sixth consecutive month (+30% Y/Y in May and driven by intra-Asian visitation). Singapore has a resident population of roughly only 5 million, so 36,500 job adds and high tourism rates will have an measured impact on the economy. Further, Singapore also has an open policy of importing highly-skilled labor to meet its growing demands (1.5 million immigrants from China, India, and Malaysia).

The demand for highly-skilled labor is particularly prevalent in the financial services, construction and energy sectors. For the third consecutive year, the World Bank has ranked Singapore as the easiest place in the world to do business and the fundamentals behind that calculation make Singapore a likely destination for relocated financial services as a result of global industry regulation. Singapore is already Asia’s leading OTC commodity derivatives hub with more than 50% of the region’s volume. According to Singapore’s Ministry of Trade and Industry, increased intra-regional trade will likely result in the need for upwards of $8 trillion of infrastructure and insurance investment over the next decade, so the government has been busy making concessions to accommodate this growth. In the construction sector, the government has set aside 25% ($250 mil.) of the National Productivity Fund for manpower development and technology adoption. In the energy sector, Singapore is developing a facility to store liquefied natural gas to reduce dependence on imports from neighboring countries where the pricing outlook is uncertain. All in all, Singapore is making moves in line with our TAIL thesis that Asian markets will continue to take share from the U.S. and the EU in the global economy.

Risks: Moderate in the Absolute; Negligible Relative to the Downside Risks of Other Advanced Economies (U.S., Spain, France, Greece, Mexico)

So what are the downside risks to the bullish case on Singapore’s economy? With the equity market up only 1.9% YTD and far from the top of the performance leaderboard, this leading indicator suggests there are risks associated with this thesis. Those risks include: an expedited move in the Singapore Dollar vs. the U.S. Dollar, which would further dampen export prospects to that market; and a potential for a hiccup in pharmaceutical manufacturing, which itself is a very volatile industry subject to large production swings by big companies such as Sanofi-Aventis SA.

With 19% Y/Y GDP growth and CPI currently running at the highest level since Dec. ’08 (+3.24% Y/Y), the Singapore Dollar is in a hawkish setup ahead of the next Monetary Authority of Singapore policy review in October (the Monetary Authority uses the Singapore Dollar instead of interest rates to manage inflation). The currency rose as much as 1.2% on the day of the last MAS meeting back in April when the board allowed a revaluation of the Singapore Dollar and shifted to a stance of gradual appreciation. If the currency continues to strengthen against the U.S. Dollar from here, export competitiveness to the U.S. market may come under pressure. SGD-USD has gained 1.5% against the last two weeks alone and our Short the US Dollar thesis makes this trend likely to continue. If the euro appreciates further from here, however, relative strength in that currency may offset a portion of this pressure. Fifty-eight percent of the U.S. Dollar Index is Euros, further U.S. Dollar debasement from here will provide reasonable support for the EUR-USD, which is teetering on a TREND line breakout above $1.28. SGD-EUR supports this view, down (-0.3%) in the last two weeks.

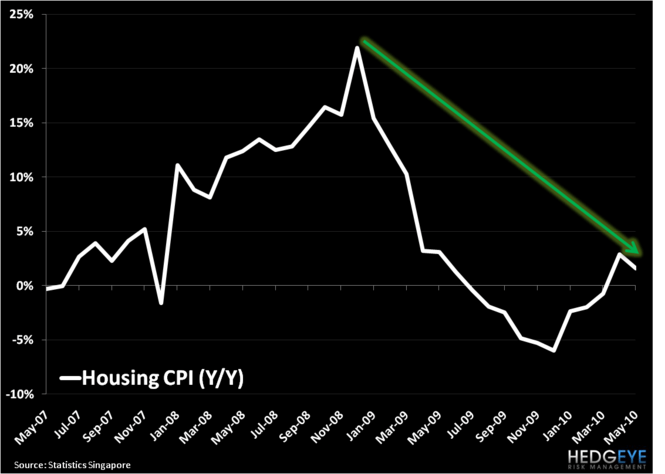

A second risk to Singapore’s go-forward outlook is the prospect of an eventual overheating in the housing sector. An alarming report by CIMB suggests that overall housing affordability in Singapore is now inching closer to the banks’ mortgage-to-income threshold ratio, after a 10% YTD increase in private home prices which has elevated those levels above the 1996 peak. While appropriate cause for alarm, further analysis suggests that housing prices are far from a China-like bubble. First, housing CPI (the largest component of the consumer price index) has lagged overall inflation for the past 12 months. From the November 2008 peak-of-peaks, housing CPI has experienced a (-4.2%) decline. Furthermore, a marginal deceleration of Y/Y growth in the latest housing CPI reading suggest that concerns are likely overdone for now. In the event that they aren’t, however, expedited appreciation in Singapore’s housing market will likely put more pressure on the MAS to raise the value of the currency – which would further augment our bullish consumption thesis. Moreover, immigration policies designed to expand Singapore’s population by over 50% in 10 years suggest there won’t be any “ghost towns” on the island anytime soon.

Conclusion: Long EWS; Long SGD-USD

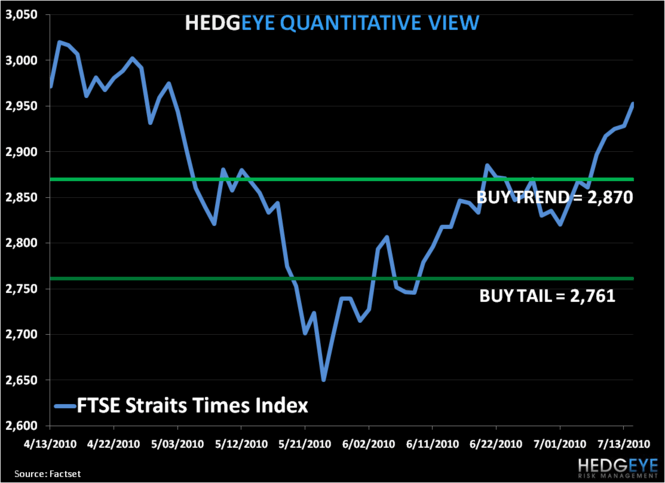

In summary, we like economies in the back half of 2H10 and 2011 that are setup to accelerate domestic consumption to offset a decline in global trade and industrial production (China, Brazil, Singapore). Keep in mind, however, that every market and currency has its price and with growth poised to slow globally, relative economic performance will matter even more in 2H10. We are no longer in a “rising boat lifts all tides” investment environment, so we’re waiting for price confirmation in markets like China and Brazil on the long equity side. From a quantitative standpoint, Singapore’s price is right. We expect Singapore’s FTSE Straits Times Index to outperform many global equity markets throughout the remainder of the year. From a currency perspective, Singapore’s hawkish economic setup and low deficit-to-GDP ratio (2.6% in 2010) makes the Singapore Dollar a strong FX play - particularly relative to the $USD.

Darius Dale

Analyst