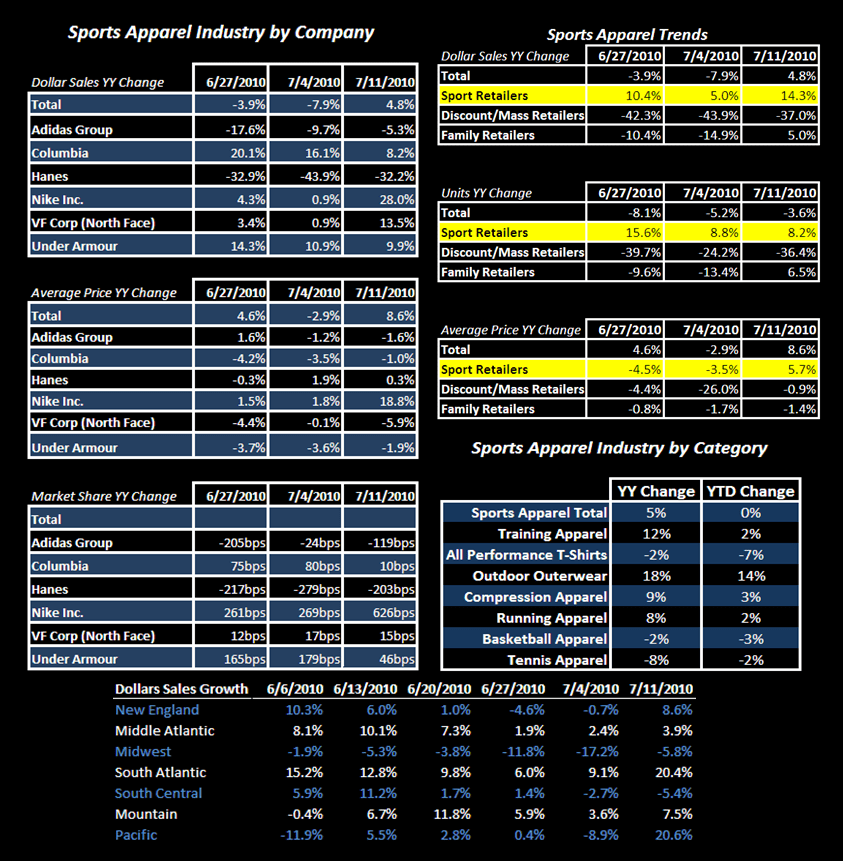

Nike Crushed It

Consumer Discretionary is clinging on for dear life. But athletic apparel sales for last week turned up sequentially. Nike crushed it. UA put in a nice dent as well. No one else came close.

Key observations from sports apparel sales for the first full week of July:

- Noticeable uptick after 3 disappointing weeks. As always, we look at the 3-week trend, which accelerated by 200bp.

- All channels improved sequentially, which in itself is rare based on the year-to-date trends. There does not appear to be a calendar shift issue or any major weather anomalies. In fact, the Northeast heat wave could have easily stunted sales last week, but it did not.

- New England, South Atlantic, Pacific/Mountain regions all showed the biggest uplift. If this is a sign of broader shopping patterns, it’ll be interesting to see how this triangulates with retailers like Payless who called the South/West as negative contributors last quarter (we’re meeting w PSS tomorrow).

- Nike had a HUGE week. I mean HUGE. Sales +28% with market share +626bps? That’s tremendous for a company that has 30% of the market.

- The next best share leader is UA, with 46bp. Might not sound as impressive, but given such a smaller sales base, it still translates to 10% sell-through growth. The recent trend of sales growth 2-3x the industry is holding for UA.

- Every other brand was a yawn/sleeper from a market share perspective. Adidas was particularly notable with sales -5.3% given its World Cup exposure. I guess not many Spain and Germany jerseys flew off the shelves last week in the U.S. despite selling nearly one-million Spanish jerseys following World Cup victory per our news run this morning.