R3: REQUIRED RETAIL READING

July14, 2010

We’ve received increased interest in names over-indexed to the gulf states of late – here are a few to keep an eye on.

TODAY’S CALL OUT

As we near day 100 of the BP Deepwater Horizon oil spill saga and the economic impact on the region shifts from near-to-intermediate term in nature, we’ve received increased interest in names over-indexed to the region. While outsized risk of underperformance in gulf state markets (i.e. TX, LA, MS, AL, & FL) is expected to soon take hold, confirmation of this reality at retail is currently mixed at best.

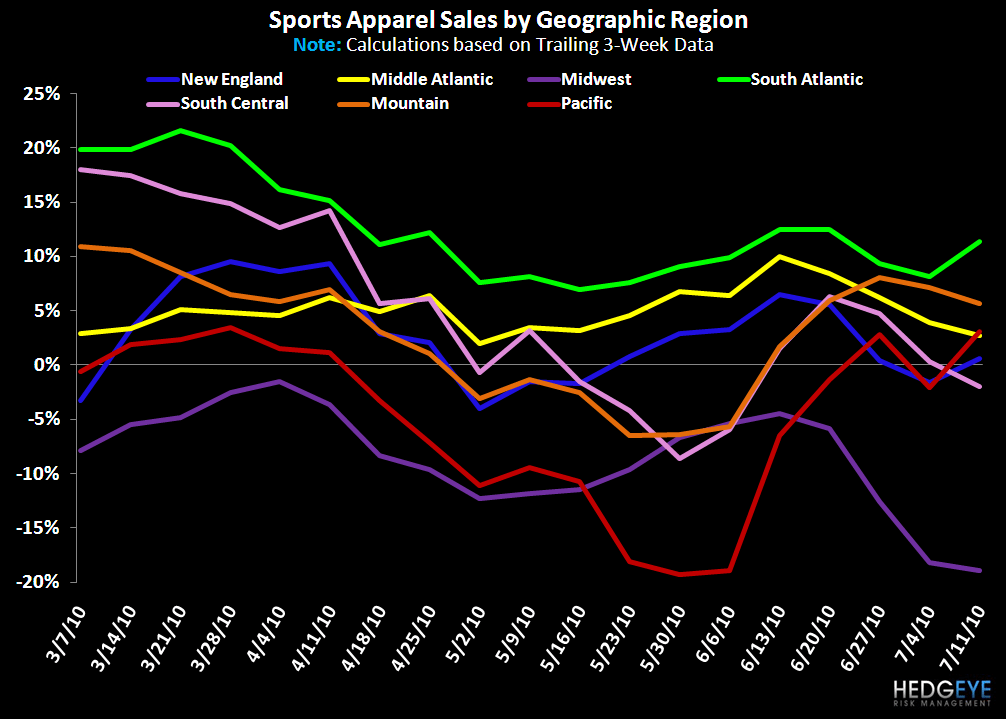

Case in point are the regional trends from our weekly Sportscan apparel data (see chart). Over the last 4-months, the South Atlantic region (including FL & AL) has reported the strongest results while South Central (including TX, LA, & MS) has held in surprisingly well on a relative basis. It’s important to keep in mind, however, this is simply one of many sources reflecting regional performance. Recall that the Midwest was highlighted as a pocket of strength in June by many retailers yet this region is a clear laggard in sporting apparel.

While the economic impact from event-driven catalysts such as the BP oil spill can take time to materialize and in some cases can be short-lived, we have run an analysis flushing out retailers with over-exposure to Gulf states. Including some names from our Restaurant sector head, Howard Penney, the retail/restaurant names with high exposure to the region include: DDS (42%), CTRN (41%), SMRT (39%), HIBB (31%), SKS (28%), SCVL (26%) as well as EAT, PFCB, and SONC. If you are interested in further detail on the broader list of names let us know.

LEVINE’S LOW DOWN

- Add maternity to the list of growing merchandise categories and demographics that privately held fast-fashion retailer, Forever 21, is targeting. The latest line called love21mternity is available online and at stores in five states. Bloggers are quick to point out that three of the five states have amongst the highest teen pregnancy rates in the country, but that’s a tough demographic positioning to prove.

- According to American Express, 61% of Americans report that customer service is more important to them in today’s economic environment and will spend 9% more when they believe a company provides excellent customer service. However, only 37% of Americans believe companies have increased their focus on providing quality service, while 27% believe there has been no change, and 28% say they believe less attention is being paid to good service.

