A few noteworthy read-throughs on the consumer as we kick off earnings.

We’re getting an early look into the strength of consumer spending here today with results out of both Hanesbrands and VF Corp.. Perhaps the most noteworthy trend here are the results themselves with each company both beating expectations by a healthy margin and raising full-year guidance. While we’re not going to rehash all of the details of the calls here, there are several noteworthy read-throughs to consider as it relates to consumer spending:

- Both companies exceeded top-line expectations suggesting that spending remained strong through June with broad-based results reflecting positive growth across product categories, distribution channels, and end markets. However, in speaking to trends since the quarter the view is decidedly more mixed with evidence of softness underway according to VFC this morning while HBI continues to see an overall increase in consumer spending. One of the areas of weakness highlighted by VF in particular was premium denim, which has deteriorated even further over the last 8-weeks.

- While shelf-share gains accounted for 6% of HBI’s 9% top-line growth, the balance was driven by increased sell-throughs at retail. Among the reason’s management cited for raising guidance was both higher productivity of its new programs than expected as well as an continued increase in overall consumer spending. Yes, replacing one’s underwear is less discretionary than some might like to admit, but the reality is that this is not simply a basics business – quite the opposite actually.

- All of HBI’s top brands (i.e. Champion, Just My Size, and Hanes) drove the outperformance in Outerwear segment (+16%) with particular strength in the new plus-size initiative Just My Size that’s sold through at Wal-Mart. Following better than expected sell into at the mass retailer over the last two years, this line continues to outperform. Granted the majority of growth here is coming from share gains, but Wal-Mart is obviously seeing healthy demand for the for product.

- Cost inflation remains at the forefront of retailer concerns with the offset coming in the form of higher prices at retail. Interestingly, it appears that the channel with greatest price flexibility is at the mass channel. While pricing is going through across the board at HBI, VF noted that its sees the opportunity for continued pricing in its Lee and Ryder product, which is sold solely in the mass channel.

- Lastly from a meteorological perspective, VF cited unseasonably warm weather over the last two months as a headwind for denim sales – no doubt. Challenging the obvious, The North Face best known for its winter jackets continues to post strong results.

Casey Flavin

Director

LEVINE’S LOW DOWN

- Add Brooks Brothers to the list of brands translating their adult fashions into kids. The company is testing two kids stores, one in Westport, CT and the other in Kansas City. The stores are called “Fleece”. With Crewcuts, Abercrombie, Ralph Lauren, AE ’77, and PS by Aeropostale all carrying an Americana aesthetic we wonder if this niche might be becoming overstored in a hurry.

- Rumors are swirling on Madison Avenue that Chanel is about embark on price increases for the company’s classic (iconic) handbags. The word on the Street is that prices are set to increase by 20% on August 1st. Now that’s serious inflation for a product that remains unchanged but cost about 40% less only two years ago.

- Add a little fashion to what is otherwise a stable, but boring category, and you end up with Diaper Wars. After Kimberly Clark announced it sold 2 mm denim-printed diapers so far this summer, Procter and Gamble has responded with a fashionable item of its own. P&G and Target have joined up for an exclusive line of diapers with 11 styles designed by Cynthia Rowley. By the way, 60% of Mom’s purchase denim for their infant before the age of 6 months. As Fall approaches we wonder if a corduroy version of Huggies is on the horizon.

MORNING NEWS

House Passes Miscellaneous Tariff Bill To Reinstate Expired Import Duty Breaks - Yarn spinners, fabric firms, footwear brands and retailers have been paying tens of thousands of dollars in duties on imported components since Jan. 1 because Congress let legislation expire that suspended tariffs on hundreds of imported products. Over the past seven months, companies have had to drop product lines, increase prices and find substitutes, all at a cost to the bottom line. On the plus side, the bill includes a retroactive provision that will provide full or partial refunds to companies on duties paid on all covered products since January. On the downside, the measure would increase duties on several hiking-boot and shoe imports because trade has grown significantly. <wwd.com/business-news>

Hedgeye Retail’s Take: Geared mostly towards a sundry of goods like basketballs, ski boots, and fishing waders, the duties re-imposed by the bill were estimated in the tens of millions of USD per year so a nice benefit to outdoor players, but not a game-changer per se.

Study Shows Toning Shoe Is A Myth - The American Council on Exercise (ACE), the organization that certifies fitness professionals, released what it believes is the first independent study on toning shoes. Results showed no evidence to suggest that the shoes help wearers exercise more intensely, burn more calories or improve muscle strength and tone. The study enlisted a team of researchers from the Exercise and Health Program at the University of Wisconsin, La Crosse. In particular, it explored the effectiveness of popular toning shoes including Skechers Shape-Ups, MBT (Masai Barefoot Technology) and Reebok EasyTone. ACE's Chief Science Officer Cedric X. Bryant, Ph.D stated, "Unfortunately, these shoes do not deliver the fitness or muscle toning benefits they claim. Our findings demonstrate that toning shoes are not the magic solution consumers were hoping they would be, and simply do not offer any benefits that people cannot reap through walking, running or exercising in traditional athletic shoes." <sportsonesource.com>

Hedgeye Retail’s Take: While we’re surprised it’s taken this long for an independent study to come out on the merits of toning shoes, were not surprised in the result…and don’t expect consumers will be either.

