|

Below is a complimentary research note from our Gaming, Lodging, and Leisure (GLL) analysts Todd Jordan and Sean Jenkins. If you are an institutional investor interested in accessing our research email sales@hedgeye.com |

Welcome to another installment of our very own Hedgeye Consumer Travel Demand Survey.

Now that the country is well into its reopening process, we have had a number of weeks where industry data points have gone from depressionary to RoC positive, but now comes the harder part.

How does the domestic travel recovery sustain itself through the macro downside that is still to come and how does it manage through the lingering Covid-19 risks? We continue to be more confident in the leisure traveler’s path to recovery, but on the whole, our survey has failed to capture a consistent level of optimism for that traveler base.

Consumers continue to be more partial towards hotels & resorts, but judging by overall travel intent, it’s not a done deal that hotels will recover any quicker than vacation rentals, at least on the leisure side.

We hope this survey should provide an advanced read on how leisure consumers are thinking about their future travel plans. Whether it’s hotel/resort, vacation rental, or ocean cruise, the survey should provide some color on where consumers might gravitate towards as more health guidelines and restrictions are lifted.

After our first 14 weeks of running the survey, we would have expected a clearer direction from the data, either decidedly more positive or negative, but interestingly, we continue to see plenty of indecision among the average person.

consumer survey results

Methodology of Survey

Each week (now every other week), Hedgeye GLL will receive updated results from their consumer survey questions. Since the majority of GLL is centered around the theme of “travel,” we geared our survey to directly plug into the wants and desires of potential travelers on a 6-month forward basis. Our survey is strictly focused on the US consumer and aims to gauge changes in interest levels across time.

Latest Results Commentary

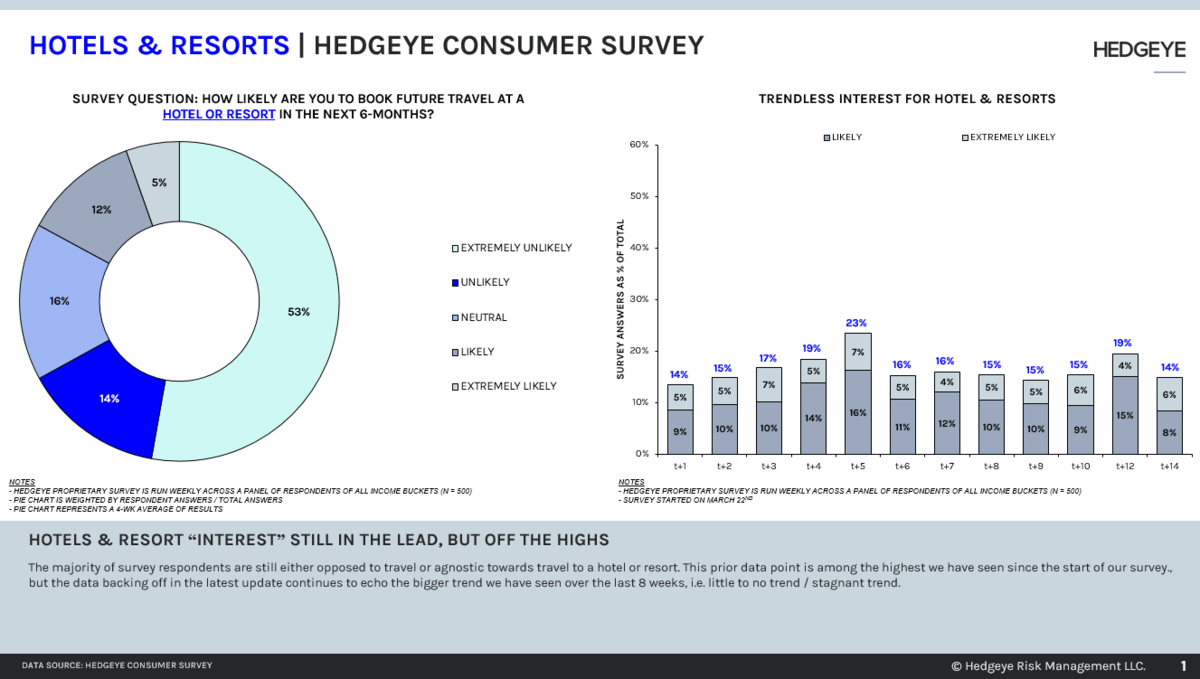

Hotels & Resorts

-

Back to base line for the hotels & resorts “likely” interest in the most recent update. The survey hasn’t breached its prior lows (positive) but continues to back off its highs (negative).