- Burberry noted that in light of more recent global macro jitters, it has yet to see any pick up in order cancellations or changes in whole account buying behavior. Additionally, U.S department store distribution was highlighted as an area in which they are expecting to gain penetration for the Spring ’11 season.

- Retail real estate continues to struggle, despite the appearance that the health of retailers remains OK. In the second quarter, vacancy rates for shopping centers hit their highest point since 1991, while regional malls hit levels not seen since 1999. Shopping center vacancies are tracking at 10.9% while mall vacancies are at 9%.

MORNING NEWS

Avon Acquires Jewelry Company Silpada Designs - The direct seller stepped up its acquisition spree by purchasing jewelry company Silpada Designs Inc., a direct seller with operations in the U.S., Canada and the U.K., for $650 mm. The purchase is Avon’s third this year — after a 13-year hiatus from acquisitions. It follows two smaller-sized buys, the premium natural skin care range Liz Earle and the trademark of baby care line Tiny Tillia. The all-cash transaction is expected to close in the third quarter. The jewlery category offers an opportunity to polish the company’s image and style authority. <wwd.com/business-news>

Hedgeye Retail’s Take: The largest of the transactions announced over the past couple of days, but just one of many.

Asics Buys Swedish Outdoor Products Company Haglöfs - Asics Corp. said Monday that it has agreed to purchase 100% of Swedish outdoor products company Haglöfs for 1 bn Swedish krona, or $133.4 mm at current exchange, from private equity company Ratos AB. Asics said it is looking to expand its apparel business by rolling out high-quality and functional products, as well as grow its core business of running gear. Haglöfs posted a net profit of 48 mm krona, or $6.4 mm, on sales of 590 mm krona, or $78.7 mm , for the fiscal year ended Dec. 12. <wwd.com/business-news>

Hedgeye Retail’s Take: Hitting the iron while its hot, Asics looking outside the company to build and boost its apparel business. We continue to believe more capital and competition put into the space is a win for retailers and the consumer.

Billabong Acquires RVCA - Billabong International Ltd. reached a conditional agreement to acquire California apparel brand RVCA. Terms of the deal were not disclosed. Billabong expects RVCA to contribute 2% to Billabong group revenues in the 2010/2011 fiscal year and be neutral to earnings. <sportsonesource.com>

Hedgeye Retail’s Take: Nothing wrong here with an effort to bring some grassroots creativity into the corporate mix. Smaller brands continue to be the lifeblood of the “alternative” sports and lifestyle sectors.

Concept One Accessories Acquires Blue Marlin - Concept One Accessories has acquired the trademarks and Web site of Blue Marlin, the men’s sportswear and headwear brand, from New Blue Holdings. Blue Marlin, known for its vintage track jackets and caps featuring the insignia of historic Negro League and international baseball teams, went bankrupt in 2008 after reaching a sales peak of $25 mm in 2006. Its assets were subsequently bought by New Blue Holdings, an investment group. Concept One Accessories owns the Block Headwear brand and also holds more than 65 licenses. <wwd.com/business-news>

Hedgeye Retail’s Take: One of the originators of vintage athletic appears to be on the cusp of a comeback. Expect to see Blue Marlin leverage the license portfolio of its parent.

Online Private Shopping Club Beyond the Rack Received Equity Investment - Online private shopping club Beyond the Rack said Monday it has received a $12 million equity investment from Highland Capital Partners LLC and BDC Venture Capital Inc. The proceeds will be used to finance accelerated growth and expansion of operations of the Montreal-based firm, which, until this point, had been funded exclusively by angel investors. The percentage of equity to be held by the new investors wasn’t disclosed. Highland, whose previous investments have included Lululemon Athletica Inc., MapQuest Inc. and Lycos Inc., will have a favorable impact on its business both logistically and financially. <wwd.com/business-news>

Hedgeye Retail’s Take: Is the bubble nearing for “private sale” ecommerce? It now appears that private equity is going well beyond the name brand sites in an effort to get in on a piece of the latest retail trend. Certainly the RueLaLa and Vente-Privee valuations are enough to keep investors interested.

Rock Creek Athletics Acquires DeLong Brand - Rock Creek Athletics, based in Grinnell, Iowa, has acquired the varsity award jacket business assets from Daden Group, also based in Grinnell, Iowa, including the DeLong brand. <sportsonesource.com>

Hedgeye Retail’s Take: Gotta love M&A, but do kids still wear wool and leather-armed varsity jackets?

