Since early 2008 we’ve singled out housing as the #1 macro driver of gaming revenues. An updated analysis shows housing and unemployment are even more critical now.

Sorry to bore you with statistics but I’m a bit of a nerd and it’s a big part of our process. Way back in early 2008, we regressed all important macro variables on gaming volumes and found that over the period from 1993 to 2007, housing was the most important driver, followed by GDP. It was an easy call then for us to be negative on gaming for most of 2008. Statistics do matter.

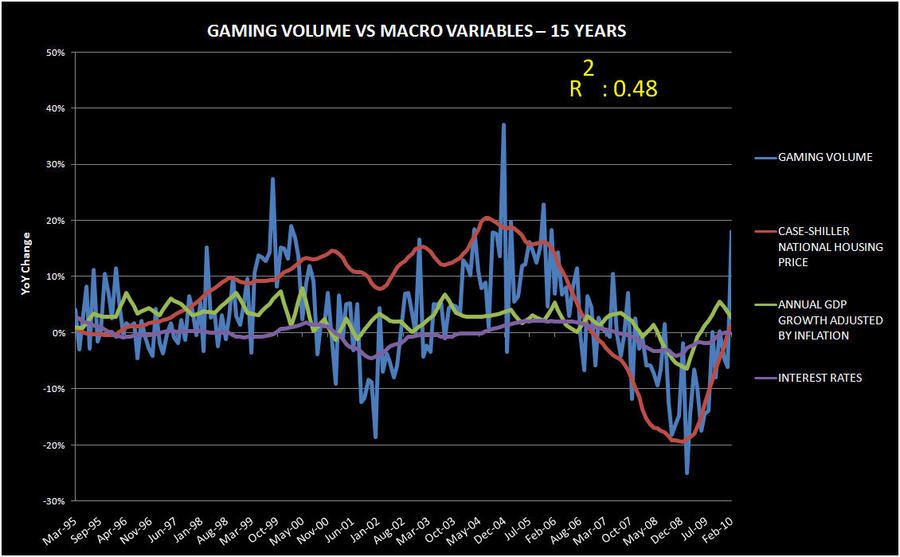

When we updated the regressions for Las Vegas Strip gaming volumes, we saw that correlations and R Squares have increased. Over the last 15 years, national housing prices, interest rates, and unemployment are the only three macro variables that mattered, and mattered in that order. T-stats are all close to or above 2. Surprisingly, GDP was an insignificant driver of Las Vegas Strip gaming volumes. Combined, these macro variables drove an R Square of 0.48.

The housing (wealth effect) and unemployment impacts are fairly obvious. The positive relationship between interest rates and gaming volumes may not be as intuitive to the casual observer. The average age of a LV visitor is 50 years old, and weighting age with gambling dollars would surely result in an even older demographic. Many of these gamblers live on fixed incomes so discretionary spending goes higher as interest rates move up. This phenomenon has been consistently borne out in our statistical analysis.

We also broke down the analysis into shorter periods. The impact of housing and unemployment escalated over the last five years while GDP remained insignificant. Interest rates were also insignificant during that period. The housing coefficient doubled from the 15 year regression while the unemployment coefficient went up slightly. Most importantly, the R Square actually increased to 0.69 despite fewer observations (months). Now more than ever, investors need to have a view on housing and unemployment to make real money in this sector in our opinion.

So where do we stand? We defer to the Hedgeye Macro group and our financials guru Josh Steiner. Hedgeye Macro is negative on unemployment relative to consensus and Josh has written extensively on the significant hurdles the housing market face. If we are right, Las Vegas won’t be recovering anytime soon and MGM MIRAGE will struggle to maintain its 12x EBITDA multiple and/or the consensus EBITDA projection.