This guest commentary was written by Mike Shell. It was originally published on ASYMMETRY® Observations on 8/6/20.

I pay more attention to macroeconomic trends when we are in a recession.

Though my tactical investment decisions are driven by the direction of price trends, momentum, sentiment, and volatility, it’s useful to take a moment to see what in the world is going on.

Clearly, employment and payrolls seem to be one of the main macroeconomic risks right now.

The July ADP employment report showed private employment increased by 167,000, far less than the expectations of the street of 1.2 million. It’s a big disappointment.

Today, we see the US Continuing Claims for Unemployment Insurance is at a current level of 16.11 million, down from 16.95 million last week, which is a change of -4.98% from last week and -35% from the peak in May.

For a long term perspective, here is US Continuing Claims for Unemployment Insurance going back to 1967, the past 53 years. It averaged 2.8 million over the period, reached 10 times higher than average, and is still 5 times higher than the long term average.

Of course, the average over 53 years doesn’t mean much when such an outlier is present, but maybe it helps put the trend into perspective.

Prior to now, the highest continuing claims for unemployment insurance from the Department of Labor was 6.6 million. That’s 10 million less than now. So, for perspective, todays level is nearly three times what it was at the peak in 2009. Said another way, the worst claims for unemployment insurance in 2009 was only 1/3 of today.

But hey, today’s 16.1 million is better than the peak at 25 million just a few months ago.

By the way, that 25 million was more than four times the highest level it reached in 2009.

So yeah, employment is an issue that certainly has my attention as a macroeconomic trend guy.

Next up is US Initial Claims for Unemployment Insurance. US Initial Jobless Claims, as tracked and reported by the US Department of Labor, provides data on how many new people have filed for unemployment benefits in the previous week. It allows us to gauge economic conditions in regard to employment.

As more new people file for unemployment benefits, fewer people in the economy have jobs. Of course, initial jobless claims tended to peak at the end of recessionary periods such as the last cycle peak on March 21, 2009 when it reached 661,000 new filings.

US Initial Claims for Unemployment Insurance is at a current level of 1.186 million, which is nearly double the 2009 peak, but it’s -83% below the stunning March 2020 high of 6.8 million.

I know I just shared some of these numbers a few days ago, but these are updated data this morning.

The next big issue I think we’ll see comes tomorrow. If tomorrows payroll numbers are similar to these ADP numbers, the job growth will be way below Wall Street expectations of 1.5 million.

We’ll see how it unfolds in the morning.

