DEEP DIVE IN MACAU'S JULY NUMBERS

July total revenues came in at $2.04BN, increasing 70% YoY, while total table revenues increased 73%. Mass revenues increased 39% YoY while VIP revenues grew 87% YoY, compared to only 55% growth in Junket RC volumes. Similar to June, easy hold comparison contributed to some of the big growth we saw this month. Adjusting for direct play levels, we estimate that VIP hold was 3.18% in July vs. 2.64% last year. If we normalize for hold, VIP table revenues would have been "only" up 55% YoY this month and total market growth would have been 49%. August will have a tougher comp, as hold for August 2009 was normal at 2.8% and total revenues increased 18% last year.

YoY Table Revenue Observations

LVS table revenues increased 51% with growth coming from a 68% increase in VIP revenues and only a 27% increase in Mass revenues.

- Sands grew 1%

- VIP revenues declined 7% despite a 22% increase in Junket RC volume. Assuming 12% direct play volume on VIP, we estimate that hold for July was only 2.4%.

- 14% increase in Mass revenues

- Venetian was up 39%

- VIP revenues increased 44%

- Mass revenues increased 32%

- Junket RC increased 18% YoY. Assuming 22% direct VIP play volume, we estimate that hold for July was 2.7%. However, last July, assuming 20% direct play, the hold percentage was even worse at 2.55%.

- Four Seasons growth was almost infinite this quarter, since they experienced negative hold in July 2009. Volume was very low back then so a big loss to one player was all it took for that to happen.

- Mass revenues grew 67%

- Junket VIP RC increased 323% to $921MM

- If we assume over 50% VIP turnover came from direct play, hold was 3.27%.

Wynn Macau/Encore table revenues were up 74%, driven by a 82% increase in VIP revenues and a 44% increase in Mass revenues

- Junket RC volume increased 57% compared to a market increase of 55%

- This past quarter, direct play volumes at Wynn were roughly 11% of total VIP. Assuming July had a small uptick to 12% , hold was a high 3.3%. Last year's hold comp was also easy - 2.7% assuming 13% direct VIP play. While the Encore addition doesn't appear to be fueling materially above market growth, we can't really complain about +80% YoY growth.

MPEL table revenues grew 42% with the growth fueled by 91% growth in Mass and 36% growth in VIP

- Altira was up 8%, due to a 8% increase in VIP revenues and a 3% increase in Mass.

- VIP RC was down 5% YoY. Despite Altira holding low in July (2.5%), last year's hold was even worse at 2.2%.

- CoD table revenue increased 63% YoY, driven by 118% growth in Mass and 54% growth in VIP revenues

- Mass revenues were $37MM

- Junket VIP RC increased 65%

- CoD played lucky in July, but they also played lucky last year. If we assume 18% direct play at CoD, hold was 3.5% in July vs. an estimated hold of 3.7% last year.

SJM table revenues grew 138%

- Mass was up 34% and VIP was up a massive 250%

- Junket RC volumes increased 97%

- SJM's hold was roughly 3.25%, compared to a very low hold 1.84% in July 2009. August will be another easy hold comparison month since last August's hold rate was only 2.1%.

Galaxy table revenue was up 107%, driven by a 114% increase in VIP win and a 58% increase in Mass

- Starworld's table revenue was up 120%, driven by 126% growth in VIP revenues and 58% growth in Mass

- The Group RC volumes were up 76% while Starworld RC volumes increased 95%. Starworld's July hold was normal -roughly 2.85% vs. 2.45% in July 2009. Easy hold comparisons through (~2.5%) September should continue to allow Starworld to print outsized YoY growth.

MGM was the only concessionaire to report a decline in YoY table revenue, down 5%.

- Mass revenue growth was 40%, while VIP fell 14%

- VIP RC grew 10%

- The drop in revenues was partly driven by a difficult hold comparison - 3.3% last year - and an estimated low hold in July of 2.5%. However, RC growth was definitely disappointing as MGM looks to have topped out in the 2.8-3.3BN range for RC monthly volumes since its pickup in May 2009. Hopefully for them, Mr. Kwong can bring in some new business and return the property to growth.

