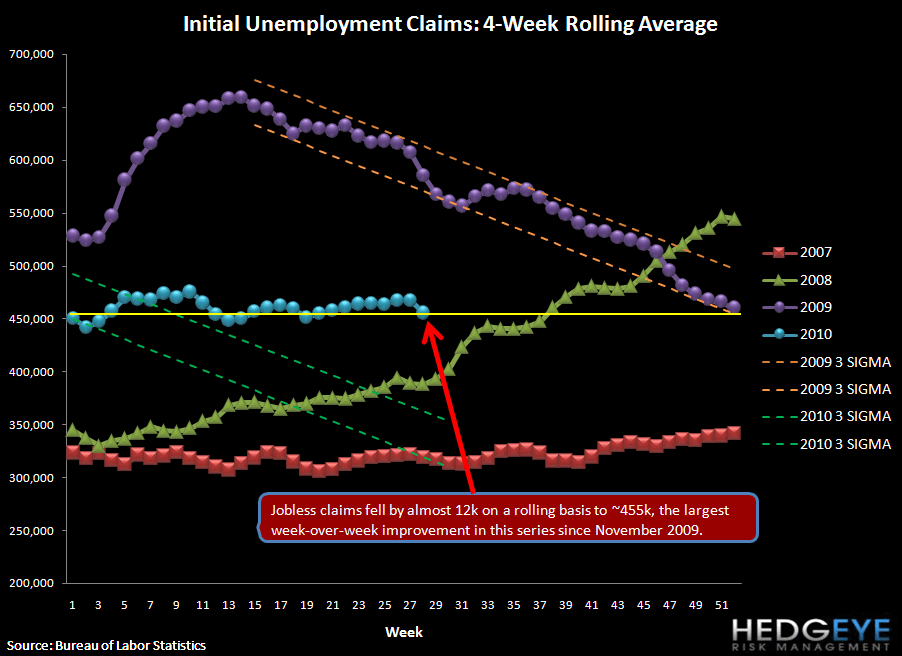

Initial claims fell 29k last week (25k net of the revision), the largest one-week improvement since February and the lowest absolute weekly number since mid-2008. Rolling claims fell almost 12k to 455k, the largest improvement since November of 2009. While the raw data has been volatile for the last five weeks (moving up or down more than 15k each week), until this week the rolling number had moved only slightly. This is undeniably a positive move. Initial claims are, however, still elevated at 455k (rolling), and we would have to see this rolling claims figure come down substantially into the 375-400k range before unemployment will meaningfully improve. We prefer a wait and see approach, but if the data continues to trend positively (better for two weeks in a row now) we will begin to change our tune as employment, along with housing, are the keystones of the economy.

Below the jobless claims charts, we show the correlations between initial claims and each of the 30 Financial Subsectors. To reiterate, Credit Card and Payment Processing companies show the strongest correlations to initial claims, with R-squared values of .62 and .72 over the last year, respectively. Surprisingly, some subsectors show a positive correlation coefficient to initial claims - i.e. Financials that go up as unemployment claims go up. These names are concentrated in the Pacific Northwest Banks and Construction Banks, though these correlations are usually not very high.

In the table below, we found the correlation and R-squared of each company with initial claims, then took the average for each subsector.

The following table shows the most highly correlated stocks (both positively and negatively correlated) with initial claims. Note that the top 15 negatively correlated stocks have a much stronger correlation on average than the top 15 positively correlated stocks - as you would expect, given that most of the Financial space is pro-cyclical.

Astute investors will note that in some cases the R-squared doesn't seem to reconcile with the square of the correlation coefficient. This is a result of finding the correlation and then averaging. For example, Pacific Northwest Banks have an average correlation coefficient of .32 and an average R-squared of .52 (with CACB, CTBK, FTBK, and STSA strongly positively correlated and UMPQ strongly negatively correlated). The different directions have the effect of canceling out each other out when finding the average correlation coefficient, but do not cancel out when finding the average R-squared.

As a reminder, May was the peak month of Census hiring, and it should now be a headwind to jobs from here as the Census winds down.

Joshua Steiner, CFA

Allison Kaptur