UK Retail Sales Rise in June Against Tough Comps, Helped by Sun and Clearance - UK retail sales values rose 1.2% on a like-for-like basis from June 2009's 1.4% increase, helped by the heatwave in the second half of the month. This June was slightly less hot, but sunny for most of the month. On a total basis, sales were up 3.4% against a 3.2% increase in June 2009. Clothing and footwear sales growth slowed, as many people had already bought in May's sun. TVs benefited from the football and outdoor DIY and leisure improved in the sun, but at the expense of indoor homewares. Overall shop price inflation slowed to 1.5% in June from 1.8% in May. Food inflation slowed to 1.7% in June from 2.2% in May. Non-food inflation slowed to 1.4% in June from 1.6% in May. Non-food items, including electricals and clothing, continue to be cheaper than they were this time last year. In the face of weak demand, retailers will continue to use widespread discounts and promotions. But, given their thin margins, there will be little scope to absorb next year's VAT increase. This will put significant pressure on inflation from January onwards. <brc.org.uk>

Hedgeye Retail’s Take: Outlook not looking good for the UK consumer, although this market has never been a hotbed of successful and profitable retailing.

China's Textile Manufacturers Fear Yuan Appreciation Will Lead to Bankruptcies - China National Textile & Apparel Council vice president Gao Yong told the China Daily that a 5% currency appreciation could cause half of the country’s textile companies to go bankrupt. He said the bankruptcies would be spurred by the industry’s thin profit margins of around 3 to 5 percent. The textile industry output in 2009 accounted for just more than 11% of China’s gross domestic product, a Ministry of Commerce report said. The Chinese government conducted a yuan stress test in March that indicated textile manufacturers’ profit margins would decline 1% if the currency appreciates by 1%. Textile industry profit margins already have been affected by rising raw material and labor costs, together with an appreciating yuan, which rose 21% against the dollar from 2005 to 2008. Textile products have become more expensive, resulting in diminishing price advantages compared with Vietnam, Indonesia and other Southeast Asian countries. China’s textile manufacturers could further be squeezed by rising labor costs. <http://www.wwd.com/business-news/?module=tn>

Hedgeye Retail’s Take: Interesting politicking here by the Ministry of Commerce, which surely must have known that this was coming. Seems suspect that the policies put in place would hurt such an important component of China’s GDP, without some sort of offset. As such, perhaps additional VAT rebates are on the horizon.

Chinese Footwear Exports Saw Significant Growth in the First Five Months of 2010 - China’s footwear exports recorded an increase of 45% in volume and 32% in value in May compared to the same period a year ago, according to the China Leather Industry Association. <fashionnetasia.com>

Hedgeye Retail’s Take: Easy comps coupled with one of the hottest sectors in retail is sure to lead to a substantial pick up in demand. Interestingly, China has lost some share on the margin to Vietnam and Indonesia, making these numbers appear to be even stronger.

Global Yarn and Fabric Output Suddenly Dropped in Q1 - Global yarn and fabric output dropped significantly in the first quarter, largely because of double-digit declines in production in China, an industry survey said. The biggest factor pushing down the numbers was the decline in apparel consumption, but conceded factors such as stock draw downs and scarcity of cotton supplies may have played a role. <wwd.com/business-news>

Hedgeye Retail’s Take: Sounds like another reason for inflation to pick up.

Adidas Sells Almost One Million Jerseys of Spanish Soccer Team - Adidas AG indicated it sold almost one million replica jerseys of the Spanish national team, which won the World Cup on Sunday. <sportsonesource.com>

Hedgeye Retail’s Take: Clear example of how one of the most challenged economies in the Western world can still find a reason to spend. At almost $100 for an official replica, plenty of unemployed Spaniards found a few extra dollars to focus on a positive.

Giorgio Armani SpA 2009 Earnings Drop - With the recession affecting its core business and licensed products, Giorgio Armani struggled in 2009. Total sales fell 6% but jumped 32% in China. The company closed 2009 with a cash pile of 447 mm euros. <wwd.com/business-news>

Hedgeye Retail’s Take: Interesting proxy as Prada readies its IPO. Expect to get sick of hearing about the Chinese luxury consumer at any point now.