- The % of neutral responses actually ticked down vs two weeks ago, suggesting more negativity is building in the system – “unlikely” bucket readings were at their highest levels since 4 weeks ago.

-

Net/net, the survey spread between “likely” and “unlikely” for Hotels / Resorts was naturally less positive than it was last reading, and it’s back to the lows (more negative) of the survey time series. We care less about the levels and more about the RoC (as does the market), and this latest reading is definitely RoC negative.

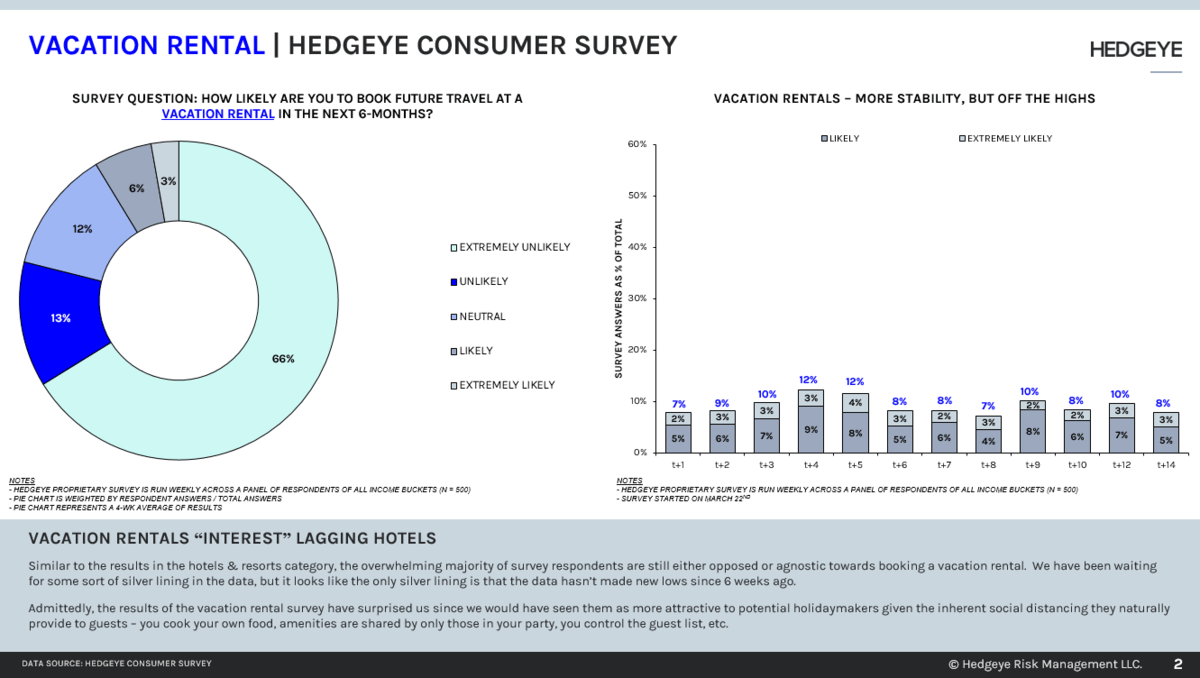

Vacation Rental

-

“Likely” buckets were down on the week, but not totally out of line with recent trends. Note, vacation rentals never really saw much of a spike since our survey started. Perhaps due to vacation rentals being less prevalent among US travelers.

-

Similar to Hotels, the neutral responses dropped this past week, and the “unlikely” buckets experienced a corresponding jump.

- Net/net, the spread between “unlikely” responses and “likely” skewed just close to as negative as they did on Week 8, when the survey hit its highs.

Ocean Cruise

-

Cruise lines continue to lag land based alternatives and the most recent datapoint was no exception – limited improvement since mid-April is what we’re seeing.

-

The % of neutral responses were lower this past week, so more interest, or lack thereof, flowed into the unlikely buckets.

-

Net/net, the survey for Ocean Cruise skews marginally more negative than it did 2 weeks ago, but not significantly worse than what we saw 4 weeks ago.

If you are an institutional investor interested in accessing our research email sales@hedgeye.com