Following UA’s 2Q call, we see two key incremental opportunities for top-line growth – outlet stores & distribution within existing partners. Below is our analysis sizing each:

One of the two incremental growth opportunities pertains to direct-to-consumer. Sales in this segment are tracking up 60%+ with growth of 17-19 stores on a base of 35 in 2010. Plans call for similar unit growth in 2011. In an effort to size the potential contribution to the top-line consider the following. Taking into account location at premium outlets where productivity is typically $600/sq. ft and an average store size of 5,000 sq. ft. with year-1 productivity at ~75%, we estimate the addition of ~18 stores in each of the next 2-years alone could add $40-$50mm, or 4%-5% annually.

Additionally, growth within existing partners such as Foot Locker also represents meaningful upside over the intermediate-to-long term. For example at Foot Locker, UA can grow through 1) increased door distribution and 2) increased product penetration (i.e. apparel and footwear):

1) We know that UA is in 700-800 of approximately 2,400 addressable FL stores (excluding ~750 international locations and ~465 Lady Foot Locker concepts – these represent an additional opportunity a few years out). If we assume that each store sells 1 pair of UA shoes/day with a net retail ASP of $70 and retailer margin of 55% (essentially $45 at wholesale), that equates to ~$13mm in footwear revs for UA at FL currently, which we view as conservative. Therefore, the expansion into 1,600 incremental stores represents a ~$26mm opportunity.

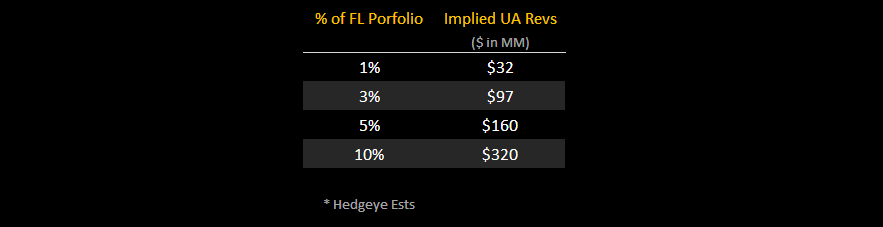

2) The more meaningful opportunity is increasing UA’s market share within FL’s mix. If we take into account the fact that Nike represents 60%+ of FL’s portfolio and no other brand accounts for more than 10%, let’s assume that UA represents only 1%, or ~$50mm of sales at retail. Again, this equates to ~$32mm to UA at wholesale (same retail/wholesale markup assumptions as above). With basketball shoes and gen-2 running shoes imminent, we fully expect UA to become more meaningful to FL’s portfolio. The table below captures just how significant an opportunity this is for UA. As a reminder, UA is currently a $1Bn business.

It’s clear that we should no longer expect major product launches from the company following its $5mm Super Bowl footwear launch in 2008. There are clearly new products on the near-term horizon in both footwear (basketball and running) and apparel (cotton-based and new fits) that will play a key role in driving double digit top-line growth. Coupled with the aforementioned distribution opportunities, we expect 20% top-line growth over the next 2-years, at least, and remain comfortably above guidance and the Street at $1.19 in 2010 and $1.75 in 2011.