Position: Long the British Pound via FXB

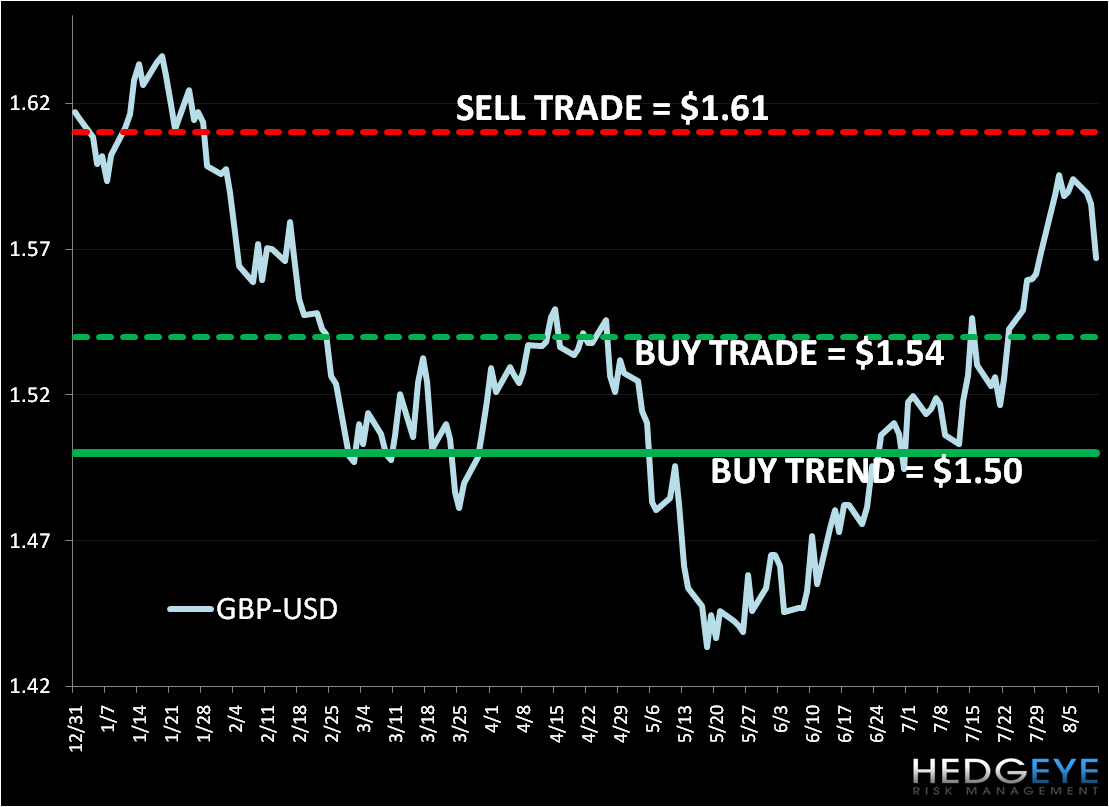

With the pullback in the GBP-USD today towards our TRADE line of support at $1.54 we bought the British Pound via the etf FXB (see chart below). As we’ve noted in recent work, we expect an economic slowing in Europe beginning in the second half of the year. Specifically in the UK, we’re cautious on the housing market.

The UK’s unemployment picture has yet to greatly excite in either the positive or negative direction over the last months (see chart). However, employment data out today showed that the number of people unemployed in the UK fell by -49K to 2.46 Million in the three months to June, the biggest drop in three years, yet the overall rate of unemployment remains unchanged from the previous month at 7.8%. Jobless claims dropped -3.8K versus consensus expectations of -17K.

Following our bearish outlook on the US Dollar, we believe that currencies like the Pound stand to gain on the other side of the trade. Below, we provide our TRADE (3 weeks or less) and TREND (3 months or more) lines for the GBP-USD. Notably, our models don’t see resistance until the $1.61 level.

Matthew Hedrick

Analyst