This insight was published on July 14, 2010. RISK MANAGER SUBSCRIBERS have access to SELECT MACRO content in real-time.

__________________________________________________________

Position: Long the British Pound via the etf (FXB); Short US Dollar (UUP)

“Put your hand on a hot stove for a minute, and it seems like an hour. Sit with a pretty girl for an hour, and it seem like a minute. THAT’s relativity.”

-Albert Einstein

When discussing currencies it’s worth repeating that we’re betting on the “relative” strength of one currency versus another. Currently we are bullish on the British Pound (GBP) versus both the USD and EUR; we expressed this conviction by buying the etf FXB in our virtual portfolio on 7/12.

The Debt Road

Taking a step back, yesterday in the Early Look Keith wrote: “This morning’s run of global macro news reminds me of three things:

1. Sovereign Debt issues are here to stay

2. American Austerity is on the way

3. Global growth is going to continue to slow”

In summary, these three points reflect much of what our macro team has focused on in our research over the last 6th months: unchecked government debt and deficit imbalances (globally) will come home to roost. Over the balance of this year the price action across global markets and multiple asset classes has swung considerably alongside fears of sovereign default in Europe, especially from those nations so affectionately named under the acronym “PIIGS” (Portugal, Italy, Ireland, Greece, and Spain) or “Club Med” states. We’ve track this fear in the form of bond yield spreads, CDS prices, currency moves, and equity market performance, and played Europe’s Sovereign Debt Dichotomy (our Q2 Theme) by shorting Spain (via the etf EWP) and being long Germany (EWG) in 1H10.

We now think that while Europe’s Sovereign debt issues are by no means rearview (Portugal’s debt was downgraded by Moody’s yesterday), the spotlight concerning the risk of a government piling debt up debt will move to the US, a position encapsulated by our Q3 macro theme of American Austerity. (Note: this position is very quickly becoming consensus).

As it translates to our view of global currencies, we believe the USD is setting up to give back much of its gains YTD. Should this be the case, and in light of the continued sovereign debt fears in Europe, we could see the Pound as the relative beneficiary of this currency trade.

Our bullish positioning on the Pound follows two main threads:

1.) The Austerity measures issued by the new UK government of PM Cameron and Chancellor of the Exchequer Osborne show their intention to rein in fiscal imbalances. We think fiscal austerity should boost investor sentiment and future growth in the UK despite meek growth prospects this year and next.

2.) For the intermediate term TREND we see continued political and economic headwinds in the US and throughout certain Eurozone countries; we believe the Pound stands to benefit on a relative basis from the downward pressure on the USD and EUR.

Bullish on the UK

We’re bullish of PM Cameron’s conservative government that took office in early May. The new tide of “austerity” that his government has issued, with initial measures proposed in an Emergency Budget released on June 22nd by the Chancellor of the Exchequer, George Osborne, spell significant spending cuts and incremental consumption tax hikes to trim fat and boost revenue in Britain. With a budget deficit (as a % of GDP) of some 11% in 2010, Britain is proverbially biting the bullet (now) to shore up its fiscal house, a move we believe will better position itself for future growth and appreciate the value of the Pound.

The UK’s main austerity measures include:

- A 25% cut in the budgets of government departments starting April 2011 through 2015 (a spending review is expected for released in October)

- Tax on banks with liabilities greater than £20 Billion (the tax is expected to generate approx. £2 Billion annually)

- Increase to the Value Added Tax (VAT) from 17.5% to 20% starting January 2011

- Increase in capital gains tax for higher tax bracket earners, to 28%. No change (18%) for low to middle income earners

- A 2 year wage freeze for all but the lowest paid among Britain’s 6 million public servants and a 3 year freeze on benefits paid to parents for rearing children

- Cuts to the housing benefit and disability allowance

- Decrease in corporate taxes, staggered over 4 years from 28% to 24%

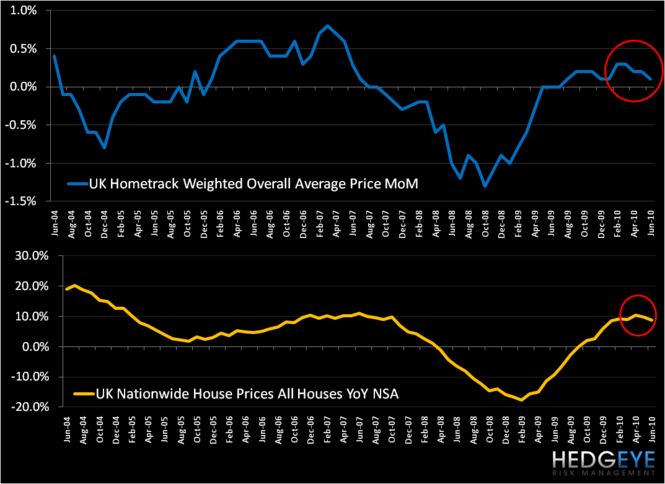

- We are by no means bullish on the UK economy across the board (it’s one of the main reasons we haven’t bought UK equities). The housing market is one particular area of concern. To the joy of many home sellers (and real estate agents), Cameron’s government did away with Home Information Packs (HIPs) in late May, documents required of homeowners to sell their properties that many complained simply increased the “cost and hassle of selling a home”. However, scrapping HIPs has increased the supply of homes on the market over the last months, and consequently dampened prices. Recent surveys from Hometrack and Nationwide corroborate the recent turn in prices (see chart below). Should the housing market take a second dip, we’d expect to see significant downward pressure on the consumer.

Secondly, the government’s go-forward relationship to the country’s all-important banking sector is still unclear. Cameron’s policy will need to find the appropriate balance between levying a bank tax (which the UK has spearheaded ahead of global backing) and guarding against excessive risk taking by banks while not running banks (and financial professionals) to tax friendly havens, like Switzerland. Decreasing corporate taxes is a start.

Bottom Line

Growth: we don’t expect to see significant growth in the UK in the next year. GDP is projected at 1.2% in 2010 and 2.0% in 2011 by Bloomberg consensus, and we think that consenus is reasonable.

Unemployment: the UK’s nominal unemployment rate has shown improvement over the last two months, dropping 10bps to 7.8% in the latest reading.

Inflation: inflation pressures appear to be waning—CPI readings have come in over the last months, registering 3.2% in June Y/Y.

Currency: we’re bullish on the Pound outright because we think that capital and currency markets will favorably price the austerity measures Britain is taking to shave down the government’s budget deficit. We think the Pound-USD can continue to trend higher from its near-term bottom of $1.43 on 5/20 (see chart below).

Our TRADE line of support for the Pound-USD is $1.48 with TRADE resistance at $1.53.

Matthew Hedrick

Analyst