|

Below is a brief excerpt transcribed from Friday's edition of The Macro Show hosted by Hedgeye CEO Keith McCullough |

The dollar was down initially a little this morning, and then went up on a “better than expected” jobs report on the headline Unemployment Rate.

To be clear “better than expected” means absolutely nothing to me. What matters is the Rates of Change.

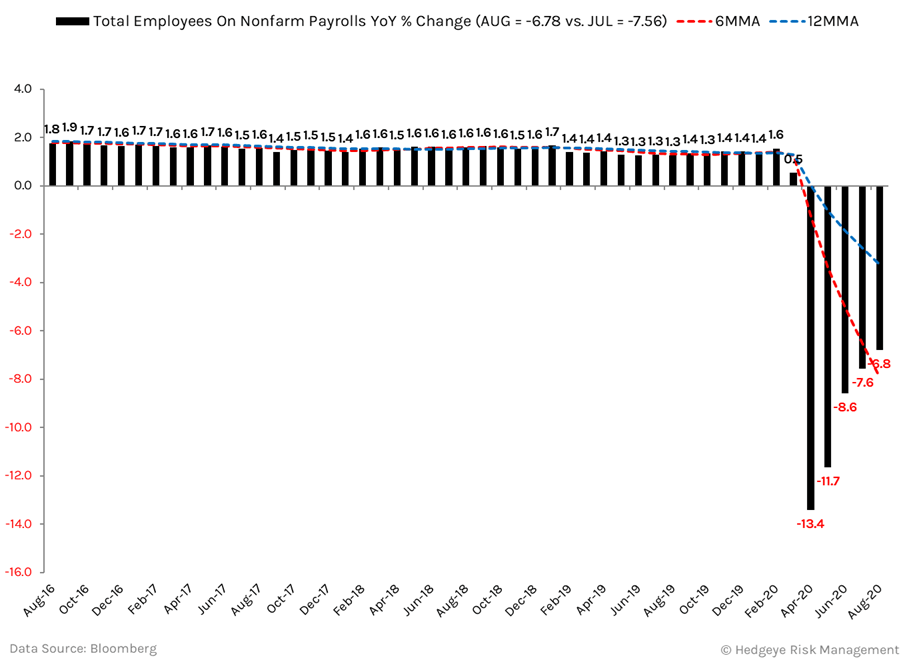

Take a look at the unemployment report.

This is what they call the “V-Shaped” Recovery.

This is the Year over Year Rate of Change in Non-Farm Payroll Growth. Try looking at the Rate of Change and figuring out if it is going up or down on a Year over Year basis?

You look at it and say “Wow, it’s not down -13.4% anymore!”

Well it’s not even down -7.6% like last month. But guess what, it is still down -6.8%! and as far as I can see when you go all back, it’s real hard to find any negative number. Never mind down -6.8%.

This is the problem. There are people like myself that are gainfully employed that are making and saving money. But there are also a lot of other people that don’t have a job.

Like 28 million people.

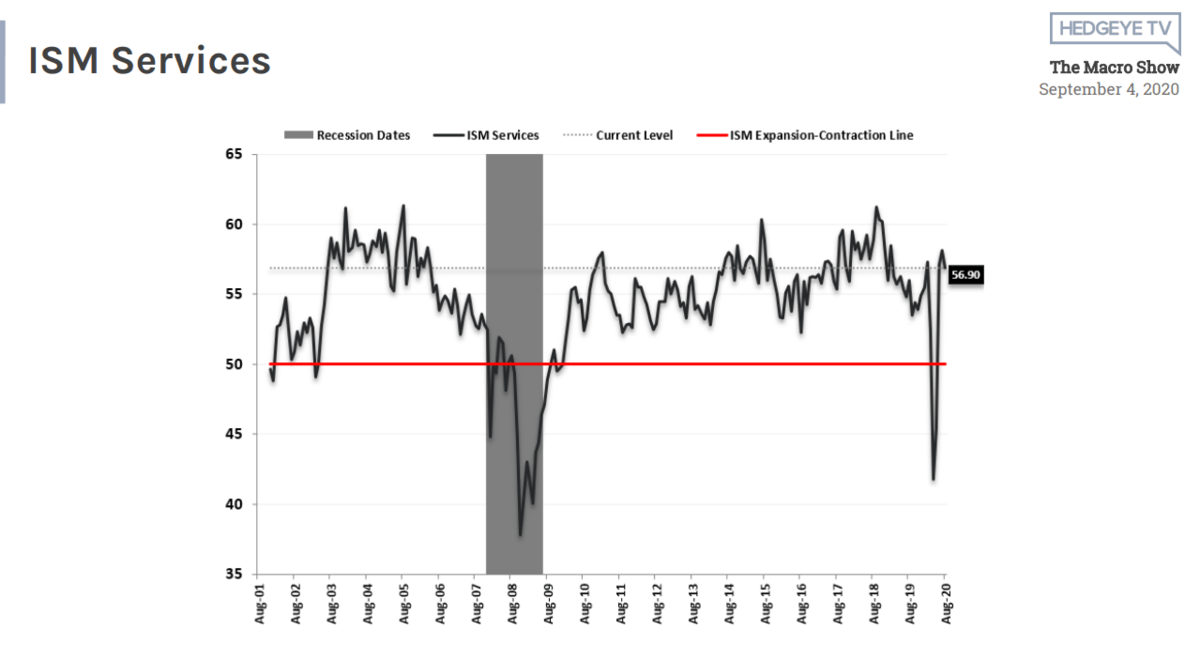

The unemployment rate whether they overstate it at 8.4% or 9%, it doesn’t matter. The big problem out there which we saw in the ISM Services number that ticked down in August, therefore signaling that it slowed in Rate of Change terms.

On top of that consumer confidence hit an almost Draconian lows of the cycle as well.

The consumer is not what you watch on TV with the cheerleaders and pom-poms from CNBC. It’s just noise and at the end of the day we have a major unemployment problem.

So anything you are modeling as a “V-Shaped” recovery is a “W” at best, and with the dollar up a little bit this morning I’d short it.

Don’t forget that I’m the one who told you to cover your dollar shorts not too long ago. That was a big reason to take down your gross exposure at the portfolio level.