Last week, 2 of the 8 risk measures registered positive readings on a week-over-week basis, while four were neutral and two were negative.

Our risk monitor looks at the following metrics weekly:

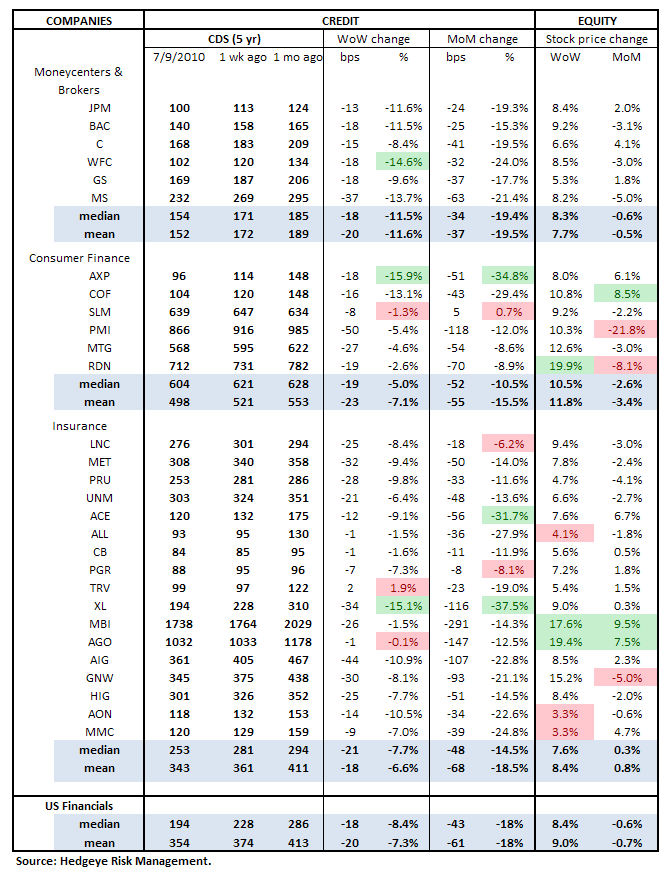

1. CDS for all available US Financials (30 companies).

2. High Yield

3. Leveraged Loans

4. TED Spread

5. Journal of Commerce Commodity Price Index

6. Greek Bond Spreads

7. MCDX Municipal Bond Credit Default Swaps

8. AAII Bulls/Bears Sentiment Survey

1. Financials CDS Monitor – Swaps came in across the board last week. AXP, WFC, and XL were the most improved, while only TRV had wider spreads week-over-week. Conclusion: Positive.

Tightened the most vs last week: WFC, AXP, XL

Widened/Tightened the least vs last week: TRV, SLM, AGO

Tightened the most vs last month: AXP, ACE, XL

Widened/Tightened the least vs last month: SLM, LNC, PGR

2. High Yield (YTM) Monitor – High Yield rates dropped 11 bps last week. Rates closed the week at 8.95% down from 9.06% the week prior. Conclusion: Positive.

3. Leveraged Loan Index Monitor - The Leveraged Loan Index rose 2 points last week, closing at 1456 versus 1454 the week prior. Conclusion: Neutral.

4. TED Spread Monitor - Last week the TED Spread rose slightly, closing at 38 bps, up from 37 bps in the week prior. Conclusion: Neutral.

5. Journal of Commerce Commodity Price Index – The JOC smoothed commodity price index is a useful leading indicator. A sharp sell-off in this index starting in July ’08 heralded further declines in the stock market. This week, the index was down slightly, closing the week at 8.6, down just over 1 point versus last week’s close at 9.8. Conclusion: Neutral.

6. Greek Bond Yields Monitor – Greek bonds yields and CDS continue to show turmoil in the Aegean. Last week yields rose modestly, ending the week at 1033 bps versus 1020 bps the prior week. Conclusion: Negative.

7. Markit MCDX Index Monitor – We are replacing the Markit ABX Index with the Markit MCDX Index, a measure of municipal credit default swaps. We believe this index will be a useful indicator of pressure in state and local governments. Each index is a basket of 50 municipal reference entities, both revenue and GO, and the chart displayed is the average of four indices with 5-year tenors. After rising for much of the last month, it fell on Friday to book a decline for the week. Spreads closed at 228 versus 252 a week ago. Conclusion: Neutral.

8. AAII Bulls/Bears Monitor - The Bulls/Bears survey grew more bearish on the margin vs last week, reaching its most bearish reading since the market bottom in March 2009. Bulls decreased by 3.8% to 20.9% while Bears rose 15.1% to 57.1%, pushing the spread to 36% bearish, versus 17% bearish the prior week. Conclusion: Negative.

One caveat is that our interpretation of the AAII Bulls/Bears survey is that a more bearish reading is bearish. Most market observers would use this survey as a contrarian indicator, which we wouldn't disagree with from a practitioner standpoint. However, for the purposes of this risk monitor, we treat an increase in bearish sentiment as a negative.

Joshua Steiner, CFA

Allison Kaptur