Position: Long British Pound via FXB

Hungary is flashing a clear negative divergence across numerous metrics today on the heels of a bearish IMF statement over the weekend. Here is the set-up behind the numbers:

The IMF concluded in its review of Hungary’s $25 Billion emergency bailout that “a range of issues remain open” and that the country is not doing enough to slash spending or make long-term reforms to its economy. If you’ve followed Hungary this report comes as nothing new: the government has struggled over the last five years to manage its budget imbalances, forcing the IMF to take the lion’s share of a $25 Billion loan in Oct. 2008 (with the EU and World Bank contributing ~ $8.1 Billion and $1.3 Billion, respectively) to support Hungary’s outstanding debt.

While skeptics may conclude that Hungary has no intent to issue “real” fiscal reform, but rather will pander to whatever the IMF wants to see, we’ll wait until this Thursday, when the government meets to vote on its next economic plan, before concluding further. However, it’s worth noting that going into the vote Hungary’s ruling Fidesz party has municipal elections on October 3rd and loud protests against austerity measures in mind.

Market Sentiment

The Hungarian market reacted decidedly negatively to the IMF’s statements, with investors worried that the country could jeopardize its access to a €5.7 Billion IMF loan tranche earmarked for this year.

Here’s what the market said:

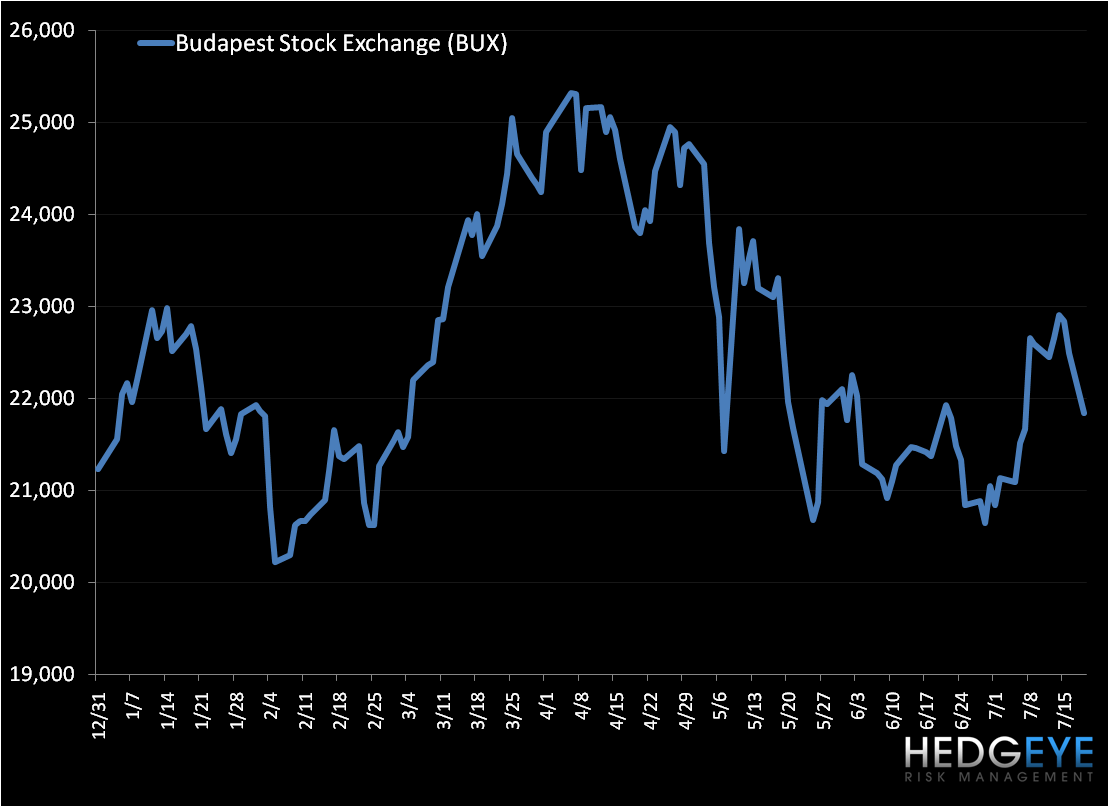

- Hungary’s equity market (BUX) fell -2.3% today (1st chart below). [You’ll note that our read-through on the European bank stress tests (which will be released this Friday) is that these banks (91 in total) are largely set up to NOT fail, yet should negative issues arise we’d expect the EU to write checks quickly to fund the gap.]

