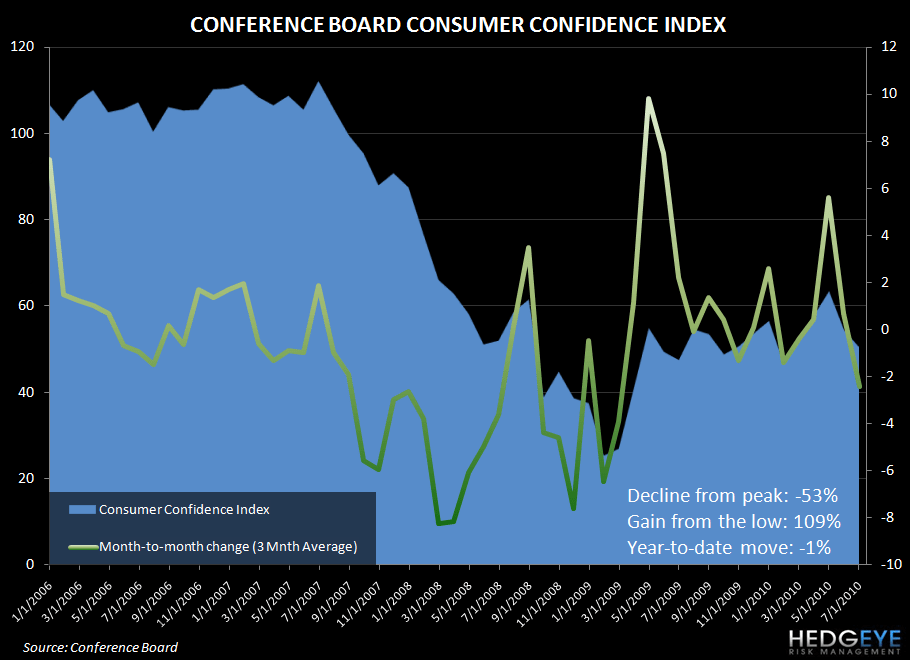

Once again we are seeing a major plunge in Consumer Confidence, which came at 50.4, below expectations of 51.0, and down 7.1% from a revised (upward) prior reading of 54.3 (previously 52.9). The Present Situation Index decreased to 26.1 from 26.8 and the Expectations Index declined to 66.6 from 72.7 last month.

Consumer attitudes are also being expressed in current sales trends. According to Johnson Redbook, U.S. same store sales fell 0.7% month-to-date for the week ending July 24 (compared to the previous month); the seventh consecutive weekly decline in sales.

Today’s confidence reading is more indicative of where we are heading than today’s Case/Shiller data.

As expected, home prices rose predictably in May and will rise again in June before heading lower in 2H10. As our Financials analyst Josh Steiner noted in his Housing Black Book, May prices reflect March contract activity which was strong due to the April tax credit expiration.

Pick your poison as to why you think confidence is going down, but I’m now focused on the incompetence of the people in Washington. Washington is the epicenter of everything consumer - unemployment benefits, policies that enable job growth and a federal reserve that won’t pay the aging population an interest rate on its savings accounts. The issues in Washington are impacting the whole country and individual states are also beginning to make significant cutbacks.

Nothing is getting done.

The precipitous drop in confidence in Washington among the electorate has been shaped largely by the harsh economic reality facing many consumers today. The approval rating of the president among 18-34 year olds is but one example. Among 18-34 year olds polled by Quinnipiac University in November 2008, 73% viewed Obama favorably. Last week, a poll conducted by Quinnipiac University revealed that only 46% of 18-34 year olds viewed Obama favorably (with 42% holding an unfavorable opinion). Additionally, 37% of the same demographic would vote for a generic Republican in a presidential election versus 34% for Obama. No age group has a tougher time finding a job at the moment than teenagers and young adults in their twenties. In turn this is putting incremental pressure on their parents….. A vicious cycle for sure!

The earnings season is been strong and as expected the corporate story telling is alive and well. We are setting up for what could be a very interesting 3Q10 preannouncement season…

Howard Penney

Managing Director