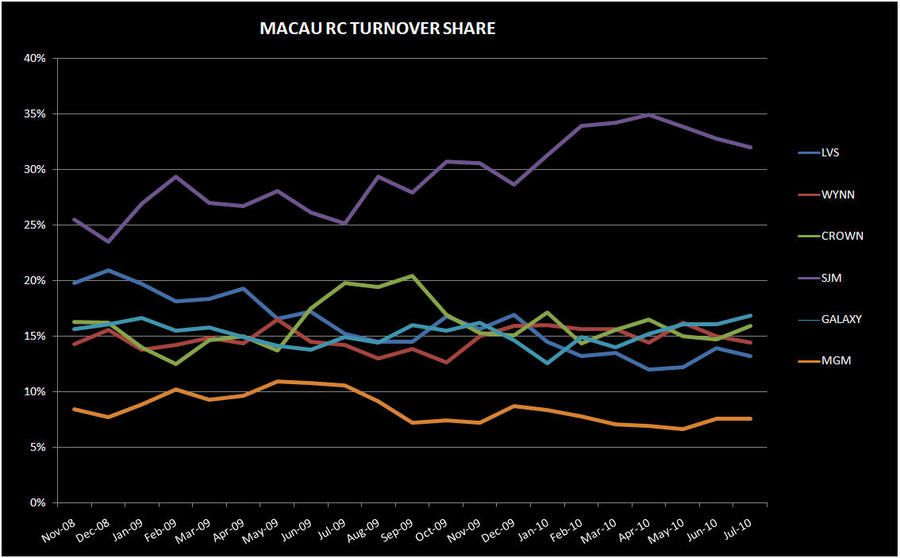

Table Market Share

LVS table share dropped 280bps sequentially to 18.4% in a reversal of last month's gains - mostly driven by bad luck on the VIP business and share losses across all 3 properties

- LVS's share of VIP revenues decreased 3.9% to 15.8% in July, while LVS's share of Junket RC only dropped 70 bps to 13.3%. This was LVS's lowest share month since May 2009.

- Mass share increased by 120 bps to 26.7%

- Sands market share continued to make new lows at 5%, down 120bps sequentially. July's sequential share loss was driven by 170bps drop in VIP share to 3.8%

- Venetian lost 130bps to 9.7% sequentially

- Venetian's share loss was entirely driven by a 160bps decrease in VIP, while Mass share gained 50bps.

- FS share lost 40bps of share to 3.6% - from an all-time high in June

WYNN's table share decreased to 14.6% from the annual high of 17.2% in June, which was still above the TTM average pre-Encore opening market share of 13.8%

- Mass market increased 130bps to 11%

- VIP revenue share decreased 4.1% to 15.8% sequentially

- Wynn's VIP share fell to 4th place behind SJM, MPEL and LVS. Although Steve would say that their share of EBITDA and Net Income on their lower share was no doubt unrivaled.

- Wynn Junket RC share decreased 60bps to 14.4

Crown's market share increased by 150bps to 14.6% in July

- CoD's share increased 310bps to 10.4% due to a 4.2% share gain VIP, which was partly offset by 30bps loss in Mass share

- Altira's share decreased to 1.5% from 4.2% in May

SJM's share increased by 240 bps to 32.8%

- SJM's share gain was entirely driven by a 400bps of share in VIP to 30.3%. August should be another good market share month for SJM given the easy August 09 hold comparison

- Mass share dropped 100bps to 40.7% sequentially

Galaxy's share rose 2.1% to 12.8%, driven by healthy hold compared to low hold in June

- Starworld's market share increased 120bps sequentially to 9.8%, due to a 130bps increase in VIP share and a gain of 20bps in Mass.

- Junket RC share increased 110bps to 14% for Starworld. Starworld should have favorable market share gains through September, given easy 2009 hold comparisons.

MGM's share decreased by 60bps to 6.9%.

- MGM's share loss can be attributed to a 80bps drop in Mass and a 50bps drop in VIP share

- RC share was flat sequentially at 7.5%

July Slot Revenue Observations

July was a good month for slots - with revenues growing 28% YoY- reaching an all-time high of $90MM

- Galaxy experienced the largest growth of 97% YoY - granted the base is immaterial at $2MM

- MGM grew 48% to $11MM

- Wynn's slot revenue increased by 47% to $21MM

- MPEL's grew 29% to $16MM

- LVS's slot revenues grew 16% to $27MM

- and lastly, SJM's slot revenues grew 15% to $14MM