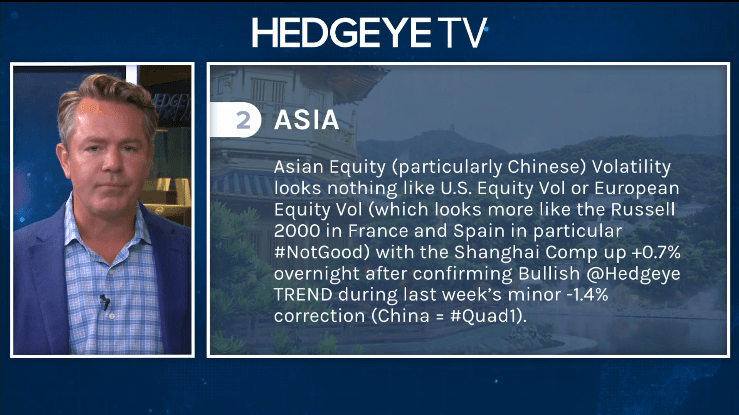

It is interesting, yet not surprising that Asia does not look like the United States in a lot of different ways.

Not the least of which is the volatility component of the Shanghai Comp as an index.

Whether it’s Shanghai or somewhere like Indonesia and South Korea (both of which were up overnight), the volatility signal in Asian Equities that we like don't look anything like the current volatility signal for things like the Russell 2000. RVX went into the mid-30’s on Friday.

It doesn’t look at all the same. That’s why were long some parts of Asia and we are short the Russell. Pay attention.

I touched on this in today's Early Look:

|

“Of course there’s always TAAS (there are alternatives to SPY) somewhere. The Long Bond (10yr Treasury) was flat week over week and didn’t feel the pain that being long something like the Russell 2000 (IWM) has across the Full Investing Cycle. Russell (IWM) was -2.7% on the week to -11.8% from its Cycle Peak (Q3 of 2018) and is only +5.7% in the last 3 months. The Financials (XLF) were up +0.3% last week but are dead money flat at 0.0% return in the last 3 months. Being long something like Chinese Stocks (Shanghai Comp is +14.9% in the last 3 months) and selective Emerging Equity Markets has absolutely pounded the US “Value” play of Long Russell and/or Financials.” |