This insight (THE DAILY OUTLOOK) was published on August 11, 2010. The Daily Outlook is published every trading morning. RISK MANAGER SUBSCRIBERS have access to SELECT MACRO content in real-time.

______________________

TODAY’S S&P 500 SET-UP

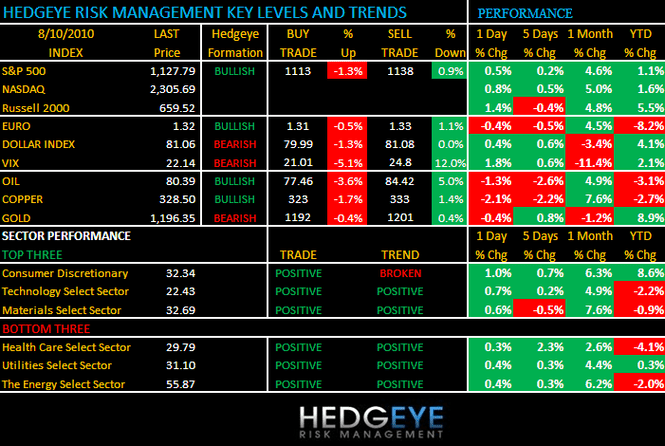

As we look at today’s set up for the S&P 500, the range is 39 points or 2.0% (1,099) downside and 1.5% (1,138) upside. Equity futures are trading below fair value - disappointing data out of China and Japan has set the early tone and Europe is broadly lower. Today's focus will be trade and budget data for July.

- ADVANCE/DECLINE LINE: -1400 (-2766)

- VOLUME: NYSE - 980.83 (+24.14%)

- SECTOR PERFORMANCE: 3 sectors positive - XLU, XLV and XLP - flight to safety

- MARKET LEADING/LOOSING STOCKS: Akami +4.86, XL Group +2.68 and ADV Micro (7.95%) and Western Digital (6.12%)

EQUITY SENTIMENT:

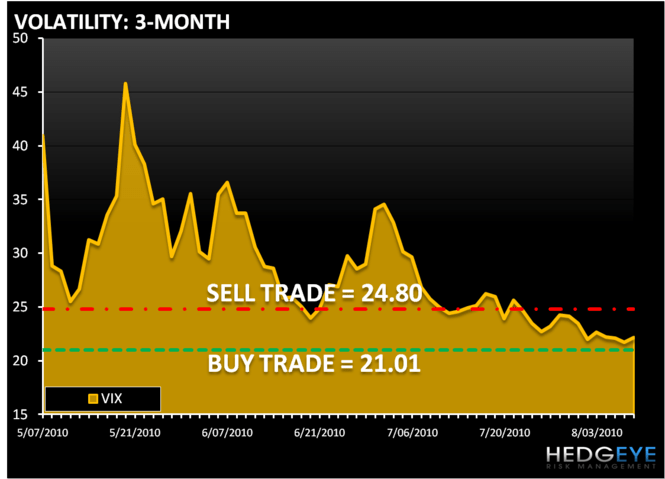

- VIX - 22.37 1.04% - The VIX now up for 2 days and bearish for equities.

- SPX PUT/CALL RATIO - 2.49 up from 2.01 trending up (not seen since March) (low on 07/15/10 of 0.87)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD - 24.87 -0.913 (-3.541%)

- 3-MONTH T-BILL YIELD .15% Unchanged

- YIELD CURVE - 2.2974 to 2.2359

COMMODITY/GROWTH EXPECTATION:

- CRB: 272.28 -0.84% (down for the last 4 days)

- Oil: 79.35 1.51%

- COPPER: 331.25 -1.24% (currently trading at 327.25 below 332 - BEARISH for growth expectations

- GOLD: 1,196 -0.32% (trading down for 3 days)

CURRENCIES:

- EURO: 1.3117 -0.84% - (trading down for 3 days)

- DOLLAR: 80.799 +0.11%) - (trading up for 3 days)

OVERSEAS MARKETS:

- ASIA - Asian markets fell after the Fed disappointed saying it would reinvest money from maturing mortgage bonds in government debt. Japan fell (2.58%) broadly - The strong yen is hurting exporters and a slowdown in the US; worries about the domestic economy also dampened sentiment as core machinery orders came in below forecasts

- EUROPE - European are trading sharply lower following weakness across Asian and in reaction to the Fed's comments that the US economy is slowing and took new step to aid the economy.

- EASTERN EUROPE - Trading lower - Russia down another 1.23% and Hungary down 0.84%.

- LATIN AMERICA - Lower but Peru trading higher for the 2nd day - Argentina down 1%

- MIDDLE EAST/AFRICA - Mostly lower with Saudi Arabia down 1.46%

Howard Penney

Managing Director