"There are two ways to conquer and enslave a nation. One is by the sword. The other is by debt."

-John Adams, US President

Yesterday was another great day for our short position in the US Dollar. It was a terrible day for our short position in the SP500. As perverse as this may sound, both the US stock and bond markets all of a sudden love the idea of America losing its status as the world’s reserve currency as we enslave our citizenry with debt.

The sad news is that despite both America and Japan resorting to “quantitative easing” in the recent past, some professional politicians in this country have learned nothing from these mistakes. So if you have any American friends who get all amped up and cheer the stock market on when they hear “rumors of QE2”, please take a step back, take a deep breath, and tell them to be careful of what they hope for.

Hope, of course, is not an investment process. Hope is not going to make America’s debt and deficit problems go away. Neither will the Paul Krugman type fear-mongering that got both the US and Japan in this mess to begin with. Before the internet, dinosaurs, and YouTube, Krugman’s fear-based model provided the false premise that no one would hold him accountable to his recommendations. No matter where the Krugmanites go, here it is:

“So never mind those long lists of reasons for Japan’s slump. The answer to the country’s immediate problems is simple: PRINT LOTS OF MONEY.”

-Paul Krugman (1997)

To be balanced, it appears that by 2006 when he penned an Op-Ed titled “Debt and Denial”, Krugman showed some evolution in his thought process:

“But serious analysts know that America’s borrowing binge is unsustainable. Sooner or later the trade deficit will have to come down, the housing boom will have to end, and both American consumers and the US government will have to start living within their means.”

-Paul Krugman (2006)

Sadly, now that it’s 2010 it’s clear that Krugman has forgotten the fiscal discipline he mustered while he was Bush-bashing the double edged sword of deficits and debt. He’s right back to his 1997 form in recommending that his Princeton pal Heli-Ben Bernanke “prints lots of money.”

Much like Nassim Taleb did in taking the puck right to the net on another Fiat Republic alum from Princeton in the Huffington Post last night (“The Regulator Franchise – Or the Alan Blinder Problem”), at 11AM EST today, my defense partner, Daryl Jones (aka Big Alberta) will be joined by our macro team here in New Haven, CT taking the Krugmanites and monetarists alike to task.

As much fun as we like to have calling people out (including ourselves), this time it’s game time. We’re dropping the mitts with those debt and deficit sponsors who are putting this country’s national wealth and security at risk.

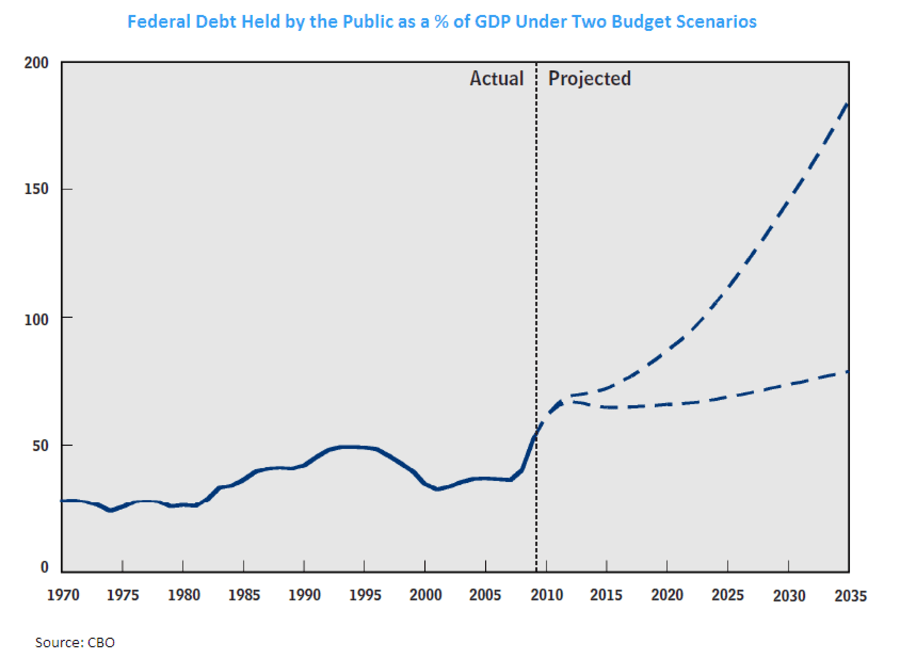

The primary implication from our conference call will have to do with our #1 concern versus consensus right now – US economic growth. A build-up in debt on the federal balance sheet proactively predicts a dramatically different future as it relates to the underlying growth in America. If the last 200 years of data has shown us anything, it is simply that those nations with high debt balances either default or grow well below mean rates of economic growth as long as debt ratios remain high.

We’ll have 45 slides of hard data and forecasts today. We also have a 101 slide presentation titled “Housing Headwinds” that our Financials team, led by Josh Steiner, has compiled to back up the embedded conclusions we are making about US GDP growth; namely that US Housing prices could drop -15-20% from this summer’s bear market cycle-peak in the Case-Shiller Index. Here are the details for the call:

"Should U.S. Government Debt Be Rated Junk Status?"

Key topics to be discussed:

- The implications for the U.S. economy of the massive build up of debt

- Various federal budget scenarios and their key drivers

- GDP growth implications based on accelerating debt balances

- Implications to the deficit under different interest rate regimes

- Comparison of the U.S. to the PIIGS on key ratios

- Appropriate investment vehicles for this long-term TAIL theme

If you would like to reserve a spot on the call, please email sales@hedgeye.com. <mailto:sales@hedgeye.com>

Back to today’s risk management setup. We got a lot of questions yesterday as to when/where I was a short seller of the SP500 (SPY). Once the SP500 broke out above my immediate term TRADE line of resistance (1118) yesterday, that resistance level became very short term support – so I watched and waited. I’d like to short the SP500 from 1133 all the way up to my Bear Market Macro line of 1144. For now, that’s the plan.

For any modern day Risk Manager of real-time market prices, the plan needs to be that the plan is going to change. We’ve been bearish on the US stock market since April and bearish on the US Dollar since June. I may have missed half of the bear market bounce that the SP500 has had since its July 2nd low, but I don’t intend on missing this next selling opportunity as we enter the most critical stage of professional politicians Enslaving America with debt.

We didn’t sell everything yesterday in the Hedgeye Asset Allocation Model, but we took our cash position back up to our highest level of 2010 at 79% (up from 58% Cash on July 2nd when the SP500 bottomed at 1022).

Best of luck out there today,

KM