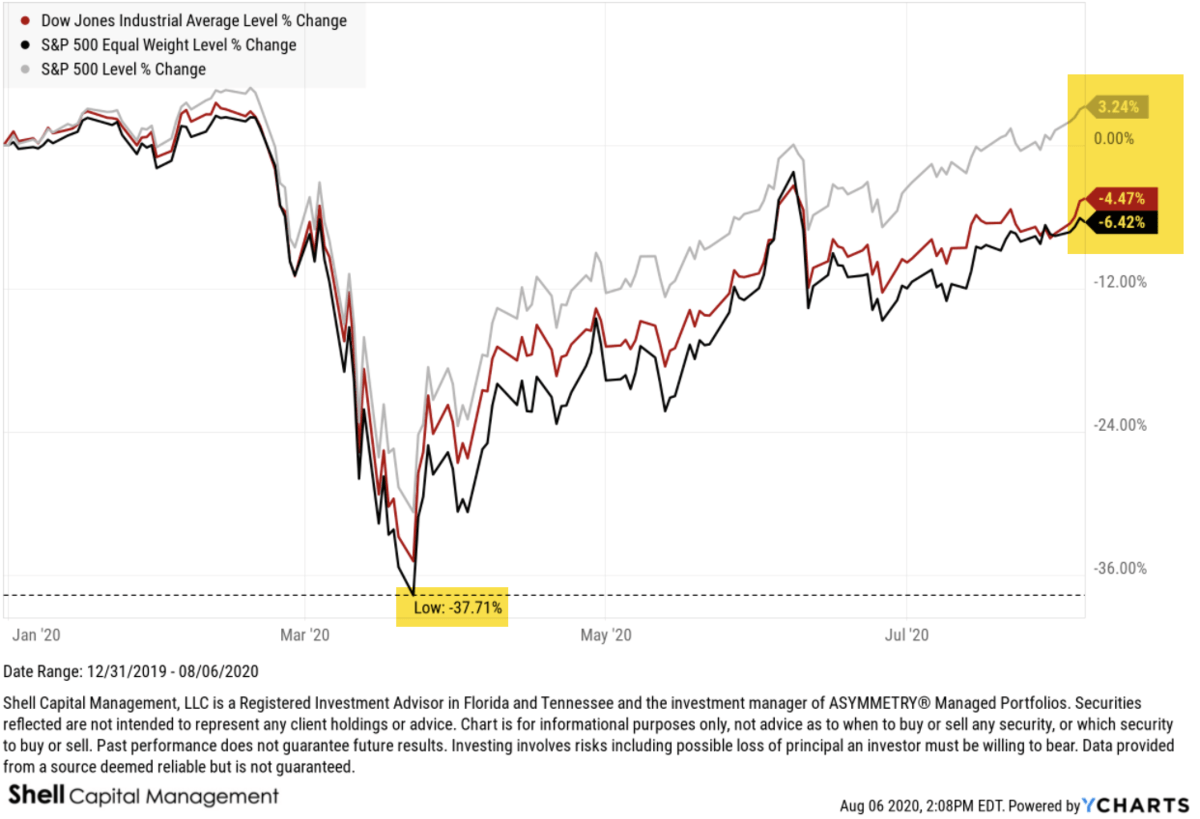

In the meantime, the resiliency of US stock market has been remarkable. Though anyone paying attention knows the driver is the US government intervention, the S&P 500 has now recovered from its -34% loss in March.

The Dow Jones Industrial Average remains about -5% from the February peak.

The equal weight S&P 500, which gives far more weighting to the smaller and mid size stocks, is about -6.4% from its prior high.

To the layman, it would seem the stock market has all but recovered.

If we didn’t know better, the bear market is over.

Do we know better? Or is it over?

Will 2020 goes down as the sharpest decline in modern history and the fastest recovery?

We’ll see.

But, over the long run, the stock market is driven by fundamentals. The challenge with fundaments like earnings growth, dividend yield, and the price-to-earnings multiple (optimism) they trade at.

Here is a chart of the rate of change of the S&P 500 price trend normalized with the Shiller S&P 500 CAPE Ratio, which is a measure of valuation. I’ve pointed out many times the valuation level was extremely high, though it has been since 2013. Look when it peaked in the relative chart compared to the SPX at the start of 2018.

What’s happened since then?

Swings.

Massive swings.

And sharp sudden drawdowns.

While the S&P 500 Shiller CAPE Ratio is now down to about 30, which is -10% below where it was at the start of 2018, the valuation level is still as high as it was before the Great Depression.

The markets are going to swing up and down and motivate a lot of mistakes along the way, but if history is a guide, we may be in for a much longer bear market and recession than is currently reflected.

You can probably see why my investment strategy is unconstrained, so I can go anywhere, including cash and treasuries, and apply different tactics for tactical decisions in pursuit of asymmetric risk/reward.

It’s never perfect, but I just keep doing what I do.

In hindsight, I’ve been underinvested in stocks the past few weeks, but we’ll see how it plays out from here.

ABOUT MIKE SHELL

Mike Shell is the founder of Shell Capital Management, LLC and the portfolio manager of ASYMMETRY® Global Tactical and ASYMMETRY® Managed Portfolios.

This piece does not necessarily reflect the opinion of Hedgeye.