This guest commentary was written on 9/16/20 by Mike O'Rourke of JonesTrading.

Today represented the conclusion of the first FOMC meeting under the updated monetary policy framework. The FOMC statement represented a rewording of the previous FOMC statement to match the new framework, but nothing changed from a substantive policy perspective.

Surprisingly, the market rallied on the statement release only to fail when buyers recognized there was nothing materially new. We believe it is almost pointless to break down what transpired today because nothing did. The first thought that comes to mind is Tommy Callahan’s “guarantee” in the movie Tommy Boy.

Chris Farley tells his prospective customer, “Guy puts a fancy guarantee on a box 'cause he wants you to feel all warm and toasty inside,” then he goes on to explain how you are being duped into buying a guaranteed piece of, well, you know.

The Federal Reserve reshuffled the language surrounding policy, made it more convoluted and confusing, but dressed it up to sound more convincing, or in Chairman Powell’s words “powerful & confident.” Powell had to repeatedly refer to the prepared text so as to not trip himself up in the Fed’s attempt to sell something used as new.

The situation is so inane that amidst the unofficial promise to not increase the Fed Funds rate for the next forty months, two FOMC members dissented in different directions in favor of equally incredibly vague criteria for interest rate movement. It is the equivalent of arguing over the upgrades you want in the car you are going to buy three years from now.

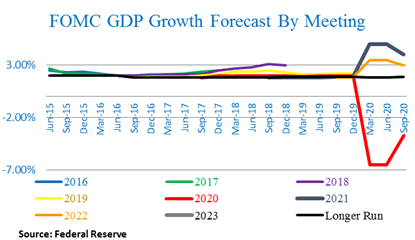

Nonetheless, for the record, we will break down what has transpired. First, the headlines all read that the Fed promises low rates until 2023. This is a mechanical move, nothing more. As 2020 draws to a close, a new year is added to the forecast.

It so happens that the forecast goes out 3 years. From our perspective, if the official forecast went to 2024, then the promise would have extended until then. If the forecast went out 5 years, the FOMC would have then signaled at least a single rate hike, or maybe even a couple, in an attempt to portray some level of competence that their policies will work.

Recall that the last easing cycle started in late 2007, and the first Fed Funds rate increase did not occur until the end of 2015, which was 8 years later. The second increase did not occur until a year later.

The policies the Federal Reserve pursued during that cycle did not create consumer price inflation. There is no reason to believe they will create that inflation this time.

As far as the linguistic acrobatics in the statement are concerned, according to the July statement, “In light of these developments, the Committee decided to maintain the target range for the federal funds rate at 0 to 1/4 percent. The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.

The new language (which replaced it) should remain standard for the foreseeable future and reads as follows, “The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.”

That new guidance has been incredibly well telegraphed for months and was precisely as expected. In the 10 years of uninterrupted economic expansion prior to March of this year, PCE inflation has only exceeded 2% in 26 of 120 months. Core PCE has only exceeded 2% in 13 of 120 months.

Therefore, if the next expansion were to mirror this past expansion, it is fair to say this policy indicates the FOMC will not raise rates for a decade or more. The history also proves that the Fed policies are not successful in creating consumer price inflation (but they are remarkable for asset price inflation). Rather than acknowledge its policy failures and trying to find new policies to foster the desired objective, the Fed continues to limit itself to asset purchases and zirp.

Therefore, everyone’s base case should remain that the Fed will not be raising interest rates for years. If they don’t do anything, one has to wonder if there is even a need for the Federal Reserve anymore.

We are back to the static monetary policy environment that persisted for most of the last decade, the only difference is that the stock market is far more expensive today.

There were two other notable observations from Chairman Powell’s press conference today. The first is that the inflation target guidance predominately apples to the Fed Funds rate and not the asset purchases.

Imagine a decade or longer of asset purchases - there are policy makers who might ignorantly make such a move. The other is that the Fed and private forecasters have some type of additional fiscal stimulus modeled into the current economic recovery projections.

As we all know, such stimulus is yet to come to fruition. The last important factor to note with regard to the Fed’s new framework is that the Chairman left himself the latitude to pursue policy as he wishes (as Fed Chairs have been doing for some time).

Although the 2% inflation target is pretty clear, the Chairman continues to highlight that “non-formulaic flexible form” 2% inflation, which allows him and his colleagues to interpret data however they wish.

Frequently in the past, we have referred to this as “policy by whim,” and again, there is nothing new here either.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Mike O'Rourke, Chief Market Strategist of JonesTrading, where he advises institutional investors on market developments. He publishes "The Closing Print" on a daily basis in which his primary focus is identifying short term catalysts that drive daily trading activity while addressing how they fit into the “big picture.” This piece does not necessarily reflect the opinion of Hedgeye.