This insight was originally published on June 22, 2010. MACRO intra-day updates are available to RISK MANAGER SUBSCRIBERS in real-time.

MACRO: HOUSING FIZZLES EARLIER THAN EXPECTED SETTING STAGE FOR WORSE DOWNTURN

_____________________________________

THE BOTTOM LINE

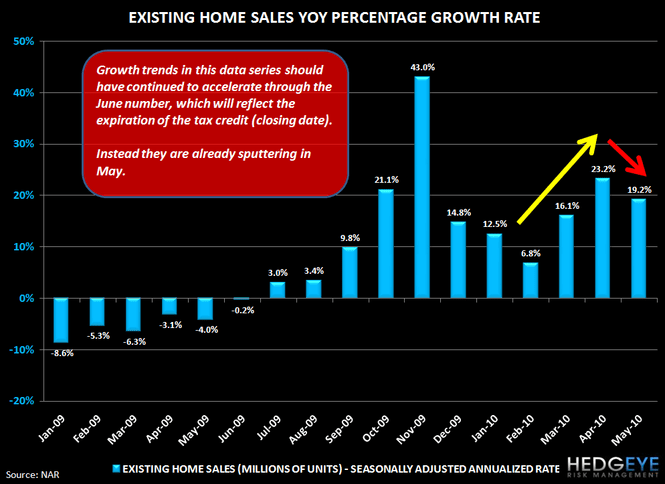

May existing home sales were much worse than expected in spite of the continued effect of the April 30 tax credit expiration pull-forward. May sales came in at 5.66 million (seasonally adjusted annualized rate) down from 5.79 million in April (revised a tad from 5.77 million). Expectations were for sales to rise north of 6.2 million units. Sales coming in 9% below expectations reflects a major incremental negative datapoint.

Summary

Remember that this May print is a lagging indicator as it reflects deals closed two to three months ago (Mar/Apr) because of the 30-60 day lag between signing and closing.

In our view, the relevant benchmark is how it compares with October 2009's print of 5.98mn. Against that measure, it's down considerably (5.66). The original tax credit expired in November, 2009, putting October 1 month ahead of that expiration. The current credit (for closing) expires June 30 (April 30 for signing), which means 1 month ahead equals May.

In other words, it's now clear that tax credit round two is having a less substantive effect on sales than round one did back in late-2009.

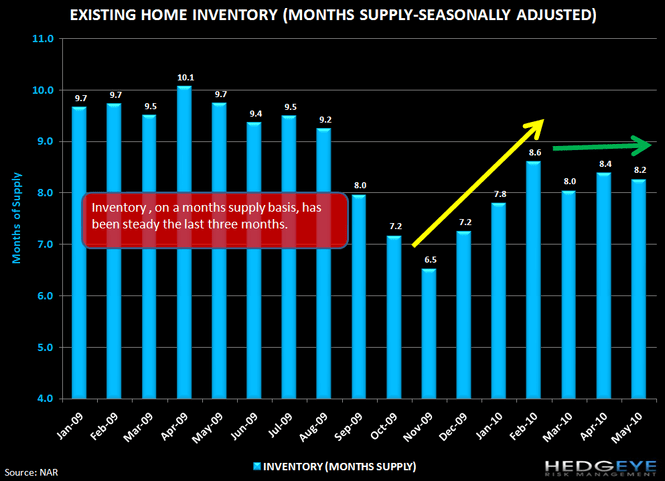

Inventory, on a units basis, fell a modest 3.4% to 3.89 million units from 4.04 million units in April.

Inventory, on a months supply basis, fell slightly to 8.25 months from 8.4 months last month. While inventory is down nominally on a months supply basis, this is somewhat misleading because its keying off an artificially high May 2010 sales rate. If we assume that the same dropoff in sales occurs following this tax credit expiration as followed the last tax credit expiration we can expect to see a sales rate of 4.25-4.5mn a few months from now. Meanwhile, inventory is at 3.89mn units. In other words, inventory could rise to 10-11 months or higher very shortly.

Our view is that this pull forward of activity is setting the stage for a much weaker-than-usual summer housing environment. Housing-sensitive stocks could be at risk heading into the 2H10 and 2011 time frame.

We have an extensive report coming out on this topic on Friday for subscribers and prospects of our Financials Vertical, which we will summarize on a conference call at 11am on Friday.

Joshua Steiner, CFA

Managing Director

Allison Kaptur

Analyst