|

Editor's Note: Below is a complimentary institutional research note written by Communications analyst Andrew Freedman on 8/5/20. To access further research please email sales@hedgeye.com. |

OVERVIEW

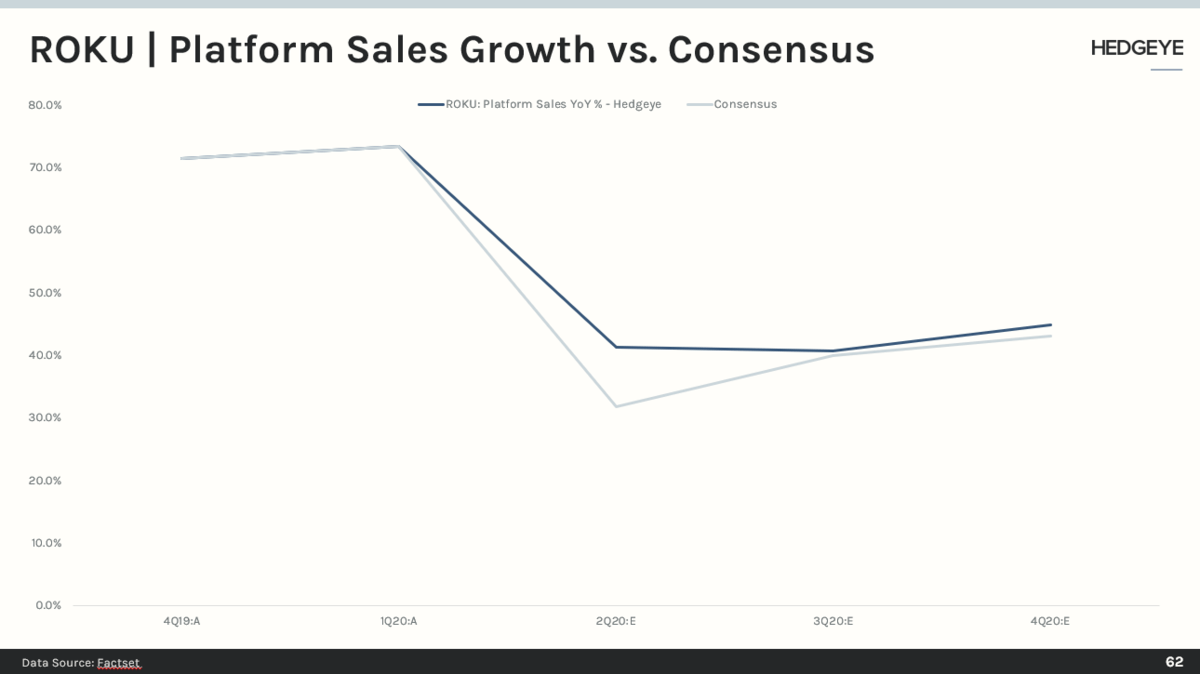

Roku (ROKU) is scheduled to report earnings after-the-close. We are modeling consolidated revenue of $330M versus consensus of $318M, with upside driven mostly by the platform business on faster recovery in video advertising (~35% of platform revenue*). Our assumptions are based on our channel checks and programmatic advertising update from Pixalate (see charts below).

We hosted a call with a former head of advertising at Roku, in June 2020, who said growth returned to 75% of pre-COVID levels in June. We also spoke with an ad agency, who said their spending on Roku only increased during the pandemic as engagement accelerated. Overall, COVID accelerated the shift of linear TV advertising to CTV and programmatic channels.

