This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

|

"Well, I woke up Sunday morning Kris Kristofferson |

In a moment of serene clarity, Registered Maine Master Guide Les Williams, who has more than 50 years of guiding experience, said: “Lures are for catching people,” meaning people buy lures of many shapes and colors, but the fish mostly don’t care.

And of course Les is entirely right. Witness the effectiveness of the bubble-gum colored wacky worm for snaring small mouth bass. Les is known to favor live bait, especially for catching White Perch.

In the markets, much the same dynamic applies to people as applies to fish in the inland waters of Maine.

The people chase the shiny object of the moment, the current object of attention, but may or may not actually catch fish in terms of value. Thus we see the divergence between bank stocks and, say, non-bank mortgage firms, which recently have been trading like 2008 never happened.

In the year-to-date, the KBW bank index is down 30.11%, the S&P 500 is up 6.07% and the mortgage leader Penny Mac Financial Services (PFSI) is up 48% for the year. Could it be that mortgages are correlated to interest rates? Or more specifically, is the FOMC gunning asset prices for rate sensitive exposures like housing but not boosting consumer price inflation?

H/T to Lisa Abromowitz at Bloomberg News for this nice summation of the problem: “Stimulus is going into asset price inflation, not CPI. And the build-up of ever larger asset price bubbles itself pins down the rates market... This combination creates a dangerous environment” where investors are compelled to abandon fundamentals & follow the money: Citi’s Matt King

Speaking of interest rates, last week we published a comment in National Mortgage News about the magical nonexistent rate know as “SOFR” or the secured overnight lending rate. SOFR does not actually trade in the markets, but the Fed till expects investors and financial institutions to accept it.

As we noted earlier, Fed Chairman Jerome Powell has an opportunity for another graceful policy pirouette.

How? By quietly redefining SOFR as being equal to the too-be-announced (TBA) market price for government insured MBS issued by Ginnie Mae. Problem solved.

With the equity markets trading off after the latest market surge, the FOMC has its inflation target 10x, but in the wrong part of the economy. The bull market in residential home lending is one bright spot in a skyline with a lot of clouds ahead. Commercial loan losses at banks are leading the way higher -- and fast. As we note in The IRA Bank Book Q3 2020:

|

“Even as income growth has moderated and now turned negative, credit costs rose again sharply in Q2 2020 to over $60 billion in provisions put aside for future loss. We anticipate that provisions could remain at these elevated levels for the balance of the year or longer. This implies that industry operating income is likely to go into the red in Q3 and especially Q4, when we anticipate a significant credit loss event comparable to the end of 2009.” |

The FOMC can accelerate lending with low rates, but it cannot ameliorate either the negative impact on credit years from now or the torrent of loan prepayments that could actually drive some investors in agency and government MBS into a loss.

Owners of legacy mortgage servicing also face the prospect of reduced or even negative returns due to the early return of capital to note holders. Meanwhile, residential mortgage markets face an extended boom.

"On one hand we have the old adage, 'No tree grows to the moon," writes Rob Chrisman. "On the other hand, mortgage loan originators (MLOs) and real estate agents are licking their chops given that 52 percent of young adults live with their parents. What does that tell you about the demand for housing and loans in the coming years?"

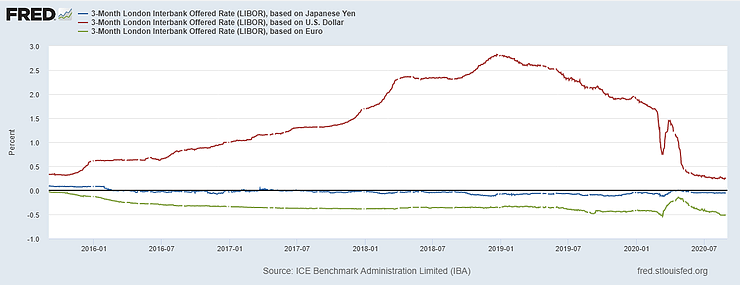

Meanwhile in Europe, the very low inflation stats for August are causing some speculation in the markets about the next move by ECB President Christine Lagarde. Most market observers believe that Lagarde will respond rhetorically, a reasonable choice for an organization that has failed miserably to achieve its stated targets for inflation and economic growth. The chart below from FRED shows dollar, yen and euro LIBOR c/o ICE.

With short-term rates in the US now close to zero, this leaves room for the ECB to experiment further with negative rates, something we suspect Lagarde is too smart to actually contemplate.

Both economically and politically, negative rates have been a failure. Going deeper into negative territory would be a mistake for the EU and Lagarde.

If anything, both the ECB and Fed need to focus on ways to inflate the income flowing to institutions and individuals before they collapse under the deflationary weight of COVID. Reducing income to investors may drive credit creation in the near-term, but the aftermath of the FOMC’s latest cycle of irrational policy actions may be quite costly to investors and financial institutions in terms of credit losses.

Volatility is the given in this market environment, so don't get nauseous when the equity markets fall 20% from recent highs. Note that as the system open market account growth slowed, the VIX spiked sharply higher and remains well above 2019 lows.

Do watch those outliers. The mortgage firms like PFSI that today trade above book value may face a very different marketplace a couple of years hence. Meanwhile, the large banks move gently sideways at -30% YTD. And for good reason.

There is no visibility on bank credit or earnings. But the Fed will be ready to add more fuel to the fire at a moments notice.

As Kris Kristofferson wrote and Johnny Cash sang decades ago, sometimes that breakfast beer tastes so good that the only choice is a second for desert.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.