This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

We have released the latest edition of The IRA Bank Book for Q2 2020. Suffice to say that our estimates for loan loss provisions in Q1 were reasonably close, but still understated the credit tsunami that is approaching US banks and bond investors.

To paraphrase the character King Willie in the 1990 Stephen Hopkins film “Predator 2,” Q2 2020 bank earnings will be "dread man, truly dread."

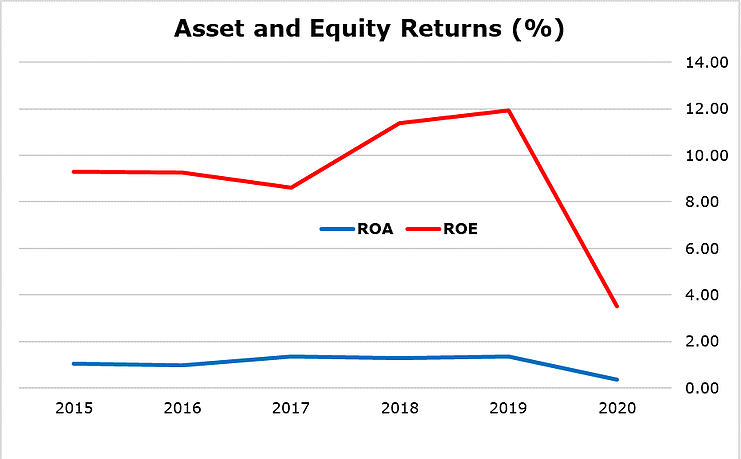

The chart below shows asset and equity returns for all US banks through Q1 2020. Take a guess where those two lines are headed in Q2.

First and foremost, we have a credit loss event coming at US banks and bond investors that is of indeterminate size but likely much larger than 2009. Second, we have market risk in the form of collateralized debt obligations (CLOs) and various other structured assets that, at the moment, have rebounded.

And third we have counterparty risk to a lot of nonbank funds, REITs and issuers that will be cut back in short order. But as you cut risk, you also cut revenue.

While the credit losses hurtling at US banks are bad enough, the liquidity assistance from the Federal Open Market Committee is increasing bank deposits and, thus, assets so rapidly that asset and equity returns are falling.

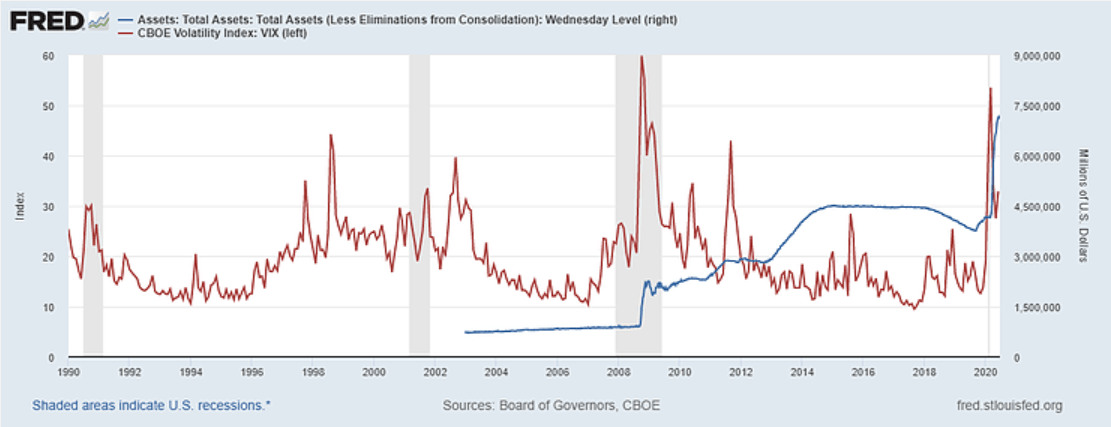

The system open market account (SOMA) is now north of $7 trillion or almost two times the portfolio expansion during QE-1-3, which ended in 2015.

Under the regime of Fed Chairman Jay Powell, we no longer refer to massive open market purchases of Treasury, agency and, yes, even private corporate bonds as “quantitative easing” or QE.

The Fed has not come up with a new moniker for this activity as of yet. We propose QE*, indicating an unknown quantity of intervention but also a factor closely related to Treasury debt issuance.

But by forcing liquidity into the system, the Powell FOMC now also has added trillions of dollars to the banking system. And this liquidity cannot be withdrawn.

For those that worry about future inflation in the age of QE*, ponder the fact that the Fed’s balance sheet is unlikely to fall much below current levels ever again -- at least so long as the Treasury is running massive fiscal deficits. The two agencies -- the Federal Reserve System and the US Treasury are inextricably tied together.

The truth of QE is that you cannot go back. Hopefully we learned this lesson in December 2018 and September 2019. The addition of liquidity and its impact on banks and investors, is permanent.

And this means that the FOMC must continue to buy and to thereby monetize trillions of dollars per year in US Treasury debt in order to ensure that liquidity does not run out of the market a la December 2018 and September 2019. QE forever. And future bank earnings will be depressed for years to come as a result.

Unfortunately, financial repression may be great for the US Treasury, but it is really bad for banks and private investors.

Yes, massive gushes of liquidity help to push up stock prices for a time, but how do you suppose markets will react when they discover that most or all of bank operating income in Q2 is going to be consumed by credit costs?

Even the inflationary impact of QE* may not be sufficient to float money-losing bank stocks.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.