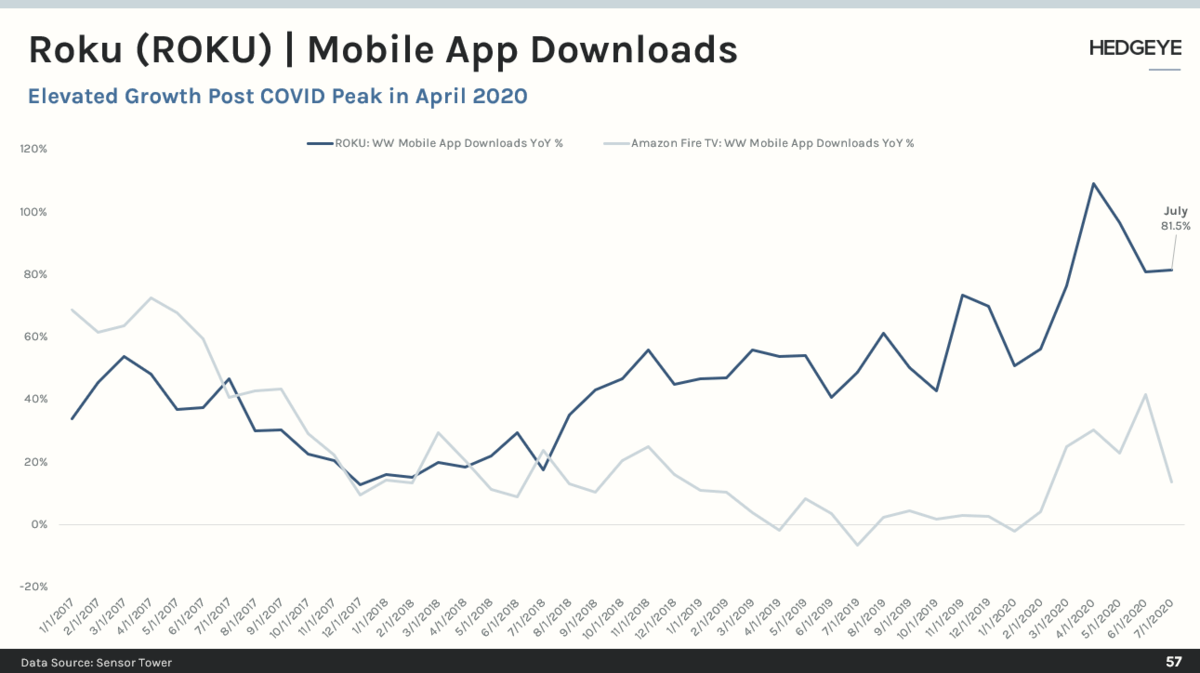

While we see upside to Q2 estimates, we believe the recovery pace will moderate in Q3 compared to Q2 due to 1) slower back-to-school season (which impacts advertising, but also device sales) and 2) higher churn from HBO now subscribers due to no HBO Max distribution agreement. That said, mobile app download growth continues to be robust (even post-COVID), which we believe is a positive indicator of account growth and engagement.

The stock has had a great run in the past couple of months and is currently trading at the high-end of its historical valuation range. However, we still believe estimates are too low and see upside to $200-$300 over the next 12-24 months as the recovery takes hold and Roku captures a greater share of the incremental TV advertising dollar.

*Hedgeye estimate

other nuggets

- From TTD: "Through the first 20 days in April, we estimated connected TV spend on our platform increased by about 20% YoY. Over the last 10 days in April, connected TV spend accelerated even more. During that period, we estimated that connected TV spend increased by about 40%."

- From FOXA: "Tubi has seen phenomenal growth it joined Fox. In June, it surpassed 200 million hours streamed per month, representing more than 100% growth YoY. During the fourth quarter, several Fox hit shows were added to Tubi, with The Masked Singer quickly becoming Tubi's #1 streamed series."

- We would remind investors of Roku's initial guidance for 2020 (since withdrawn), which called for revenue of $1,580 - $1,620M in 2020. Consensus is now at $1,511M. We would note that Q1 guidance initially called for $300 - $310M in revenue, Q1 pre-announced $307 - $317M in early April, with actual Q1 results coming in at $321M. We bring this up because, despite the negative impact of COVID in late March, Q1 reported results still came in above their guidance pre-COVID. We believe this bodes well for Q2 results and beyond relative to current consensus estimates.

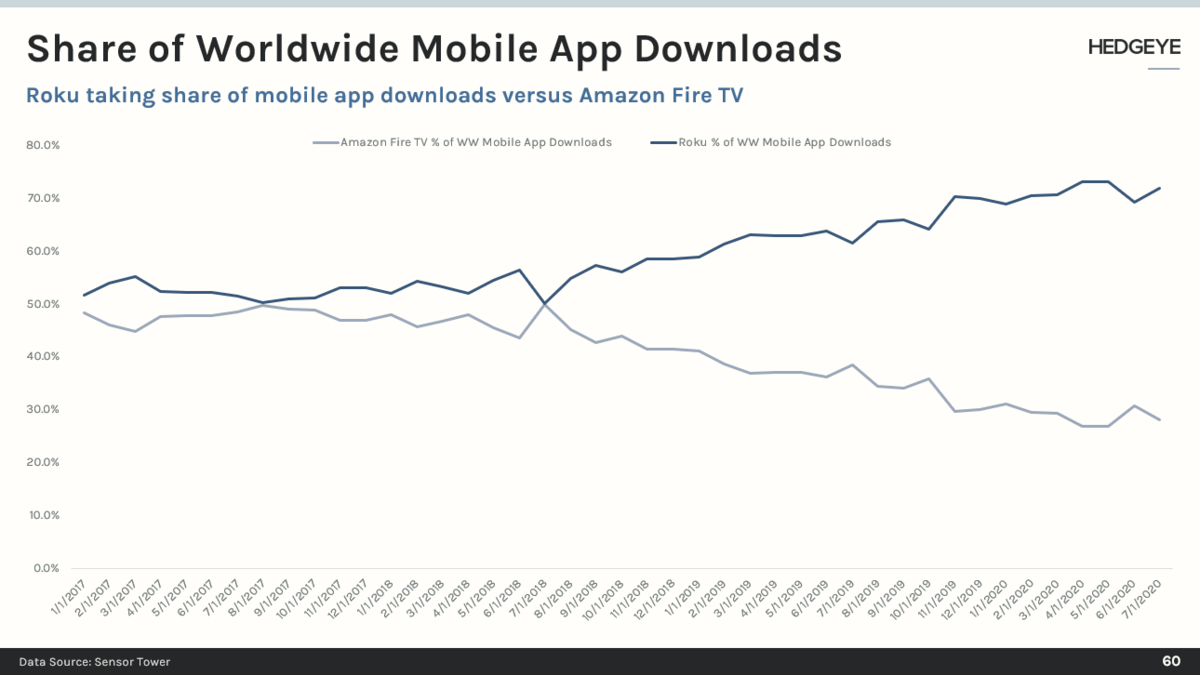

key charts

To access further research please email sales@hedgeye.com.