A surprisingly good quarter out of PENN and solid guidance.

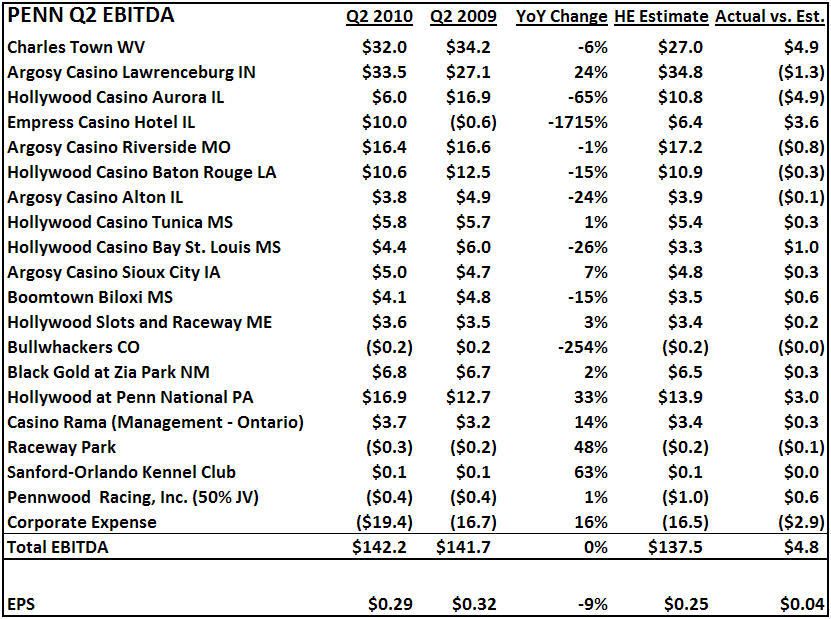

Once again, PENN did well on the cost side to offset the sluggish regional gaming trends. EBITDA of $142.2 million beat our estimate by almost $5 million, driven primarily by better than expected margins at the two big racinos: Charles Town and Hollywood at Penn National Raceway. PENN raised 2010 EBITDA guidance slightly from $578m to $580m, again a surprise given the top line trends.

EPS guidance is a little confusing as PENN includes non-recurring items, so it appears they are lowering guidance from $1.13 to $0.98. However, that is not the case. Q2 Adjusted EPS of $0.29 beat our $0.25, so we will likely be raising our full year Adjusted EPS estimate of $1.12 by $0.04, give or take a few pennies.

We’ll have more details later but if PENN can hit its guidance, the stock looks very cheap given the long-term growth associated with the high ROI projects in new markets, particularly Ohio. We think PENN can grow EPS at a 25% CAGR over the next 3-4 years.

The table below summarizes the property performance in Q2 relative to last year and our estimates.