I said this yesterday, and I will say it again today, until the consensus view begins to catch up with the weakening reality, reporting risk continues to be to the downside of expectations.

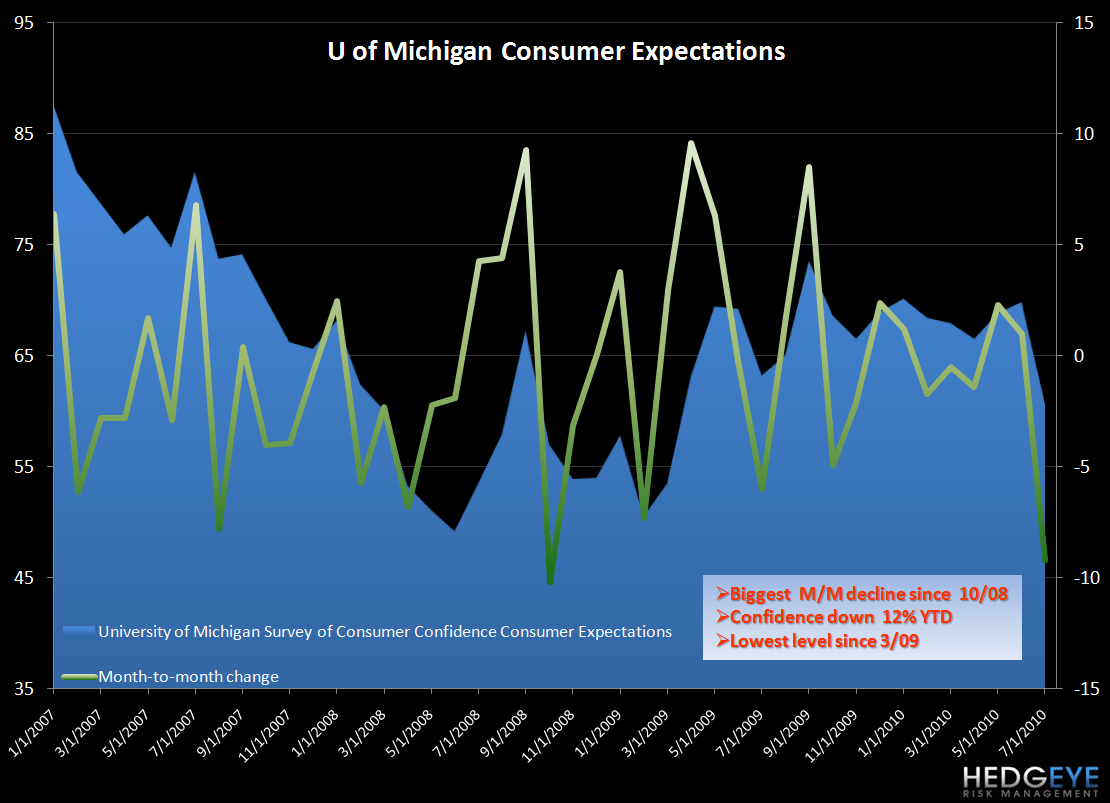

I understand why the market is selling off on this news, but who is actually surprised that confidence is declining?

- The economy and public deficits dominate as the nation's most important problems and there is little confidence in Washington’s ability to rectify either issue.

- We estimate discretionary spending to be down 2.8% in 2Q10 and 6.4% in 2H10.

- Initial jobless numbers improved of late, but the improvements are not significant enough to bring down the unemployment rate.

- Consumer demand has not bottomed - we are seeing this in a number of industries we cover at Hedgeye.

Today’s decline in confidence is a clearly not a one-time event. Two of our key themes in 3Q10 (Bear Market Macro and Housing headwinds) have only just begun to play out. Unfortunately, if our themes are right, the consumer will face a difficult time in 2H10.

Howard Penney

Managing Director