Luxury Spending Is On The Rise, But Apparel Isn’t Feeling The Love - The country’s richest consumers will drive luxury spending up between 6% and 8% this year, according to a survey of affluent Americans conducted by American Express Publishing Corp. and Harrison Group, but apparel is unlikely to benefit. Apparel spending by these consumers has recovered somewhat, but continues to slide, falling 5% in the first quarter and 4% in the second quarter. By comparison, apparel spending by this group slid 8% during the fourth quarter of 2008 and 9% in the first quarter of last year. <wwd.com/business-news>

Hedgeye Retail’s Take: Why buy something new when you can just pull the tag off something in your closet that has yet to be worn? We suspect a bit of over-supply in the wealthiest consumer’s closets is likely the culprit for share gains by more durable items (i.e. shoes, bags, and home furnishings).

SGMA Study: Nearly 80% of Americans Participate in a Sport, Fitness, or Outdoor Activity - While more than 50% of all Americans are considered 'frequent' sports participants, 12% are classified as 'regular' sports participants and 15% are active on a 'casual' basis. Unfortunately, 23% of all Americans are not active at all -- according to the Sporting Goods Manufacturers Association's Sports Participation in America report (2010 edition). <sportsonesource.com>

Hedgeye Retail’s Take: Without this 20% sample the toning craze simply wouldn’t exist.

Wal-Mart May Open Hundreds of India Stores if Foreign Restrictions Lifted - Wal-Mart Stores Inc. may open hundreds of stores in India, the world’s second-most populous nation, should the government lift a ban on foreign direct investment in multi-brand retailers. <bloomberg.com/news>

Hedgeye Retail’s Take: As multi-nationals continue to beat on the door of this lucrative market and now Wal-Mart…we suspect the mounting pressure will force the government update its stance on foreign direct investment in the near-term.

The Buckle Hits Some Hard Times - Are the glory days of double-digit comparable-store gains a thing of the past for teen retailer The Buckle Inc.? Once the golden child of specialty retail, Buckle startled analysts earlier this month with a 7.3 percent drop in June comps, far worse than estimates ranging from a small gain to a low-single-digit drop. The company blamed the disappointing results on the economy and difficult compares. But, it appears that Buckle’s long-standing aversion to price promotion may have also played a role. <wwd.com/business-news>

Hedgeye Retail’s Take: While many in retail consider Abercrombie the last to adjust its pricing, which it did several quarters ago now, there’s still Buckle insisting on holding tight to price…and is falling fast in the process. It’s tough to help brands that can’t help themselves.

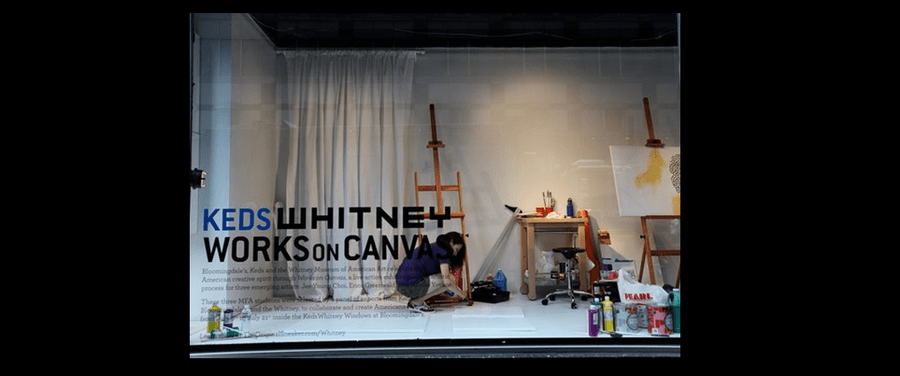

Ked's Exposure in Bloomingdale's - As part of Keds’ sponsorship of the Whitney Museum of American Art’s summer season, the brand installed a window at the Bloomingdale’s flagship store. Titled “Works on Canvas,” the installation — which closed last night — showcased shoes, a touch-screen mechanism for ordering customized kicks, and three art students in the windows making Americana-inspired art. Rubel said the initiative was a success by many measures. The window installation drew hundreds, while the blog for the event, at Theoriginalsneaker.com/whitney, attracted more than 10,000 unique page views. Keds also saw very high double-digit sell-throughs at Bloomingdale’s, as well as online at Keds.com, in the two-week period that the windows were up, according to Rubel. <wwd.com/footwear-news>

Hedgeye Retail’s Take: Rubel and his team continue to find creative ways to promote this brand including the company’s recent collaboration with GAP – all indications here are that the brand is growing once again.

JCP Showcases its New LIZ Line - With high expectations for market share and margin growth, J.C. Penney unveiled its exclusive Liz Claiborne collection on Wednesday. It’s an expanded version of its Liz & Co. line, which has been discontinued, but with comparable prices. Penney’s Claiborne collection launches next month in more than 1,100 stores and on jcpenney.com with 30 categories across men’s, women’s, accessories and home, which joins the assortment in January. The fall collection stays true to the Liz Claiborne image with a versatile sportswear array of novelty knits, nautical striped sweaters, classic denim in a variety of washes as well as outerwear ranging from a country buffalo plaid jacket to a chic fake fur urban version. Accessories run the gamut, including shiny handbags, while jewelry exudes plenty of sparkle and shine. <wwd.com/retail-news>

Hedgeye Retail’s Take: This is huge for LIZ. As we highlighted in a note out yesterday, August is a big month for the retailer in more ways than one.