At this point the consensus thinking is that EAT had a difficult quarter and every indication is that they did. The sale of OTB and the extra week will add to the confusion.

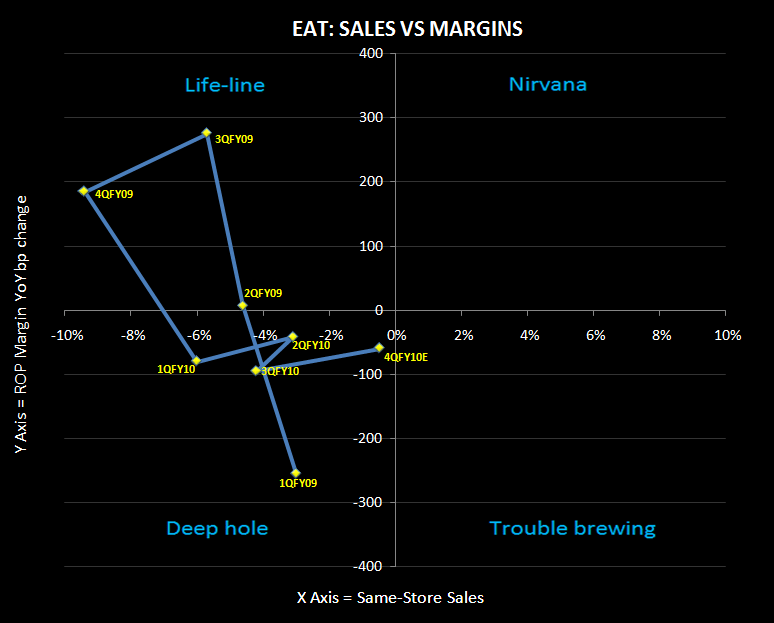

So far in the 2Q earnings season, with few exceptions, there have not been many restaurant companies that didn’t have a difficult quarter. So will EAT’s quarter be much worse than consensus and how will the stock react? As you can see for our sigma chart on EAT, the company has been operating in the “deep hole” for all of FY 2010 and this quarter will not look much better. Here is a look at guidance and key focus points ahead of earnings on Thursday.

- The current $0.46 consensus estimate is largely meaningless although $0.45 is a better number.

- The 2011 outlook and commentary on current trends will be the focus of the call.

- Progress on margin initiatives is important for restoring confidence as sales trends remain challenged.

- The street is so bearish that the number of shares sold short doubled during the quarter.

SAME STORE SALES

- To maintain or sequentially improve two-year average blended same-store sales (52 weeks vs 52 weeks), Brinker will need to post roughly flat comps or better for 4QFY10. We have sales down 3-4% (on a 52 week vs 52 week basis) so this will be a net negative.

- According to Factset, the Street is expecting a company same-store sales number of 0%, would seem to include the 53rd week. The nine estimates comprising this Factset estimate are greatly varied; the highest estimate is +5.3% and the lowest is -4.3%.

GUIDANCE

- Same-restaurant sales of 1 to 2% for current fiscal year includes 53rd week.

- Full year EPS guidance on a continuing operations basis before special items of $1.20 to $1.24 (consensus at $1.21), implying a range of $0.45 to $0.49 (consensus is at $0.46) for the fourth quarter.

- Lower-than-normal expenses such as insurance expense, property tax, utilities, and vacation expense favorably impacted margins be approximately 110 bps in 4QFY09.

- The long-term goal is to double fiscal 2010 consolidated EPS before special items by 2015 with 10 to 12% EPS growth is for fiscal years ’13 through ’15.

- Minor levels of sales growth of approximately 1 to 2% same-restaurant sales.

- 500 basis points of margin expansion at Chili’s offset by 100 basis point depreciation impact for a net 400 basis point impact to operating margins over the next three years.

- Investment in CapEx will only continue as proof of returns warrant.

- Free cash flow will be reinvested into the business, used to reduce debt, pay dividends and, to the extent cash remains, reinstate our share repurchase program.

- The cash balance will be put to work and the company will likely carry levels to meet working capital needs of approximately $50 million, barring any significant event in the future that may suggest a need for higher liquidity levels. (Cash balance at 3/31: $181.9m)

- On The Border proceeds will be put to use…for share repurchase to quickly rebuild the EPS base

- “We will receive approximately three to $6 million of fees for providing support services to the acquirer, Golden Gate.”

- We will extend our portfolio to have 425 Chili’s restaurants internationally by 2014, cementing us as the dominant player.

OTHER INTERESTING COMMENTARY/NOTEWORTHY POINTS

- We will fuel our growth through equity investments and franchise partnerships, taking advantage of demographic and eating trends that will only accelerate In the rest of the world over the next decade.

- Same-restaurant sales for the quarter at our international restaurants increased nearly 1%, and we’re further encouraged by the economic stability of many of the countries that we do business in today.

Howard Penney

Managing Director