This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

This week The Institutional Risk Analyst reaffirms our negative view of The Goldman Sachs Group (GS). The securities firm with a small bank attached had a record quarter in Q2 2020 thanks to great performance by the global markets team.

But a week later, the GS investment bankers promptly puked out the profit for the first half of the year to partially settle criminal and civil claims arising from the 1MDB fraud in Malaysia.

And BTW, anyone with information as to the whereabouts of the fugitive Jho Low, the Malaysian businessman and international fugitive sought by the authorities in Malaysia, Singapore, the United States, to name only three jurisdictions, do drop us a note. Not only did Low fool the folks at Goldman Sachs, including former CEO Lloyd Blankfein, but he also managed to swindle a whole lot of US financial moguls and Hollywood types including Leonardo DiCaprio in the process.

Of course, in a purely existential sense, we could attribute the frequent financial shenanigans seen in the Asian financial markets to the vast sea of fiat paper dollars being emitted by the US Treasury.

Not only does the world of offshore dollars provide big opportunities for global banks, investors and rating agencies, to name but a few, but it also produces some of the most remarkable frauds and scams seen in modern times.

The arbitrage between the dollar world and the two other major currency alternatives, the Japanese yen and euro, is one of the key factors affecting US monetary policy in a global sense. As we’ve discussed frequently with our friend Ralph Delguidice of Pavilion Global Markets, the interplay of offshore spreads is a key part of understanding the global demand for dollars.

Most recently, though, we have seen the US Treasury amass a vast pile of cash in the wake of the fiasco in March, when most markets essentially stopped functioning for two weeks.

The Fed is supposed to be the guardian of the Treasury's market access, after all. The Fed then compounded the problem by initiating a massive open market program in April (not “QE,” you understand) that nearly caused the failure of several small banks, REITs and hedge funds.

Understanding the interplay between the Treasury General Account (TGA) and the Fed’s now $7 trillion balance sheet is essential. The TGA is the proverbial dog and the federal Reserve System is the tail.

In a note appropriately entitled “Carry On; Zero is Coming,” Ralph wrote last week about the monetary impact of the TGA:

|

”The key takeaway here now becomes clear. If a 25% contraction in system-wide reserves was insufficient to raise USD funding costs in any of the money markets used to provide leverage to buyers of US assets, what is the likely impact of a huge reversal in these liquidity flows when the Treasury spends down the account? Funds will flow back into a global USD market still saturated with cheap funding, and carry trades will become that much more attractive to foreign buyers as hedge costs fall and even go negative.” |

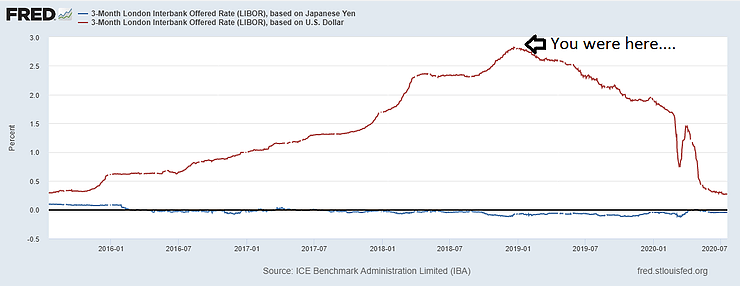

That’s right, in the not too distant future, the cost of hedging dollar assets could swing negative, something that will complete the cycle from the end of QE in 2015 and the peak of US interest rates in early 2019. Remember when the Federal Open Market Committee actually thought that they could raise interest rates even further in 2019? Three-month LIBOR never even made it to 3% in that strange period, as shown in the chart below.

Students of the foreign exchange markets understand that the weight of public sector debt is acting like a 100 kg kettle bell tied around the neck of the global economy.

We already had a debt problem before COVID19. But now, with much of the world economy idled or in shock, or both, and asset prices falling accordingly, the prospects for widespread global deflation are greater than ever before.

And the global central banks seem powerless to prevent this long-avoided endgame.

Even as interest rates in the US fall under the weight of shifts in the TGA balances, the dollar continues to strengthen, the opposite situation to that faced by most other nations. This strange circumstance allows the Fed to monetize most of the interest cost of the Treasury’s debt issuance and deficits, one big reason why people in Washington think that deficits don’t matter – at least this week.

Next will come the creation of new fiat dollars to offset interest and principal expense for the Treasury. Are you horrified by this suggestion? Think this can't happen?? Tell us the last time an official of the Federal Reserve or Treasury publicly rebuked Congress for the absurd conduct of fiscal policy.

The fact of global deflation makes it seem like negative interest rates and even stranger ideas like modern monetary theory or “MMT” are feasible. But in fact, the artificial environment that allows the Treasury to issue trillions in debt and the Fed to purchase most of it comes from the “special role” of the dollar dating back to WWII.

The dollar monopoly on global payments and as a unit of account allows Americans to pretend that black is white or that negative interest rates are somehow the cure for deflation. What is MMT but an acknowledgement of another terrible disease, namely war?

As the victor post WWII, the US became the "global reserve currency" by default. The job found us. And we'll enjoy the dubious benefits until we don't. Then the MMT illusion vanishes along with negative interest rates and the pretense of the low inflation.

But for now, the rules of dollar global finance apply to all nations -- except the United States. Just as the Federal Reserve System is the accounting antithesis of the Treasury, the dollar is the global long position and the holders and issuers of debt in all other currencies are, by definition, short dollars. When economists suggest that the US should embrace negative interest rates, they betray a fundamental misunderstanding of America's position in the global markets.

“The Austrian theory of interest, as elaborated in Böhm-Bawerk’s hefty three-volume Capital and Interest, holds that interest emerges from the time preference of individuals—the willingness to pay more to have something now rather than later,” writes Edward Chancellor in The New York Review of Books. “Given that people prefer instant to deferred gratification—as the saying goes, a bird in the hand is worth two in the bush—time preference, and hence interest, must always be positive.”

Sadly, the widespread idiocy that suggests that expedients such as negative interest rates or MMT are a solution for global deflation, our collective woe, misses the point.

It is the dead weight of burgeoning global debt and falling cash flows from assets that is the root cause of deflation.

Try as they might, the Fed and other global central banks cannot avoid forever the eventual reset in asset prices to match reduced cash flows. Right on time, COVID19 has arrived almost a century since the emergence of the Spanish flu in 1918, setting the stage for the deflation of the 1920s and the economic collapse of the 1930s.

We think observers should be more attentive to the historic parallels of the centennial of the Spanish flu pandemic and the deflation of the 1920s. Professors Stephen G. Cecchetti of Brandeis University and Kermit L. Schoenholtz of NYU Stern, writing in The International Economy, put the future situation in concise terms:

|

“The value of cruise ships, airplanes, trains, retail space, office buildings, dormitories and the like has almost surely collapsed. Meanwhile, the value of other productive capital, such as high speed internet connections, has risen, but these investments appear to be far less costly to undertake. So, on average, the observed return on investment is likely to decline for some time.” |

The good news is that the deflation in the real value of asset prices for assets like cruise ships, airplanes and malls has already occurred.

The bad news is that the current value of these assets has yet to be adjusted.

Over the next several months and years, we expect to see significant losses emerging as the inexorable process of price discovery and resolution catches up with the nonsense that passes for serious thinking in Washington.

We wonder if @JoeBiden and his handlers understand that it is 1920 all over again. That we will have years more of COVID and, at the end, we'll see an end to the "special" role of the dollar. Then things like QE and MMT will fade into memory as we embrace the reality of no longer being special.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.