- The Hungarian Forint versus the EUR took a dive into the news (2nd chart below).

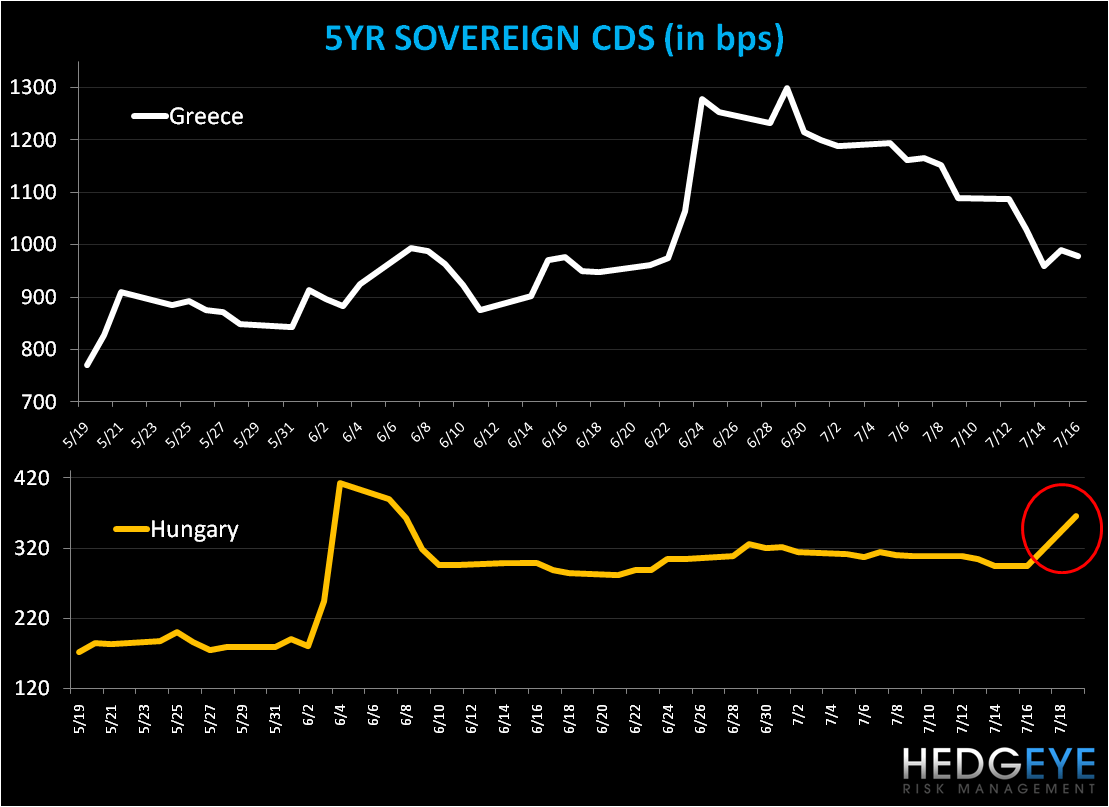

- The country’s sovereign CDS rose materially (3rd chart below).

Take-Away

One concern with a weakening Forint versus the EUR or Swiss Franc is that many loans extended in Hungary over the last five years were denominated in lower yielding Euros and Francs. Clearly a depreciating Forint increases risk of default as debtors are squeezed further with repayments.

The IMF also took issue with the country’s two-year levy on banks, aimed at raising over $900 Million, citing that “a significant negative impact on the country’s investment climate and economic growth.” Also, we note the worry for foreign banks in Hungary, in particular the Austrian lenders Raiffeisen and Erste, as relative loser under these parameters.

Hungary gets another chance to prove its fiscal discipline when the IMF meets again in September. Between now and then we could see an uptick in volatility in Hungary and related Western and Eastern European markets. Despite the Euro’s recent gain above $1.29, clearly Europe’s sovereign debt default fears are not in the rear-view window!

Matthew Hedrick

Analyst