Amazon Offers College Students Exclusive Perks - Amazon.com Inc. moved today to grab a bigger piece of the online textbook business by offering college students special deals. The world’s largest online retailer today launched Amazon Student, a free membership program that offers college students at least one year of free two-day shipping via free membership in Amazon Prime, which usually costs $79, as well as other benefits such as exclusive discounts and promotions. In doing so Amazon enables students who buy new textbooks through the site to have those books guaranteed to arrive in two days—or they can pay $3.99 for next-day delivery. The Amazon Student page, located at www.amazon.com/b/?node=668781011, also features a variety of other merchandise likely to appeal to college students, such as laptops, bedding and microwavable foods like Kraft Easy Mac. <internetretailer.com>

Hedgeye Retail’s Take: And now we wait to see what Barnes & Noble does in response now that they own one of the largest college bookstore operations in the U.S.

Retailers Seek an Edge with New Formats - The retail landscape is being remodeled as economic volatility compels stores to alter traditional formats. Large chains are breaking out the most profitable or promising segments of their businesses, such as accessories, sportswear and denim, into smaller stand-alone footprints. Other retailers are trying to appeal to a younger demographic with new labels and edgier store concepts. BCBG launched BCBGeneration to target a younger crowd and A|X Armani Exchange opened a new concept store in Los Angeles that doubles as an event space and features an art gallery. Guess is revamping its accessories-only concept, and plans to open more than 40 of those doors globally over the next year. The company’s Guess denim stores also have a new look and are branded separately from other company lines, such as G by Guess. <wwd.com/retail-news>

Hedgeye Retail’s Take: Creativity is the most overlooked factor in a retailers ability to drive sales. Those that are not investing and experimenting will ultimately lose, or be relegated to a simple one factor model, which is price.

Prada Receives 360 mm Euro Loan - Prada SpA has negotiated a three-year loan agreement of 360 mm euros to refinance a long-standing debt and to propel the company’s retail growth, its top priority. Prada is eyeing an initial public offering for the fourth time, possibly as soon as the first quarter of 2012. The timing coincides with the expiration of a 450 million euro, or $568.5 million, debt, which will partly be written off by this fresh loan, secured at lower interest rates. <wwd.com/business-news>

Hedgeye Retail’s Take: The pre-IPO cleansing process is now in full force.

Golfsmith Secures $90M Loan; Opening 14 Stores - Golfsmith completed an amendment and extension of its revolving credit facility with GE Antares Capital. <sportsonesource.com>

Hedgeye Retail’s Take: With the golf space in a malaise (was it ever really that great?), it’s unfortunate to see companies still growing for the sake of growth.

GIL Shuttering Fort Payne Hoisery Plant, Shifts to Honduras - Gildan-Prewitt company officials announced plans to relocate 30% of its knitting equipment and all its remaining wet processing operations in Fort Payne, AL to Honduras. About 130 of Fort Payne's remaining hosiery workers will lose their jobs by the end of the year. <sportsonesource.com>

Hedgeye Retail’s Take: Hard to believe there were still socks being manufactured stateside. On the other hand this is a natural off-shoring margin boost strategy that is long overdue.

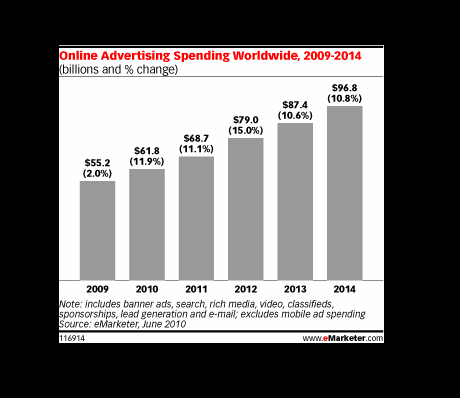

Double-Digit Growth Again for Online Ad Spend - The economy suffered around the world in 2009, but the online advertising market showed its resistance to the recession. While total media spending dropped, online ad spending increased by 2% to $55.2 bn. eMarketer forecasts that 2010 will bring a return to double-digit online ad growth, with global spending set to reach $61.8 bn. Growth will continue at rates of over 10% each year through 2014. North America and Western Europe accounted for nearly three-quarters of the world’s online ad spending in 2009, but those mature online ad markets will post slower growth rates than developing areas in Asia-Pacific, Eastern Europe and Latin America. The internet’s share of total ad spending worldwide will jump from 11.9% in 2009 to 17.2% in 2014. Continued high growth in the online space coupled with a 2009 spending decrease of 10.5% for total media, followed by a slower recovery, will help online get an ever-larger slice of the ad spending pie. <emarketer.com>

Hedgeye Retail’s Take: Nothing surprising here, given the relatively small share online advertising currently has in the grand scheme of things. Furthermore, the with higher ROI’s and almost infinite ways to get closer to specific target audiences online ads just make a heck of a lot of sense.